by William

Henderson, Vice President / Head of Investments The equity markets reacted negatively to

the discovery of a

new highly transmissible COVID-19 variant

in South Africa. The announcement of a new strain, dubbed omicron by the World

Health Organization, shocked markets and impacted

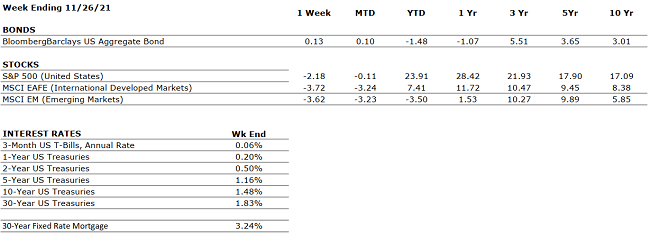

most major sectors. The Dow Jones

Industrial Average dropped by -2.7%, the S&P

500 Index fell by -2.3% and

the NASDAQ dropped by -3.1%. However,

all three major indexes remain in

positive territory for the year. Year-to-date,

the Dow Jones Industrial Average has returned +15.9%,

the S&P 500 Index +23.9%

and the NASDAQ +20.9%. The U.S.

Treasury market

reacted as expected to bad

news,

with prices rising on bonds,

reminding investors why bonds

remain an anchor in most

portfolios – providing the needed

risk management tool while risk assets

are selling off. Last Friday, the 10-year

U.S. Treasury briefly dipped below

1.50%, before settling

in over the weekend at 1.53%, four basis

points lower than

last week and well below the 1.74%

level reached in March of this year.

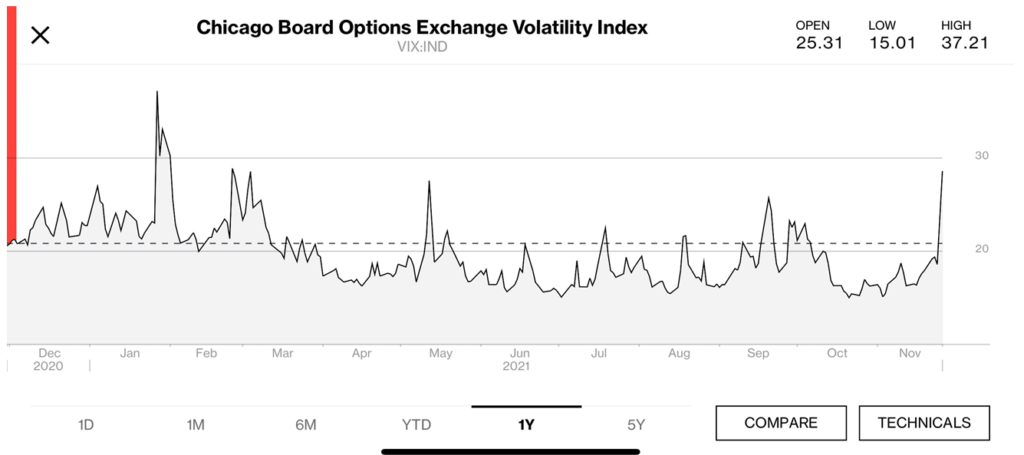

Last week, we

talked about the VIX (CBOE

Volatility Index – or measure of

the market’s risk level) and

how “calm” the VIX

had been thus far in 2021.

Well, add in an omicron variant,

and the VIX spikes to

a 10-month

high. See

the chart below from Bloomberg.

As of the writing

of this

article, the markets are already rebounding nicely, and

many market prognosticators

are calling it a “buying opportunity.” We

often get that question: “Is this

a buying opportunity?” Our

answer is always the same: “YES!” If

you are a long-term investor, with appropriate risk levels applied

to your portfolio, every

day is a buying opportunity as time

generally smooths out peaks

and valleys in the markets.

Certainly, this

new COVID-19 variant

puts the unknown

element back into the

markets, but we have seen this before

with the delta variant and

the pharmaceutical firms are

already touting the

need for another booster

shot to deal with the omicron variant. Further, FED

policy markets are well aware of

the issue and resultant

market and economic

implications. This means that

their announced monetary policy tightening, and bond purchase

tapering could at any time be adjusted.

In fact, trading markets

are already pushing out their expectations

of the first rate

hike to July 2022 from June 2022.

Lastly, there seems to

be an overall consensus gathering in Washington and

Wall Street that

the pandemic is becoming endemic and

will be with us in some form or another for

quite a

long time. For each sector negatively

impacted by lockdowns

and new COVID strains such as

travel & leisure, there

are sectors that are

positively impacted such as technology and

bio-tech. There are a

lot of economic indicators being released

this week including

data around retail

sales, home prices

and the labor markets. This

information will give us needed information

about the future of the economy, the

direction of Fed policy and

the sentiment and strength

of the consumer. Inflation continues

to be a concern and

the question remains

about which parts of inflation will be

transitory vs. permanent.

