Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie will discuss: Navigating Social Security Options

Laurie can address questions on the air that are submitted either in advance or during the live show via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

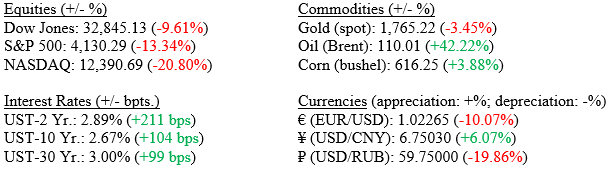

Last week, the markets were torn between the FED’s message on Wednesday, continued inflationary pressures and weak economic growth data, yet for all the uncertainty, Wall Street posted a positive week overall. For the week, the Dow Jones Industrial Average rose +3.0%, the S&P 500 Index increased by +4.3%, and the tech-heavy NASDAQ moved higher by +4.7%. Continuing its month-long rally, the 10-Year U.S. Treasury Bond fell another 10 basis points during the week, to close at 2.67%; quite an unusual feat considering that the FED is technically in a tightening (moving interest rates higher) cycle. The yield curve continued its inverted stance and GDP figures released last week confirmed that we saw two back-to-back quarters (albeit very modest dips) of negative GDP (economic growth).

Markets (as of 7/29; change YTD)

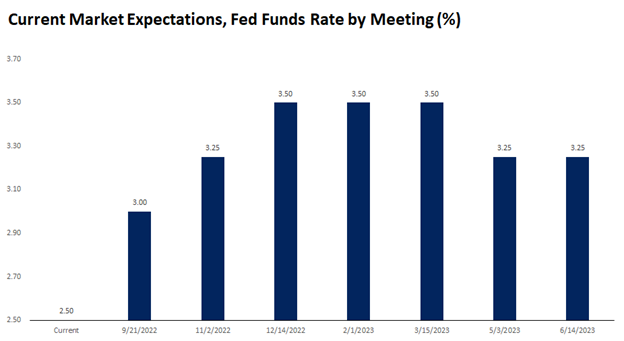

Global Economy At last week’s FOMC meeting, the Federal Reserve raised rates by 75 basis points (0.75%), bringing the benchmark fed funds rate to 2.50%, the highest level since 2019. Fed Chair Jerome Powell noted in his commentary that the fed funds rate is now close to the Fed’s estimate of a neutral rate, indicating an official end of the post-pandemic easy money policy. Chairman Powell also noted that by the end of the year, fed funds could be at their terminal rate of 3.00% to 3.50%. There may only be one or two more rate hikes this year thereby slowing or ending this tightening cycle. Chart 1 below from FactSet shows the current market expectations by Fed meeting date. Importantly, as early as March 2023, we could see rate cuts as the Fed begins to deal with slowing economy.

As noted above, the markets ended the week, and the month, with strong gains. Clearly, the markets are banking on a Fed pivot (moving from tightening or raising rates, to easing or lowering rates). GDP figures released last week for the second quarter 2022 showed -0.90%, and when combined with the first quarter of 2022 at -1.60%; showed we have a “technical” recession in place – which economists historically cited two back-to-back quarters of negative GDP signaled a recession. The GDP data is accurate and when combined with many recent missed EPS releases by companies such as Intel and Proctor & Gamble certainly point to a slowing economy, which goes into the Fed’s decision to consider a pivot sometime in late 2022-23. A pivot means lower interest rates in the future and that is what the markets are rallying on. Chart 2 (from FactSet) shows the broad performance of several major indexes thus far in the 3rd Quarter 2022. Every sector is higher, led by the NASDAQ.

Policy and Politics The markets are banking on the Fed doing its job in combating inflation, however we have yet to see any indication that inflation is moderating except in lower commodity prices as we discussed last week. For the markets to continue their recovery, we must see some real impact on the inflationary pressures impacting consumers. Note that gasoline prices are well off their highs of $4.50-5.00/gallon, and this is a commodity that immediately impacts all consumers. Further downward pressure on gasoline could be seen in the months ahead as global economies cool and demand for oil lessens.

What to Watch

August 4th U.S. Initial Jobless Claims estimate +249,000 vs prior month +256,000

August 5th U.S. Non-farm payrolls estimate +250,000 vs prior month of +372,000

August 5th U.S. Unemployment rate estimate 3.6% vs prior rate of 3.6%

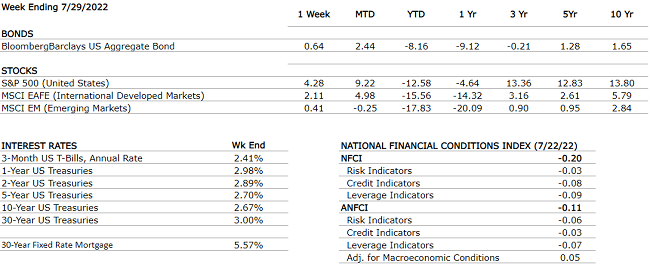

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Q1 2022 Real GDP shrunk at a 1.5% annual rate according to the second estimate. The main factors that resulted in a decrease in GDP were a surge in imports and trade deficit highlighting that the U.S. is buying more goods from foreign countries. Real GDP for Q2 2022 decreased at an annual rate of 0.9% marking the second consecutive quarter of declining GDP.

CORPORATE EARNINGS

NEUTRAL

The estimated growth rate for Q2 2022 is now 6.0% (up from 4.3%) which would mark a new post-pandemic low; but still solidly in the “growth” stage. 56% of S&P500 companies have now reported earnings — 73% beat earnings estimates and 66% reported actual revenue above expectations. For Q3, 28 companies issues negative EPS guidance while 17 companies issued positive guidance.

EMPLOYMENT

POSITIVE

Total nonfarm payroll employment rose by 370,000 in June and the unemployment rate remained constant at 3.6%. Job growth was widespread, led by gains in leisure and hospitality, manufacturing, and transportation and warehousing. Employment in retail trade declined.

INFLATION

NEGATIVE

The annual inflation rate in the US accelerated to 9.1% in June, the highest since November 1981, from 8.6% in May and above forecasts of 8.8%. Core CPI increased by 5.9%, slightly below 6% in May, but above forecasts of 5.7%. The increase in CPI was driven by major surges in food and energy prices, as food costs rose by 10.4% and energy prices by 41.6%.

FISCAL POLICY

NEUTRAL

Senator Manchin and Majority Leader Schumer reached an agreement on the Inflation Reduction Act last Wednesday. If enacted, the bill will provide significant incentives to cut carbon emissions and promote renewable energy. It will also result in the largest increase in corporate tax in decades.

MONETARY POLICY

NEUTRAL

Last week the Fed hiked rates by 75 basis points, raising their target to a range of 2.25% to 2.5%. This decision had unanimous agreement by the 12 members of the rate-setting committee. In a statement, members of the committee acknowledged a slowdown in the economy over the last month in terms of spending and production despite strong jobs gains.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

Russia has defaulted on its debt as of Sunday, June 26th when the 30-day grace period on $100 million of interest payments expired. This is the first Russian default since 1918. Sanctions imposed by Western powers effectively isolated Russia and its financial system from Europe and the U.S. making it much harder for Russia to complete international financial transactions.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but the rising cost of oil due to the Russian- Ukraine war is likely to cause additional inflationary pressures not only on gasoline prices but also on many other goods and services. Starting in June, China has started to remove some restrictions in major cities to end the COVID-19 lockdown.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie can address questions on the air that are submitted either in advance or during the live show via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.