There is still time to support WDIY 88.1 FM and Second Harvest Food Bank of Lehigh Valley and Northeast Pennsylvania. Valley National Financial Advisors will continue their support to provide meals through Second Harvest Food Bank.

Donate by calling WDIY at 610-758-8810 or completing the Donation Form online. Visit WDIY to learn more and get involved.

Financial Planning Month is indeed an excellent opportunity to emphasize the importance of financial planning and empower individuals and families to secure their financial futures. Here are some valuable financial planning tips from expert Laurie A. Siebert, CPA, CFP®, AEP®.

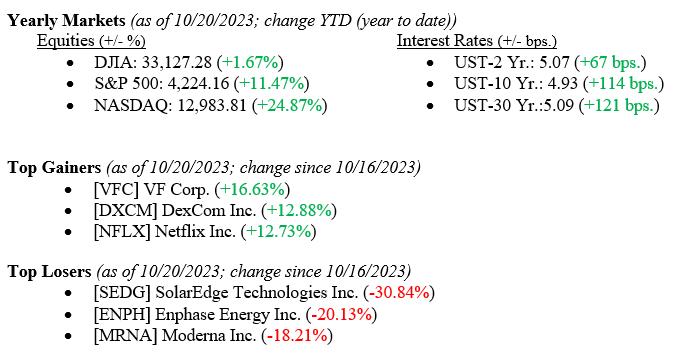

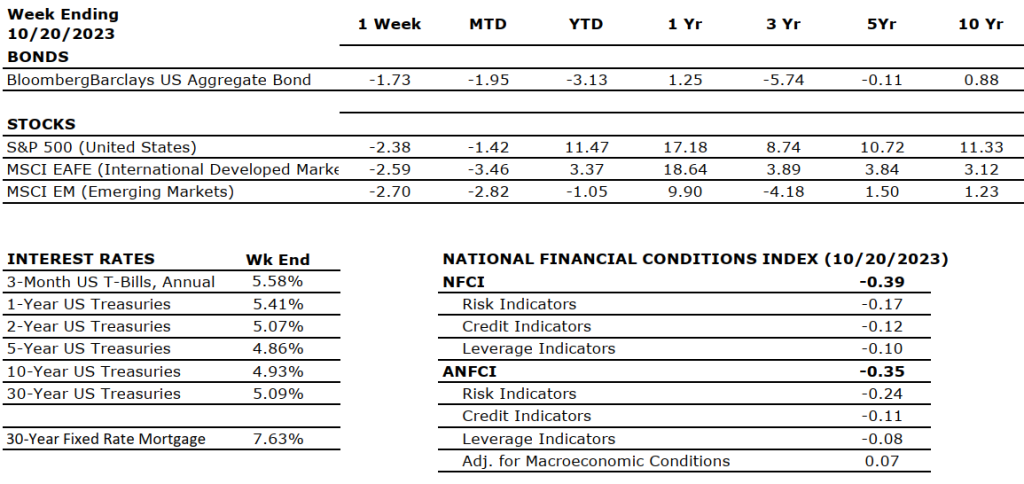

All three major market indexes posted heavy losses for the week, with the Dow Jones Industrial Average falling –1.6%, the broader S&P 500 Index falling –2.4%, and the tech-heavy NASDAQ falling –3.2%. A flurry of uninspiring earnings releases, higher bond yields, and continued global unrest led to the losses. Bond yields meanwhile moved higher, with the yield on the 10-year U.S. Treasury rising 15 basis points to close the week at 4.93%. Early reports this week show a 10-year Treasury yield moving to 5.00%, a level not seen since 2007. Two weeks ago, in this report, we introduced three words in our commentary that we do not take lightly. The words were turmoil, fear, and uncertainty. In this week’s report, we unpack those words and explain why we remain concerned.

