Congratulations to 5 team

members who have been promoted, in recognition of their hard work and contributions

to our client-first culture.

Ryan Mulhearn, CIMA® and

Michael Warch to Associate Financial Advisor, and Nico Wolfgang was promoted to

Senior Associate. READ MORE

Elizabeth Wilson, CPA was promoted to Vice President, Finance & Tax Services, and Judianne

Harris was promoted to Chief Marketing Officer. READ MORE

AWARD SPOTLIGHT Elizabeth Wilson, CPA has been selected as the Rising Star Award recipient by Lehigh Valley Business as part of the 2019 CFO of the Year Awards. READ MORE

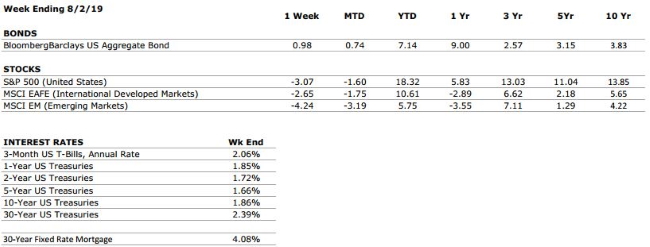

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A

Our consumer spending grade remains an A. Surveys of US consumers continue to indicate that the consumer is in a strong position, and recent GDP data provided further evidence of healthy consumer spending.

FED POLICIES

B+

Our Fed Policies grade remains a B+ after the Federal Reserve opted to cut its interest rate target by 25 bps following last week’s meeting. The cut was widely anticipated by markets, and if history is any representation, it is unlikely to be the last.

BUSINESS PROFITABILITY

B-

With 77% of S&P 500 companies having reported earnings as of August 2, the EPS growth rate for the second quarter is -1%. If that number holds up, we will have observed two consecutive quarters of year-over-year earnings declines for the first time since 2016.

EMPLOYMENT

A

The US economy added 224,000 new jobs in June, beating consensus estimates by a wide margin. We continue to view the jobs market as very healthy.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but as the economic cycle continues to mature, this metric will deserve our ongoing attention.

OTHER CONCERNS

INTERNATIONAL RISKS

6

On a 10 point scale, we currently assess the “international risks” to markets as a 6. The key areas of focus for markets remain US/China trade relations, the ongoing Brexit negotiations, and escalating tensions in the Middle East.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

People

with a financial adviser say they aren’t just better with money – they’re

happier with life overall. We think so, of course, but

don’t take our word for it… read (and share) this Business Insider

article covering the results of a Northwestern Mutual survey. READ MORE

by Connor Darrell

CFA, Assistant Vice President – Head of Investments As

was widely anticipated by markets, the Federal Reserve opted to reduce its

target interest rate by 0.25% last week. However, the dovish pivot was not

enough to support equity markets, which ended the week in a downswing following

a series of tweets from President Trump which indicated he was moving forward

with an additional round of tariffs on Chinese goods. That this announcement

came just one day after the Federal Reserve’s interest rate decision is likely

no coincidence, as the Fed’s accommodative stance will provide the President

with greater confidence that the economy can withstand the consequences of

upping the ante with the Chinese.

With the confirmation that interest rates

would slide downward and the increase in equity volatility stemming from

President Trump’s tariff announcement, the bond market managed a small rally

last week. The Barclays Aggregate Bond Index is now in the midst of one of its

strongest years since 2011.

Global Manufacturing in Contraction Purchasing

Managers’ Indices (which utilize survey data to evaluate business confidence

and manufacturing activity) released last week revealed that global

manufacturing activity remains challenged by the uncertainties posed by the U.S.-China

trade dispute and Brexit negotiations. The U.S. PMI remains the only major

region that has held above 50 (a critical level which separates expansion and

contraction), though it has declined materially over the last several quarters.

PMIs in the eurozone, Japan, and China all remained below 50 last month,

indicating that these manufacturing markets are in contraction.

Manufacturing is far more cyclical than

top line economic growth, but the reduction in global manufacturing activity

that we have observed over the past year is a symptom of the toll that mounting

geopolitical uncertainties are having on business decisions. If businesses’

reluctance to invest in production permeates into hiring decisions, it could begin

to impact labor markets and accelerate the arrival of the next recession. Given

the relative health of the U.S. economy and the potential for these

uncertainties to be lifted by a simple handshake between Presidents Trump and

Xi, this scenario looks a long way from playing out. But for investors who have achieved double

digit returns in a year where the economic backdrop has continued to weaken,

this type of data should not be ignored and may represent a reminder of the

prudence of maintaining discipline and avoiding the urge to chase returns

during late cycle investing.