Chief Investment Officer, William Henderson, touches on his 2023 Outlook. Want to know more about what may be on the horizon for 2023? Tune in to “Your Financial Choices” on Wednesday, January 18, 2023.

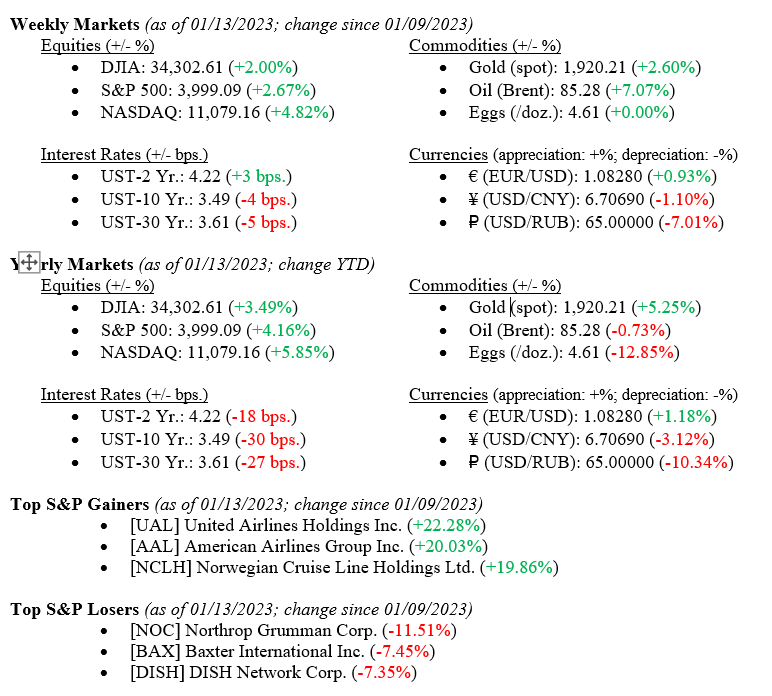

All major market indices traded higher last week as weaker-than-expected inflation data ramped up hopes by investors that the Fed’s Federal Open Market Committee would only raise the central bank’s key lending rate by just 0.25% rather than 0.50% or 0.75% that previous markets were predicting. The Dow Jones Industrial Average rose +2.0%, the S&P 500 Index rose +2.7%, and the tech-heavy NASDAQ rose by +4.8%. (See additional specific returns below.)

The hopes for a slower pace of rate increases came as data showed the U.S. consumer price index rose 6.5% year over year in December, paring from a year-over-year increase of 7.1% in November and a peak increase of 9.1% in June. The core U.S. consumer price index, which excludes food and energy prices, rose 5.7% year over year in December, down from a 6% increase in November.

Several major banks, including JP Morgan Chase, continue to beat the drum for a recession in 2023, while other major investment banks, such as Goldman Sachs, are not calling for a recession in 2023. We at VNFA continue to believe that the economy, consumers, banks, and corporations exhibit growth, balance sheet strength, and earnings growth, but admittedly, slower earnings growth. Lastly, labor continues to show near-record strength, with the unemployment rate hitting 3.5%, a 40-year low.

What to Watch

U.S. Producer Price Index Year over Year for December 2022, released 1/18/2023, (Prior 6.25%)

U.S. Housing Starts for December 2022, released 1/19/2023, (Prior 1.427M)

U.S. Job Openings: Total Nonfarm for December 2022, released 1/20/21, (Prior 10.46M)

The Q4 earnings reporting season will also move into full swing this week, and earnings are a good predictor of growth in 2023. Companies expected to release quarterly results next week include Morgan Stanley (MS), Goldman Sachs (GS), United Airlines (UAL), Charles Schwab (SCHW), Alcoa (AA), Procter & Gamble (PG), Netflix (NFLX), and Schlumberger (SLB). These firms are a good indicator of future market expectations and represent a wide dispersion across industrial and banking sectors.