Global Economy

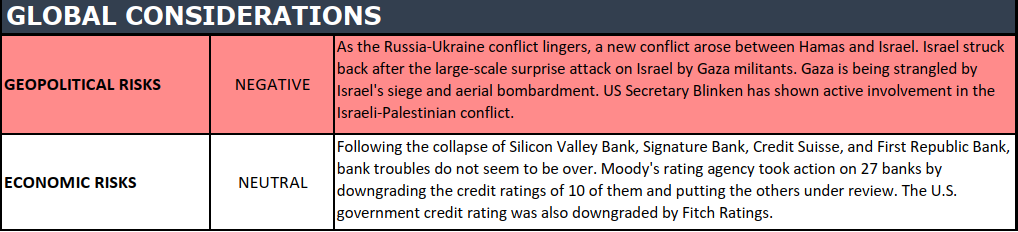

The global economy is where turmoil firmly falls on the markets. The Israel/Hamas war continues without any view to a swift or less costly end to the conflict. The Middle East has rarely been a calm place, but relations have certainly been better than they are now among members of the region. For obvious reasons, oil markets and global trade rely on relative calm in the region – major oil producers are located here, and trade through the Suez Canal is a critical route for Asia/Europe trade. The Israel/Hamas War piles onto the Russia/Ukraine War and the China/Taiwan concerns. Hence, our use of the word turmoil – “a state of great disturbance or confusion.”

Policy and Politics

The second word we introduced is fear. Why fear? For the first time in many years, investors are fearing the Fed instead of welcoming the Fed and their concomitant market actions. Last week, in a speech to the Economic Club of NY, where we have two Valley National Group investment associates present, Fed Chairman Powell danced around the future path or direction of interest rates, pointing instead to the data as his compass for what the Fed will do next. Investors hoped to hear language stating that future rate hikes were off the table, but that was not the case in both fixed-income and equity markets sold off because everyone was still waiting for the classic Fed Put. The Fed Put happens when markets expect and price in lower interest rates, not higher ones. So, instead of welcoming Fed actions, markets fear future Fed actions. We believe that the economy remains healthy, which is most evident in the consumer who continues to spend. The labor market, where unemployment remains at a near-record low level of 3.8% and housing, while slower, continues to exhibit resilience.

What to Watch

Merger activity – there are two major M&A (merger & acquisition) deals on the table right now: Exxon/Pioneer Natural Resources and Chevron/Hess. These mega-billion-dollar mergers provide much needed fuel and profits to Wall Street where M&A and IPOs have been quiet recently.

U.S. Single Family Houses sold for September 2023, released 10/25/23, prior 675k.

U.S. Real GDP QoQ for 3rd Quarter 2023, released 10/26/23, prior +2.1%

U.S. Personal Consumption Expenditure Index YoY for September 2023, released 10/27/23, prior 3.48% (Fed’s favored inflation indicator)

U.S. Index of Consumer Sentiment for October 2023, released 10/27/23, prior level of 63.

We chose the summary for the week to discuss our third word – uncertainty. We have discussed markets hating uncertainty the most out of all worrisome trends. Typically, in a market where fear and turmoil exist, investors are uncertain, and their natural reaction is a flight to quality, which means buying U.S. Treasuries. However, U.S. Treasuries continue to sell off as the Federal Reserve’s surge in debt supply and mixed signals on the rate path weaken fixed-income markets. Furthermore, our leaders in Washington continue to do nothing as they wrangle to simply fill the U.S. Speaker of the House position, notably the third position in line for succession to the U.S. President.

