We Are Hiring! Team VNFA seeks a motivated, self-starting, passionate leader to join our Bethlehem Office in the role of Client Service Manager. The Client Service Manager will oversee client-facing support staff and be responsible for procedures contributing to the client experience. READ MORE / APPLY ONLINE

2022 Volunteer Challenge Project Team VNFA has been working hard on gathering the items we will need to complete our 2022 Volunteer Challenge Project with Community Bike Works.

We will be restoring their garden to be used as part of their youth programing this summer. If you would like to help, our team could use donations of gift cards to Home Depot or Lowe’s, bags of organic potting soil, paint brushes, marigolds or sunflowers, large flowerpots, or berry bushes.

Our Tax Department has begun filing

tax return extensions. If we did not receive all of your information and supporting

documents by April 1, we are likely going to file an extension on your return.

Please refer to the following guidance about preparation of an extension:

Still give us whatever information you have as soon as possible or as soon as it becomes available.

Expect to pay an anticipated taxes owed by the original filing date in April. We will determine if you will have a balance due or if you ca expect a refund based on the available tax information you submit.

If you are required to make quarterly estimated tax payments, individual first quarter estimated tax payments are due April 15.

If you are anticipating a large refund, we will try to get your extended return completed as soon as possible once all tax information is available.

by William Henderson, Chief Investment Officer Volatility and uncertainty are the best two words to succinctly describe the first quarter of 2022 and, as we have always said, both of those are bad for markets. Markets like boring and we did not get a lot of boring in the first quarter of 2022. Instead, we had continuing high inflation data, Russia starting a war with Ukraine, and the first Fed rate hike since December 2018. Over the course of the quarter, we saw violent swings in the stock market and huge intra-day moves in prices, which were largely attributed to uncertainty around the Russia/Ukraine war. War in that region severely impacted prices for certain commodities and strained an already stressed market still suffering from global supply chain issues due to the pandemic. Ukraine and Russia are large producers of oil, natural gas, wheat, and certain rare early elements such as palladium which is used to make catalytic converters for cars and trucks. Additional shortages in these critical commodities immediately spiked higher prices across the board and sent overall inflation numbers higher.

Quarter-end returns do not

accurately reflect the markets’ violent swings

during the quarter. Looking at the chart below from Valley National

Financial Advisors and YCharts, we see the quarter-end numbers for each major

market index.

While the chart shows the NASDAQ

at -9.1% for the quarter-end March 31, 2022, at the bottom of the quarter, the

NASDAQ was down over -20%. The

chart reflects the huge move upward during the month of March as the risk-off

trade faded and investors moved again to buy equities. For

the quarter-end March 31, 2022, the Dow Jones

Industrial Average fell -4.75%, the

S&P 500 Index fell -4.95% and the

NASDAQ fell -9.10%. Fixed

income investors fared no better as the Barclays Bloomberg U.S. Aggregate Bond

Index (a widely used measure of fixed income investment performance) fell

-6.12% in the first quarter. The

benchmark 10-Year U.S. Treasury bond started the year at 1.52% and ended the quarter

80

basis point higher at 2.32%.

Around mid-March, the markets

forged a dramatic turnaround as investors believed equities

fell enough now warranting

buying again. In our

opinion, the markets were simply focusing on the strength

and solid fundamentals underlying

the

U.S. economy: corporate profitability, bank

health, the strong labor market,

and consumers’

overall financial health. While

these factors alone were not enough cure all the world’s ailments,

specifically the Russia/Ukraine

war, they

were enough to pull investors back to U.S. equities.