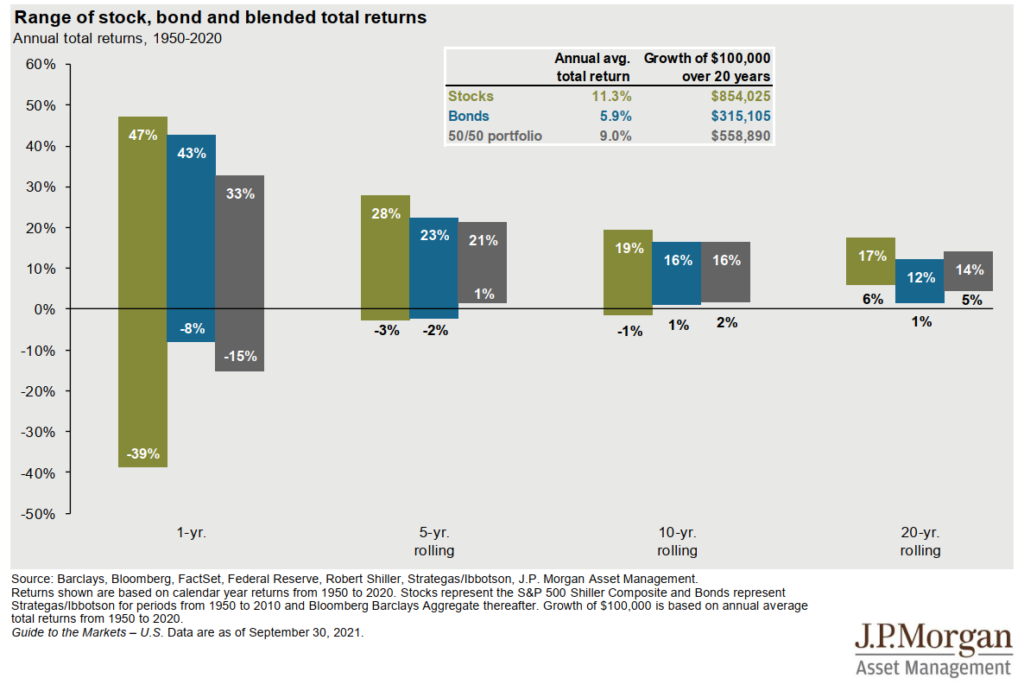

Certainly, last week was a

sell-off in all market sectors but we have talked about sell-offs occurring in

every major bull market – so this is generally typical market behavior. However,

over

long periods of time, sell-offs are simply blended into long-term

returns. See the chart below from JP Morgan showing performance of portfolios over

time.

In any given single year,

equities alone can produce a return of –39% and a blended portfolio of

–15%. Looking out 20 years, both portfolios are in positive

territory. Simply put – investing is a long-term activity.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. GDP growth decelerated to a 2% annualized pace in Q3. The slowdown was driven primarily by supply chain constraints. Economists expect a modest acceleration in Q4.

CORPORATE EARNINGS

POSITIVE

With 95% of S&P 500 companies having reported Q3 results, sales and earnings are up 17.5% and 39%, respectively. However, company commentary suggests that the supply chain has been and will continue to be problematic in the coming quarters.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 4.6%, as of October. The labor market is very tight at present as many employers, particularly in the Leisure and Logistics sectors, are struggling to fully staff because the labor participation rate remains below pre-COVID levels. The labor shortage is one of the causes of the global supply chain glut.

INFLATION

NEUTRAL

CPI rose 6.2% year-over-year in October, the highest increase since 1990, driven by the global supply chain backlog. Will inflation be transitory or permanent?

FISCAL POLICY

POSITIVE

A $1.2 trillion infrastructure bill was passed by Congress. A $1.75 trillion spending bill passed by Congress also went to Senate for revisions.

MONETARY POLICY

POSITIVE

The Fed will begin bond tapering by November’s end. By mid-2022, all Fed bond purchases will halt. The Fed’s bond buying program works to keep interest rates low. Inflation concerns are persisting, and some are calling for faster tapering and high rates.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

A new COVID-19 variant, omicron, was discovered in South Africa and countries around the world immediately reacted by closing borders to foreigners. While still new and unknown, this needs to be closely watch for potential long-term impact globally and risks of new “lockdowns,” which could severely impact economic recoveries.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions are hampering the economy; however, demand remains very strong. While global logistics are operating far below normal efficacy, it appears the supply chain is slowly improving and may reach normalcy by mid-to-late-2022.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

“Tomorrow is the most

important thing in life. Comes in to us at midnight very clean. It’s perfect

when it arrives and it puts itself in our hands, and hopes we’ve learned

something from yesterday.” – John Wayne

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.