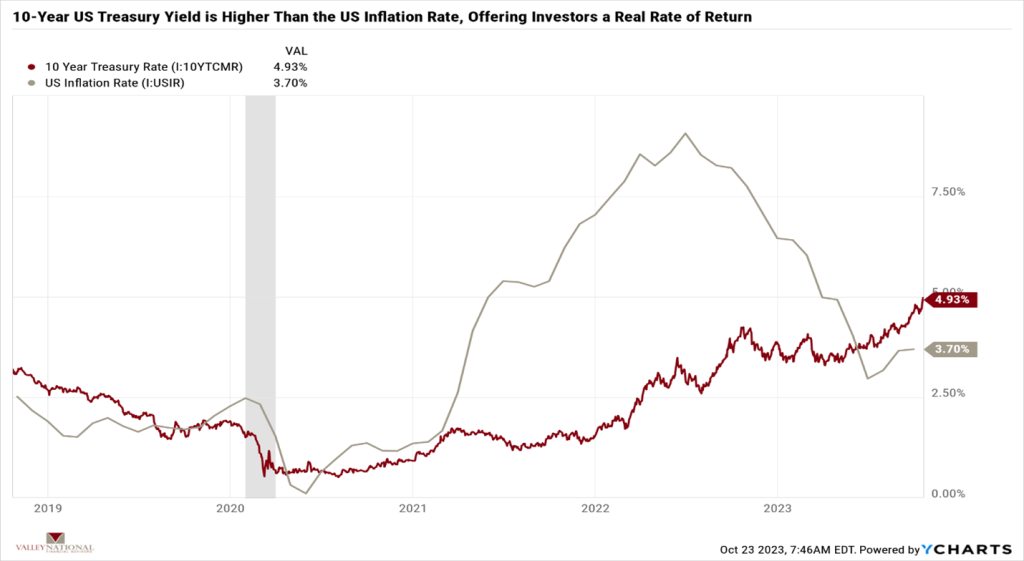

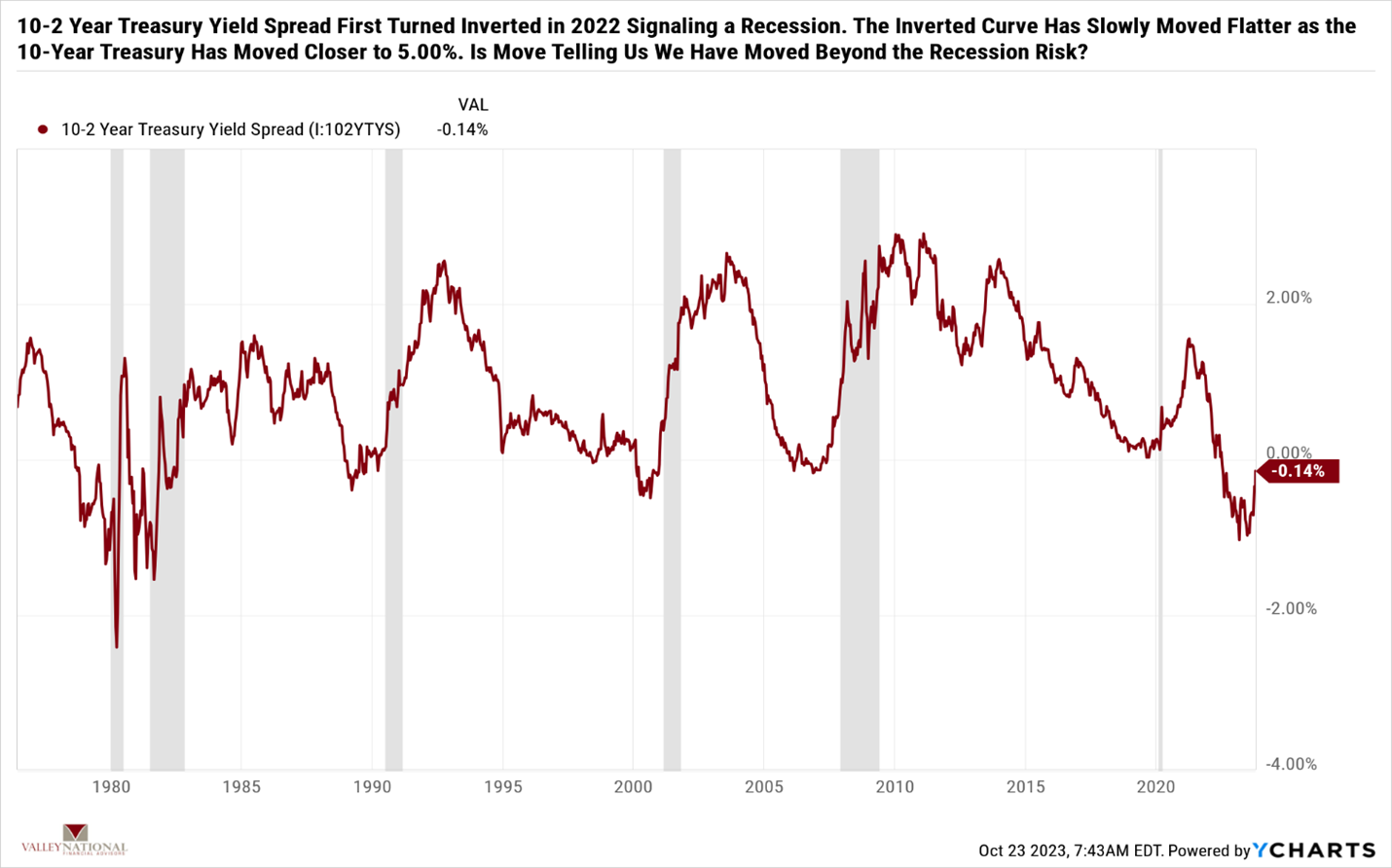

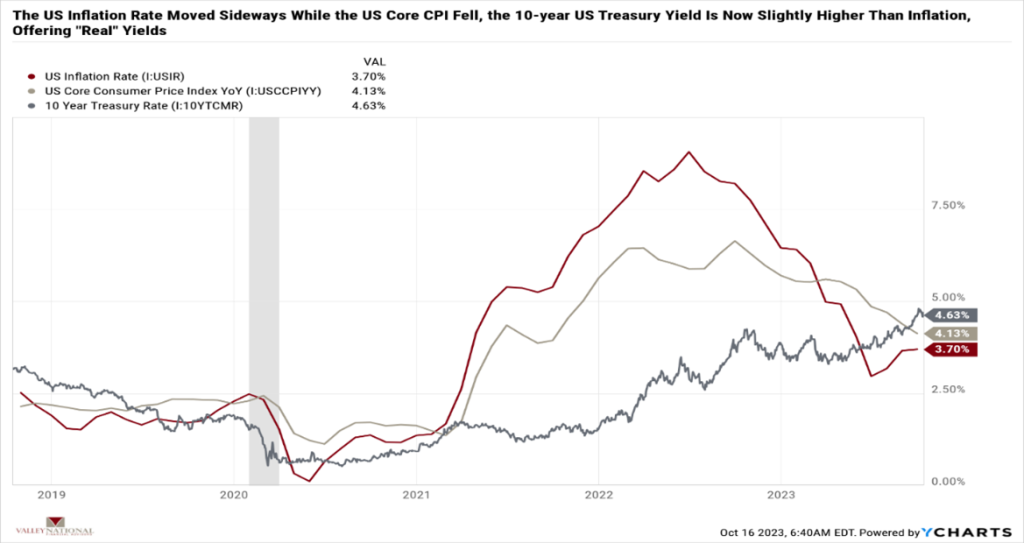

Uncertainty persists in our leaders, world politics, and the markets, so while it is not unusual for markets to sell off, it is unusual to see such a connected and broad sell-off in all markets in tandem. Treasuries at 5.00% offer investors real after inflation yields. See charts 1 & 2 above by Valley National & Y Charts showing first the U.S. Inflation rate and the 10-year U.S. Treasury yield and second the 10-2-year Treasury Yield Spread.

We expect to see turmoil, fear, and uncertainty in the market until each issue gets resolved over time, and time is always on the patient investors’ side. The patient investor can outlast uncertainty. Reach out to your advisor at Valley National Financial Advisors for advice or questions.