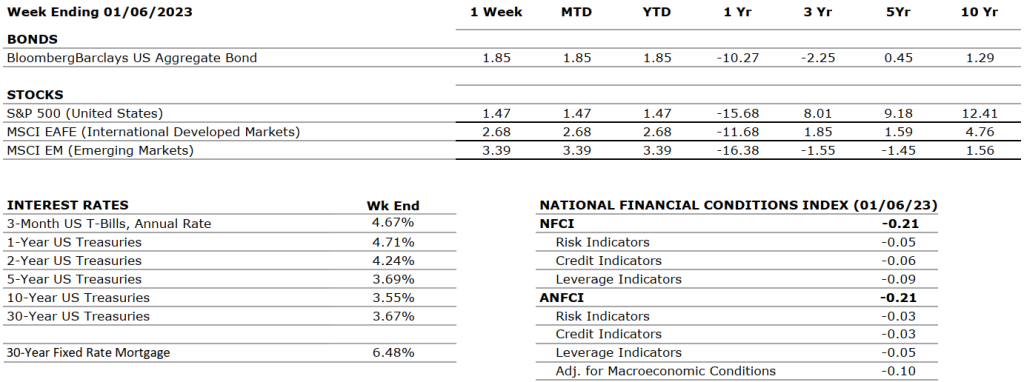

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Real gross domestic product (GDP) increased at an annual rate of 3.2 percent in the third quarter of 2022, in contrast to a decrease of 0.6 percent in the second quarter. The third quarter’s increase primarily reflected exports and consumer spending that were partly offset by a decrease in housing investment. The estimated growth rate for Q4 2022 Real GDP is now 3.8%.

CORPORATE EARNINGS

NEUTRAL

The earnings growth rate for Q3 2022 was 2.4%. For Q4 2022, earnings are expected to decline by -3.9%, down from the previous estimate of -2.8%. This would be the first negative growth since Q3 2020 (-5.7%). So far, 29 S&P 500 companies have reported earnings, with 23 companies beating EPS estimates and 20 beating revenue expectations.

EMPLOYMENT

NEUTRAL

U.S. Nonfarm Payrolls for December 2022 increased by 223,000, and the unemployment rate fell slightly to 3.5% from 3.7%. Leisure and hospitality, health care, construction, and social assistance were among the sectors with the most notable gains.

INFLATION

NEGATIVE

The annual inflation rate in the U.S. increased by 6.5% for December 2022 compared to the November reading of 7.1%. This is the lowest CPI value since October 2021. Core CPI rose to 5.7% versus 6.0% in November. Most prices fell during the last month of the year, including food, used cars, and most energy sources. Electricity and shelter still saw an increase from the previous month.

FISCAL POLICY

NEUTRAL

Senator Manchin and Majority Leader Schumer agreed on the latest tax and energy bill with incentives for green energy, electric cars, and oil & gas companies for exploration. No changes in private equity taxes or higher tax rates for the very wealthy were enacted. The Senate has officially passed the bill. President Biden announced student loan forgiveness of up to $20,000, subject to income limitations.

MONETARY POLICY

NEGATIVE

Last month the Fed approved a 50-bps rate hike after four consecutive 75-bps hikes taking its target range to 4.25%-4.50%. Although the magnitude of rate hikes has been decreased, rates are likely to be kept higher through 2023 with no reductions until 2024. According to the FOMC’s dot plot, the expected terminal rate is now 5.1%. The next meetings will be held on at the end of January and the beginning of February.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

While the Russian-Ukraine conflict does not show signs of abating, additional geopolitical issues have arisen in South America with the violent protests that hit the capital of Brazil last week. Following the October 2022 elections won by the left party, Jair Bolsonaro’s far-right supporters stormed Brasilia accusing the winning candidate and party of corruption. Bolsonaro is currently in Florida and has not communicated little publicly.

ECONOMIC RISKS

NEGATIVE

China has abandoned its zero-Covid policy, which should help the global supply chain recover. Gas supplies from Russia to Europe have decreased by 88% over the past year, and EU countries have agreed to cut gas usage by 15% as gas prices have more than doubled. Nevertheless, an unusually mild winter has helped most of Europe deal with increased energy costs.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

According to the IRS, one of the first decisions taxpayers must make when completing a tax return is whether to take the standard deduction or itemize their deductions.

When starting the tax process, there are several factors to consider before making a choice, including changes to your tax situation, changes to the standard deduction amount, and recent tax law changes.

Want to learn more on Tax deductions, visit the IRS Tax Basics.

Tune in Wednesday, 6 PM “Your Financial Choices” on WDIY 88.1FM. Laurie and her guest Bill Henderson, Chief Investment Officer at Valley National Financial Advisors will be discussing: The 2023 Outlook.

The Martin Luther King, Jr. holiday is the only federal holiday designated as a National Day of Service? Each year Americans across the country use MLK Day of Service as an opportunity to volunteer and improve their communities. Want to learn more about Martin Luther King, Jr., National Day of Service, visit United We Serve.