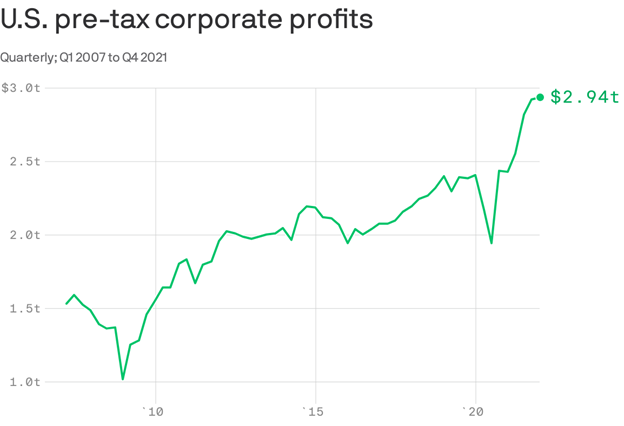

Corporate profitability,

while slowing a bit so far this year, hit a record in

2021,

and is expected to continue its upward trend in 2022. For

the full year 2021, pre-tax profits rose 25% to roughly $2.81 trillion, which

more than outpaced the 7% rise in consumer prices over the

same stretch; proving that companies were able to

pass on to their customers much

of the underlying spike in materials and

labor costs. (See

the chart below from the U.S. Commerce Department

showing U.S. pre-tax corporate profits

2007-2021.)

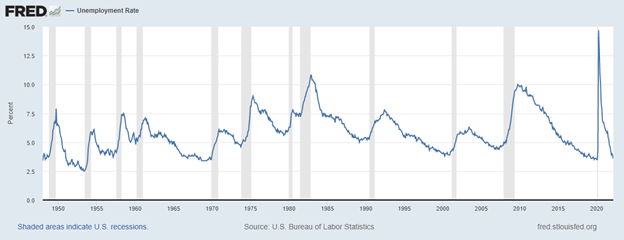

The labor market continues to be

strong with new jobs being created each month. The unemployment rate fell to 3.6% in

March from 3.8% a month earlier, quickly approaching the February 2020

pre-pandemic rate of 3.5%, a 50-year low. While low, the jobless

rate helps to boost wages, higher inflation continues to impact workers pockets

as prices for basic goods

like gasoline and food creep higher each month. (See

the chart below from the Federal Reserve Bank of St. Louis showing the unemployment rate since

1950).

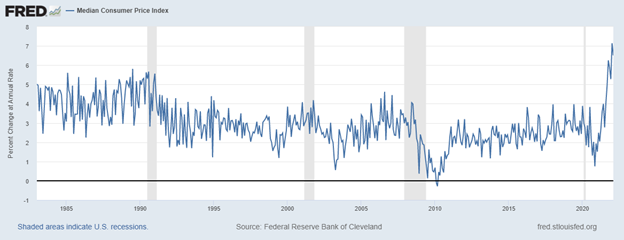

As mentioned, corporate

profitability shows that

companies have been able to pass

on inflationary prices of materials to the consumer. Further, more people are working as

evidenced by the unemployment rate. Certainly, these two factors coupled with global supply chain

issues and commodity shortages exacerbated by the Russia/Ukraine war have impact inflation

beyond the Fed’s 2.5% target rate. Hence, Fed Chairman Jay Powell’s response by raising interest rates

at the March 2022 FOMC meeting. Given where inflation and employment levels are, we expect,

along with all Wall Street economists,

more rate hikes to follow in 2022. For a visual of how dramatic the

inflation spike is, see the chart below from the Federal Reserve Bank of St.

Louis showing the

Median Consumer Price Index (common

gauge of inflation) 1985-March

2022.

There’s an old Wall Street

maxim that states:

“higher prices cure

higher prices.” Essentially,

stating that as prices increase, fewer buyers

will emerge and thereby decreasing demand and high prices. In the current case, we have very

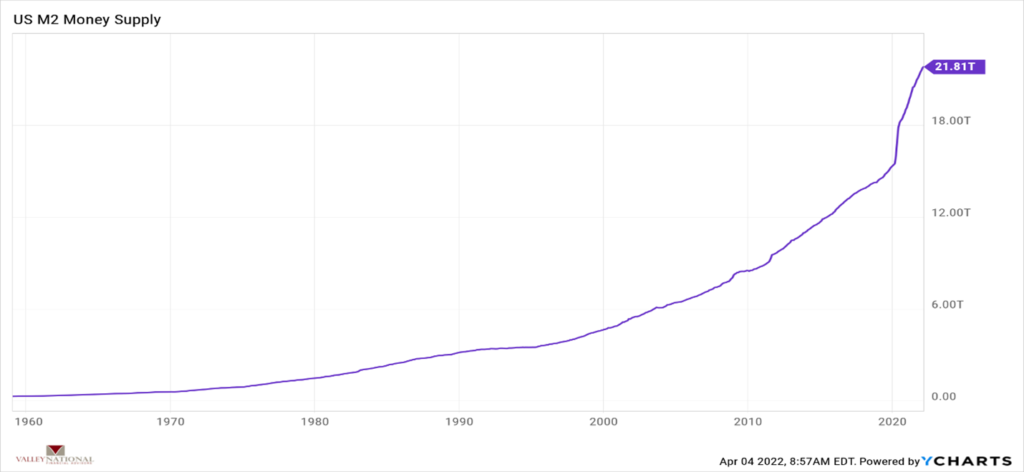

healthy consumers with a lot

of cash in

their coffers accumulated over the past two years as spending on leisure activities was practically halted yet

cash continued to build up from savings and government stimulus funds widely distributed to Americans. M2 – the measure of the total U.S.

