Vice

President at Valley National Financial Advisors Announces Retirement

Michael Ippoliti, MBA, CFP®

After 18 years as a Financial Advisor at Valley National

Financial Advisors, Michael Ippoliti, MBA, CFP®

will retire at the end of 2021.

Mike became a financial professional as a second act after a

successful 30-year corporate career with management positions in engineering,

accounting, and planning. Inspired to make a significant impact on people’s

lives, Mike chose the path of financial planning. In addition to his degree in

Engineering, Mike learned Personal

Financial Planning from Moravian College, earned an MBA with a concentration in

finance from Lehigh University, and is a Certified Financial Planning

ProfessionalTM. In 2003, he joined the team at VNFA and has been

helping our clients make financial choices with a holistic approach ever since.

“It has been a joy for me to do this work and to form the

relationships I have with my clients and community,” Mike says of his time at

the company.

Michael Warch and Michael Ippoliti, MBA, CFP®

Michael

Warch, an experienced Financial Advisor recruited to join VNFA in 2018, will

continue to serve the client relationships Mike has been responsible for over

the years. “I have spent the past three years preparing Mike Warch to carry on

my work and take over as Financial Advisor for the clients I have served. My

wife and children are among them, so I can say with confidence that those

clients are being left in good hands with Mike and the team at VNFA. Mike’s 10

years of experience and the depth of this independent organization are and will

continue to be a valuable support for their families, and mine.”

Mike looks forward to continuing to spend time with his wife

serving in the community and enjoying travel and outdoor adventures.

All of us at VNFA will miss having him on the team, and we

wish him all the best living in retirement.

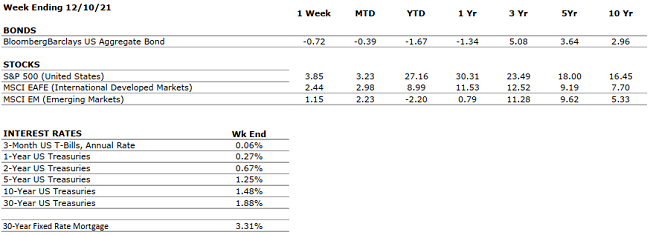

by William Henderson, Vice President / Head of Investments Last week the markets shrugged off Omicron-related news and strong November inflation numbers as all three major indexes closed higher. The Dow Jones Industrial Average jumped by +4.0%, the S&P 500 Index rose by +3.8%, setting a record, and the NASDAQ gained +3.6%. With fewer and fewer days left in the year, we are moving to close 2021 out with some near record levels on all three major indexes, giving us quite a year of overall returns. Year-to-date, the Dow Jones Industrial Average has returned +19.7%, the S&P 500 Index +27.2% and the NASDAQ +22.0%. As mentioned, the year-over-year CPI (Consumer Prices Index) for November was reported at +6.8%, the highest reading on inflation since 1982. This information gives Fed Chairman Jay Powell the ammunition needed to consider moving interest rates higher before June 2022, which was the previously telegraphed date. We will get some further direction this week at the FOMC (Federal Open Market Committee) meeting December 14-15. The 10-year U.S Treasury ended the week at 1.47%, seven basis points higher than last week and still below 1.74% level reached in March of this year.

Chairman Powell will consider the

Fed’s so-called “dual mandate,” 1) average inflation at 2% and 2) unemployment

rate at

4.1%. See

the chart below from Factset which

shows we are nearing the point where both mandates are being met.

It is likely that the FOMC

announces a faster pace in their balance sheet tapering process. Currently,

they are tapering (reducing purchases of bonds) by $15

billion per month; an

increase to $30 billion per

month is likely. At

that rate, the Fed would wind down the tapering process by March of 2022,

thereby allowing the start of the rate hikes, if

needed. At

any rate, we expect rate hikes to be clearly telegraphed, measured and

incremental.

A lot of noise is being made

about rates hikes and the Fed “Hawkish Pivot,” meaning a Fed that will raise

rates rather than keep them lower. Certainly,

interest rates at the Fed’s current target range

of 0.00 – 0.25%, are accommodative to economic growth, but interest rates at

100 or even 200 basis points higher are still considered accommodative

by historical standards. We are not predicting huge

interest rate moves like that, but it

seems to us that higher rates are inevitable. When

we look at the Fed’s last tightening cycle (December 2015

– June 2019), interest rates moved from 0.00% (post the Great Recession) to 2.50%. During the

period, the S&P 500 Index moved higher by 57% (or 11%

per year). Of course, past performance is

never a preview of future performance, but we showed that data simply to prove

that markets can move higher even while the Fed removes monetary

accommodation.

Lastly, even while the Fed

begins to raise interest rates, we expect bonds to continue to offer investors

an important risk management tool – critical to their portfolios. A

look at the current U.S. Treasury 10-Year Breakeven

Inflation Rate shows the level at 2.44% (Federal Reserve

Bank of St. Louis). The breakeven inflation rate represents a

measure of expected inflation derived from 10-Year Treasury Constant Maturity Securities and

10-Year Treasury Inflation-Indexed Constant Maturity Securities. The

latest value (2.44%) implies

what market participants expect inflation to be in the next 10 years, on average,

well below the 6.8% inflation number released last week.

Watch for

retail sales data this week as we get our first glimpse of holiday shopping data. Further,

early indications show supply chain issues are slowly getting worked out in West

Coast ports as we showed last week with falling shipping

rates (China to U.S.). The Omicron variant’s impact

seems to have abated a bit in the U.S. while the opposite is happening in the

U.K and elsewhere globally. The Fed and the Biden Administration have

their hands full and will need to decide where, when and how to remove monetary

and fiscal stimulus, both of which have powerfully and effectively fueled strong price inflation

in goods and services. Wall Street trading desks will

be thinly staffed for the next few weeks; so, watch for limited volatility

but remain focused

on your long-term goals.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. GDP growth decelerated to a 2% annualized pace in Q3. The slowdown was driven primarily by supply chain constraints. Economists expect a modest acceleration in Q4.

CORPORATE EARNINGS

POSITIVE

Huge year-over-year increases in corporate earnings are likely to decelerate in 2022 as CapEx begins to have an impact on income statements. The supply chain disruptions have forced a significant surge in CapEx as companies improve delivery and shipping processes and raw materials costs continue to increase. However, this spending is still a tailwind for earnings.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 4.2%, as of November. The labor market is very tight at present as many employers, particularly in the Leisure and Logistics sectors, are struggling to fully staff because the labor participation rate remains below pre-COVID levels. The labor shortage is one of the causes of the global supply chain glut.

INFLATION

NEUTRAL

CPI rose 6.8% year-over-year in November, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Will inflation be transitory or permanent? Powell may remove “transitory” from his testimony this week.

FISCAL POLICY

POSITIVE

A $1.2 trillion infrastructure bill was passed by Congress. A $1.75 trillion spending bill passed by Congress also went to Senate for revisions.

MONETARY POLICY

POSITIVE

The FOMC meets this week. Watch for wording around “transitory inflation.” By early 2022, all Fed bond purchases will halt. The Fed’s bond buying program works to keep interest rates low. Once tapering ends, rate hikes follow. Mid-June or sooner for rate hike?

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

The new omicron COVID-19 variant has shown up in many parts of the world. This strain seems

less virulent and more reactive to boosters so its impact it still yet to be calculated. President Biden threatened a 2022 Olympics boycott in China. Russia builds up its border with the Ukraine.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions are hampering the economy; however, demand remains very strong. While global logistics are operating far below normal efficacy, it appears the supply chain is slowly improving and may reach normalcy by mid-to-late-2022.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.