Important Reminder: January 16, VNFA offices will be closed for Martin Luther King Jr. Day.

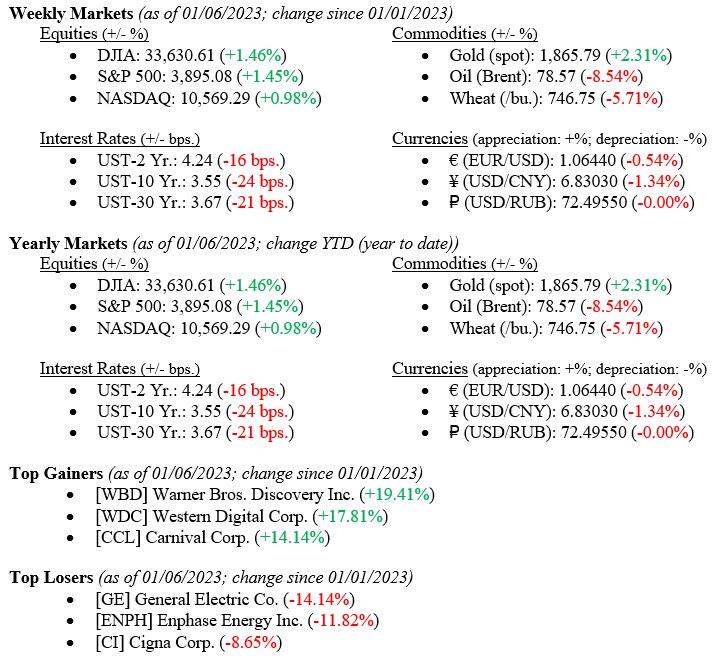

On Friday, a solid jobs report by the BLS (Bureau of Labor Statistics) pushed equity on bond markets higher as investors hung new hopes for an economic soft landing in 2023 rather than a Fed-induced recession. The economy added 223,000 jobs in December, beating consensus expectations and continuing the string of strong payroll gains. Further, job openings, a measure the Fed pays close attention to, stayed elevated. For the week ended January 6, 2023, the Dow Jones Industrial Average and the S&P 500 Index closed higher by +1.5%, while the NASDAQ moved higher by +1.0%. Lastly, the 10-year US Treasury fell a stunning 24 basis points to close the week at 3.55%.

Economy

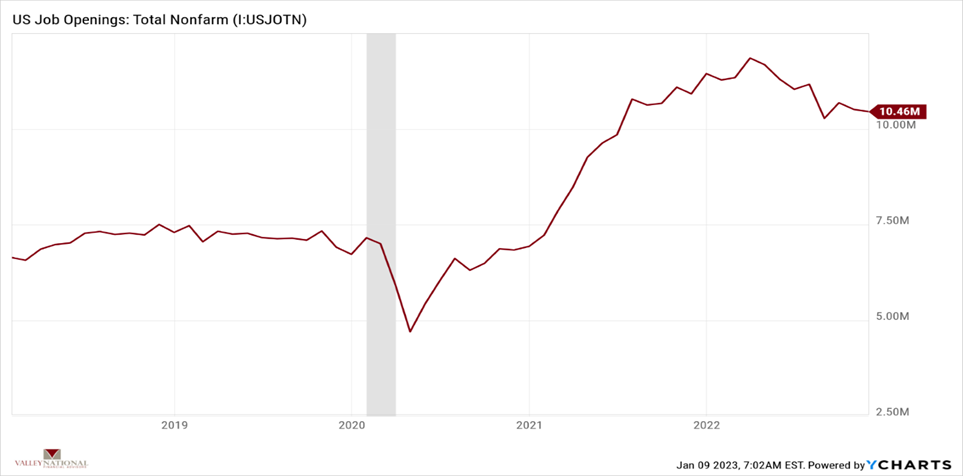

As mentioned, the BLS reported a strong number of jobs, and job openings also remained elevated. The unemployment rate fell to 3.5%, presenting yet another piece of stubborn employment data. Chart 1 below from Valley National Financial Advisors and Y Charts shows job openings are elevated and elevated not just from the pandemic period of 2020 but also from the pre-pandemic period before 2020. Although many companies are announcing job cuts, especially in technology (Amazon) and banking (Goldman), these industries also hired many employees during and after the pandemic, giving them reasonable amounts of job cuts to make without impacting the overall employment picture. The combination of elevated job openings and low unemployment dims the prospects for a hard landing (aka recession) in 2023.