Money Supply stands at a record $21.8 Trillion,

giving consumers a lot of cash to spend – eventually. (See the chart below from Valley

National Financial Advisors and YCharts

showing M2).

“Eventually” is the key word here. The second quarter of 2022 brings Spring

and the widespread lifting of pandemic-related lockdowns. With the grand reopening of the U.S.

economy,

consumers will be released to spend and enjoy travel, leisure, and other expensive activities – all

at the newest, latest, and greatest “higher prices.” “High prices cure high prices.”

While the pandemic in the United States seems well behind

us, other parts of the world are still suffering its devastating effects. For example, China continues to

impart severe lockdowns on whole regions in

an

attempt to quell the

spread of COVID-19. Further, the Russia/Ukraine war is far from over resulting in continued disruptions in

key commodities such as oil and wheat, which are dramatically impacting prices

in the EU region and beyond. The U.S. is not immune to the

pandemic or inflation and the Fed continues to watch both reminding us along

with way that their dual mandate of full employment and 2.5% annual inflation

are front and center for Powell. While the first quarter of 2022 produced negative returns for stocks

and bonds (a very rare event), we remain positive on the economy and the

markets for the remainder of the year with a word of caution for investors.

Volatility will be present based on continuing unrest due to geopolitical

events and

continued pressure due to inflation, which will certainly shape the direction and severity of interest rate hikes by the Fed.

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. Real GDP growth for Q4 2021 increased at an annual rate of 7.0% compared to 2.3% in Q3 (according to second estimate). The acceleration was driven primarily by private inventory investment. Real GDP increased by 5.7% in 2021 versus a decrease of -3.4% in 2020. For Q1 2022, estimate show GDP growing at 1.7% at an annual rate.

CORPORATE EARNINGS

NEUTRAL

For Q1 2022 the estimated earnings growth rate is 4.8% – the lowest since Q4 2020 (3.8%). This estimate was revised downward from the previous forecast of 5.7% in December 2021. So far, 12 out of 17 companies reported a positive EPS surprise and 14 beat revenue expectations. Sixty- seven S&P500 companies issued negative EPS guidance and 29 companies issue positive EPS guidance.

EMPLOYMENT

POSITIVE

Total nonfarm payroll employment rose by 431,000 in March, and the unemployment rate edged down from 3.8% to 3.6%. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, retail trade, and manufacturing.

INFLATION

NEGATIVE

CPI rose 7.9% year-over-year in February 2022, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Inflation concerns are clearly impacting the markets, the FED and consumer behavior. CPI for March will be released on April 12th.

FISCAL POLICY

NEUTRAL

Congress passed a $1.5 trillion spending package expected to be signed into law next week. Republicans rejected any additional COVID-19 related aid, which was removed from the bill. $13.6 billion aid package to help Ukraine saw strong bipartisan support. The Violence Against Women Act was reauthorized and Democrats pushed for a 6.7% increase in domestic spending.

MONETARY POLICY

NEUTRAL

The Fed raised rates by the expected 25 bps last week and Jay Powell projected a clear path for 2022 with as many as six additional rate hikes bringing short-term rates to 1.75-2.00% by year end 2022. Reduction of the Fed’s balance sheet was not mentioned.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

The conflict between Russia and Ukraine keeps worsening as negotiations are not leading to any results and attacks by Russia do not cease. Russia has been able to avoid defaulting on their debt and recently made a $447 million payment however, experts think a default on the next payment of $2.2 billion due April 4th is likely.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but the rising cost of oil due to the Russian-Ukraine war is likely to cause additional inflationary pressures not only on gasoline prices but also on many other goods and services.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie will discuss: A First Quarter Market Update

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.