We are pleased to

welcome Amanda Schneck to our team as Front Office Coordinator for our

Bethlehem headquarters. Amanda will be taking over the responsibilities for

Caroline Kohler who has been promoted to Administrative Assistant for our Tax

Department. Amanda has more than 10 year of experience in client service, and

she is eager to get to know our clients. We look forward to introducing her to

you as she learns from and takes over for Caroline as front office reception, answering

your phone calls, and general office coordination.

Inflation and Your Portfolio The VNFA Investment Department takes a long-term approach to managing inflation. Although our team stays abreast of all regular data points, we do not endeavor to alter the portfolio meaningfully based on short-term metrics because we feel that we are strongly positioned for a range of long-term inflationary scenarios. Our fixed income portfolio maintains a duration approximately 2/3 of that of the Barclays Aggregate Bond Index, our benchmark. In turn, our fixed income is likely to outperform in an inflationary scenario under which interest rates increase. While our fixed income holdings may underperform in a falling-rate outcome, our investment personnel believe that a persistent declining rate environment is improbable given how low rates are at present. On the equity side, we are invested with a modest growth tilt. Generally speaking, growth companies are relatively insulated from inflation as they oftentimes have pricing power, enabling them to pass higher prices onto their customers and maintain profitability. On the other hand, our equity managers have proven their long-term outperformance in recent periods, which were characterized by tame inflation.

VNFA’s Investment Department remains adaptable to new

information but disciplined with respect to a long-term outlook. WATCH

A SHORT VIDEO to learn more about the general impact of inflation on your

investment portfolio and reach out to your Financial Advisor or our Investment

Department with any questions.

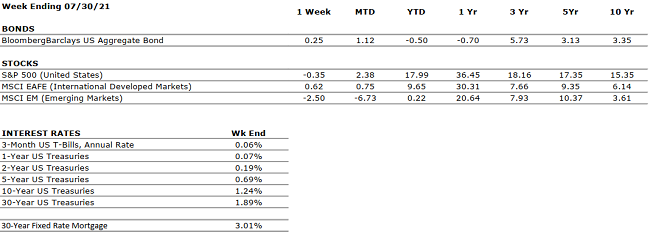

by Maurice (Mo) Spolan, Investment Research Analyst The Dow Jones, S&P 500 and Nasdaq 100 returned -0.36%, -0.35%, and -1% last week. Nonetheless, July represented the sixth straight positive month for the S&P and all three indices are up healthily – between 15% and 18% – year-to-date.

In economic news, U.S. GDP increased at a 6.5% annualized pace in Q2. While a very high number, based on historical standards, the result was far below expectations of 8.4%. At least some of the shortfall is attributable to the global supply chain constraints, as lack of inventory decreased GDP by nearly $200 billion. On the positive side, the U.S. has now recovered all its GDP losses incurred during the pandemic. Consumer spending increased at an average 12% pace and consumer confidence is at a 17-month high. Economists expect U.S. GDP to decelerate to some degree in the second half of the year, but overall, for growth to remain very healthy.

Q2 S&P 500 results are incredibly strong, as sales and earnings are up 21% and 86%, respectively; growth rates in both metrics are near or at record levels. Similar to GDP, corporate results are exacerbated because they are compared to a period in 2020 in which economic activity was extremely limited. On the other hand, many companies are struggling with inventory shortages, which curbed results. Analysts anticipate that corporate performance will remain strong through this year and into next.

The Fed concluded its two-day meeting by leaving rates near zero, as expected. Jay Powell cautioned that the economy has a way to go before the Fed moves rates upwards but has made significant progress towards the Fed’s goals. Powell reiterated, yet again, his view that inflation is transitory. By contrast, the IMF (International Monetary Fund) expressed the opposite view and recently encouraged global central banks to take preemptive action to prevent inflation.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

Q2 U.S. GDP grew at a 6.5% annualized pace; a very strong number, historically speaking, but below the 8.5% expectation. A lack of inventories, resulting from a constrained global supply chain, reduced GDP by nearly $200 billion.

CORPORATE EARNINGS

POSITIVE

With about half of S&P 500 constituents having reported Q2 results, sales and earnings growth are running at an astonishing 21% and 86% pace when compared to the heavily depressed figures from Q2 2020.

EMPLOYMENT

POSITIVE

In June, the U.S. economy added 850,000 jobs, beating expectations handily. The unemployment rate is 5.9%, well within normal parameters.

INFLATION

NEUTRAL

Inflation accelerated to 5.4% in June. Jay Powell, Federal Reserve Chair, believes that the recent uptick in inflation is primarily attributable to global supply chain constraints, and that inflation will slow as such constraints resolve through the remainder of the year.

FISCAL POLICY

POSITIVE

The Senate voted to advance the $550 billion bipartisan infrastructure bill, opening up the bill to debate and amendments.

MONETARY POLICY

POSITIVE

The Federal Reserve indicated that it plans to hike rates twice in 2023. Previously, the Fed had suggested it would not raise rates until 2024. Nonetheless, the monetary stance is accommodative in the near future.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

With multiple vaccines in distribution and accommodative fiscal and monetary policies in place, 2021 is looking like one of the strongest economic years on record. The primary risk at present is that of persistent inflation which begets higher interest rates.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie can address question on the air that are submitted either in advance

or during the live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.