Policy and Politics

Republican Representative Kevin McCarthy was elected Speaker of the House in a near-record set of 15 elections before the conclusion on January 7, 2023. The election was less critical than the November 2022 election. At that point, the Republicans took control of the US House of Representatives and thereby set a firmly divided government in place for at least two years. Historically, markets like a divided government for the sole reason that nothing drastic can happen that would impact the business environment. It is too early to see which direction our divided government will take, but we take solace in the fact that there are strong checks and balances.

What to Watch

U.S. Inflation Rate for December 2022, released 1/12/23, (Prior 7.11%)

U.S. Core Consumer Price Index Year Over Year for December 2023, released 1/12/23, (Prior 5.96%)

U.S. Index of Consumer Sentiment for January 2023, released 1/13/23, (Prior 59.7)

Markets are off to a good start thus far in 2023. Still, a week does not make a year, and uncertainty remains with the Fed, China’s reopening, the Russia/Ukraine War, ongoing painful inflation, and the long-running inverted yield curve in the U.S. Treasury market has historically preceded a recession. In the face of this uncertainty, we have conflicting employment information that shows layoffs by many companies while job openings remain high and unemployment remains low. Inflation continues to be the Fed’s primary concern, and we expect further rate hikes in 2023. We also expect the pace, tenor, and size of those rate hikes to soften as Chairman Powell balances higher rates with inflation and prospects for a recession. Lastly, wage growth, while moderate recently, is keeping consumers healthy. When you add in bank balance sheet health and corporate earnings growing modestly, it is difficult to see a recession in 2023 and much easier to see the hoped-for “Soft Landing.”

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Real gross domestic product (GDP) increased at an annual rate of 3.2 percent in the third quarter of 2022, in contrast to a decrease of 0.6 percent in the second quarter. The increase in the third quarter primarily reflected increases in exports and consumer spending that were partly offset by a decrease in housing investment. The estimated growth rate for Q4 2022 Real GDP is now 3.8%.

CORPORATE EARNINGS

NEUTRAL

The earnings growth rate for Q3 2022 was 2.4%. For Q4 2022, earnings are expected to decline by -4.1%, down from the previous estimate of -2.8%. This would be the first negative growth since Q3 2020 (-5.7%). So far, 20 S&P 500 companies have reported earnings, with 15 companies beating EPS estimates and 13 beating revenue expectations.

EMPLOYMENT

NEUTRAL

U.S. Nonfarm Payrolls for December 2022 increased by 223,000, and the unemployment rate fell slightly to 3.5% from 3.7%. Leisure and hospitality, health care, construction, and social assistance were among the sectors with the most notable gains.

INFLATION

NEGATIVE

The annual inflation rate in the U.S. increased by 7.1% for November 2022 compared to the expected 7.3% — showing some continued signs of deceleration. Core CPI was also reported below expectations at 6.0% versus the estimated 6.1%. Although energy prices have come down, energy, along with food and shelter, are still the main contributors to inflation. December inflation data is set to be released this Thursday, 01/12.

FISCAL POLICY

NEUTRAL

Senator Manchin and Majority Leader Schumer reached an agreement on the latest tax and energy bill with incentives for green energy, electric cars, and conversely oil & gas companies for exploration. No changes in private equity taxes or higher tax rates for the very wealthy were enacted. The bill has been officially passed by the Senate. President Biden announced student loan forgiveness of up to $20,000 subject to income limitations.

MONETARY POLICY

NEGATIVE

Two weeks ago the Fed approved a 50 bps rate hike after four consecutive 75 bps hikes taking its target range to 4.25%-4.50%. Although the magnitude of rate hikes has been decreased, rates are likely to be kept higher through 2023 with no reductions until 2024. According to the FOMC’s dot-plot, the expected terminal rate is now 5.1%.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

Russia held controversial referendums for the annexation of four Ukrainian regions and the Russian Parliament unanimously recognized these regions as part of Russia. Ukraine and Western countries have condemned these actions by Russia by declaring them illegitimate and illegal.Additional sanctions are being imposed on Russia by many countries.

ECONOMIC RISKS

NEGATIVE

China seems to have abandoned its zero-Covid policy, which should help the global supply chain recover. On the other hand, the Russian-Ukraine war does not show signs of abating. Gas supplies from Russia to Europe have decreased by 88% over the past year, and EU countries have agreed to cut gas usage by 15% as gas prices have more than doubled. The U.S. is now dealing with a significant diesel shortage, with national reserves at their lowest levels since 1951 and a ban on Russian products that will intensify the issue.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.