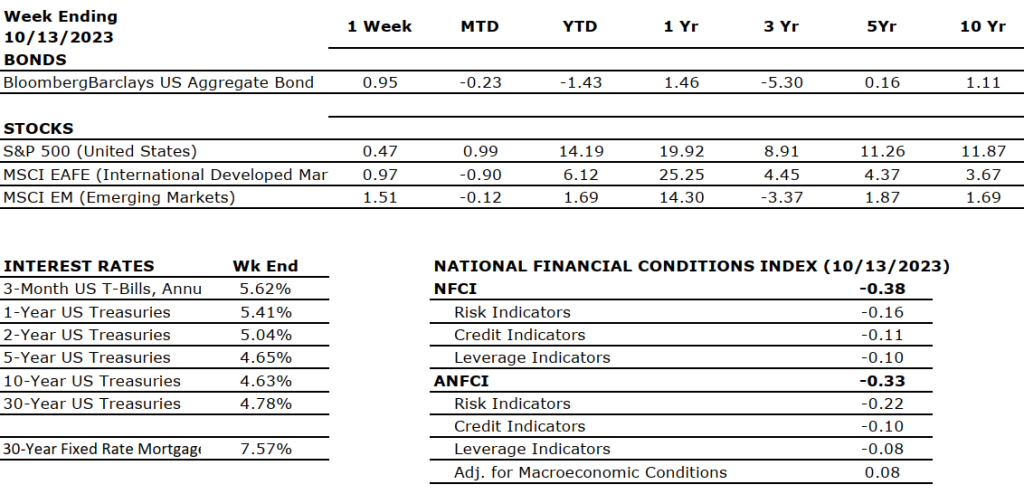

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

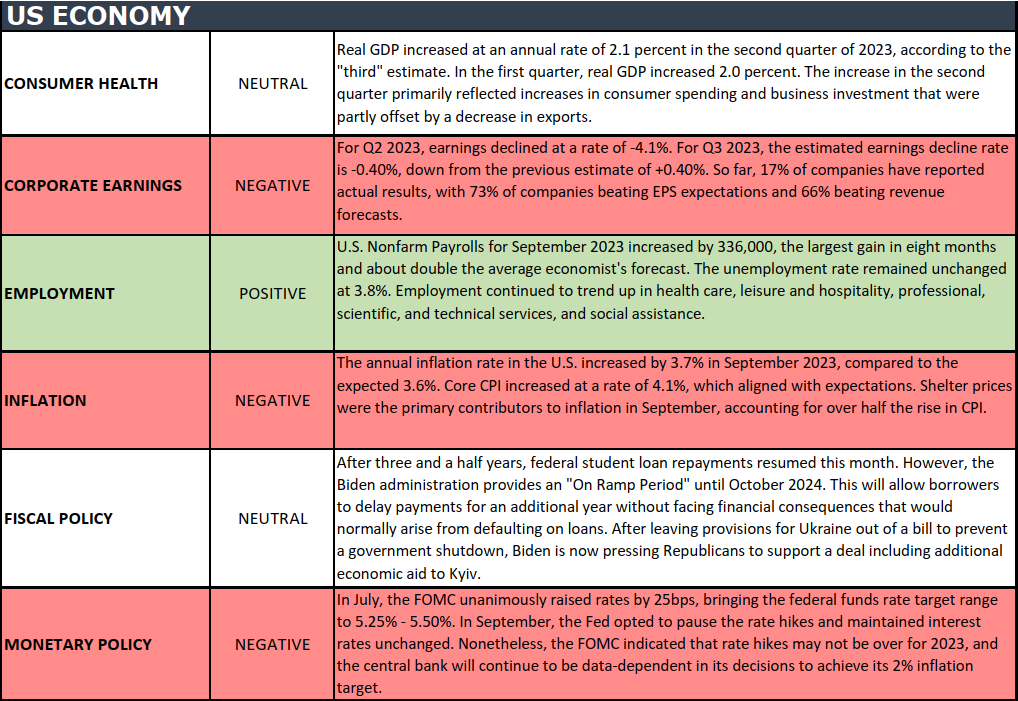

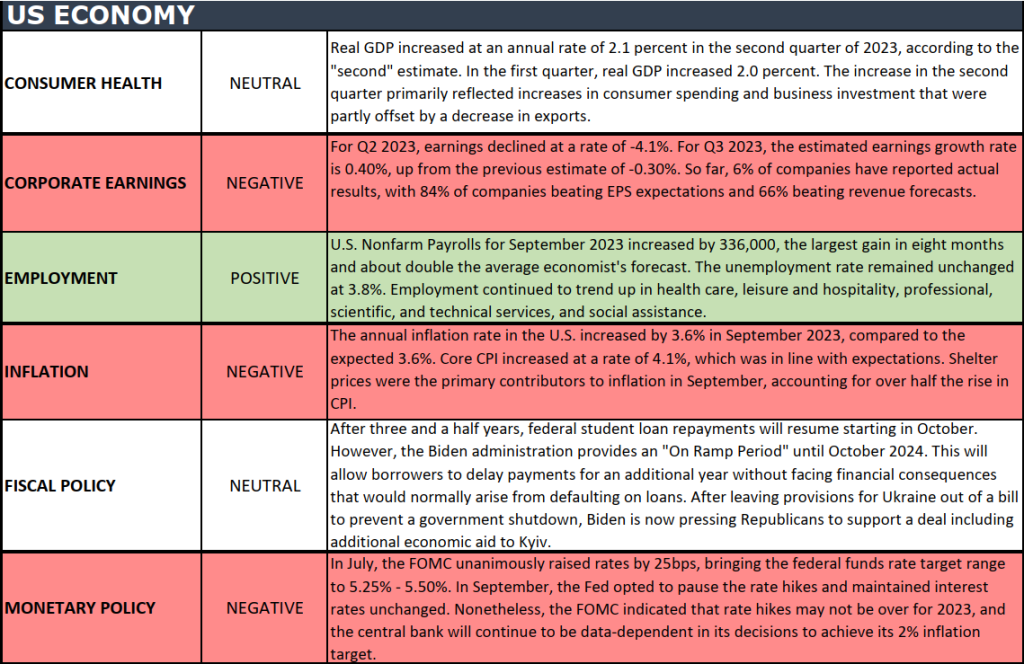

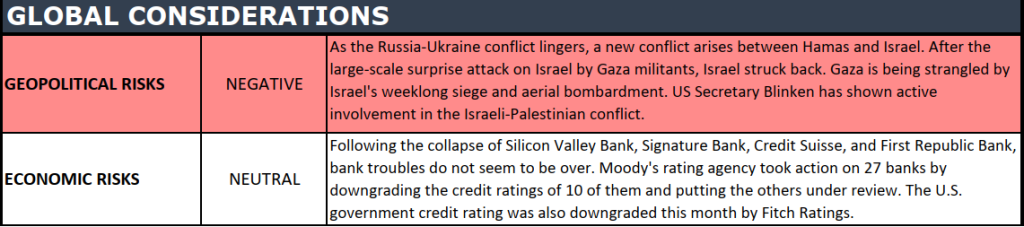

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Financial Planning Month is indeed an excellent opportunity to emphasize the importance of financial planning and empower individuals and families to secure their financial futures. Here are some valuable financial planning tips from experts Rodman D. Young, CPA, CFP ® and Jaclyn M. Cornelius, CFP®, EA.

The broader markets rallied last week, seeing through the noise of continued inflation concerns, a protracted war in the Middle East, and mixed third-quarter corporate earnings releases. Last week, the Dow Jones Industrial Average and the S&P 500 Index moved +0.79% and +0.45%, respectively, while the NASDAQ moved lower by –0.18%. In a classic “Flight-to-Quality” trade, U.S. Treasury bond yields fell as investors moved to safe Treasuries during a time of global conflict. The 10-year U.S. Treasury bond fell 15 basis points, ending the week at 4.63%. Even at this lower yield, investors are finally seeing “real” yields on Treasuries as the U.S. Inflation Rate has finally fallen lower than the 10-year U.S. Treasury bond yield. See Chart 1 from Valley National Financial Advisors and Y Charts.

US Economy

As mentioned above, while stubbornly staying above the Fed’s target rate of 2%, the U.S. Inflation Rate is now 3.70% (released last week). The U.S. Core CPI (Consumer Price Index) fell to 4.13% in September 2023 from 4.39% in August 2023. Chart 1 below shows the 10-year U.S. Treasury and two inflation measures. While inflation remains higher, the yield on the 10-year Treasury is slightly higher, thereby finally offering investors real, after-inflation returns.

Higher interest rates continue to negatively impact growth stocks as those companies typically borrow money to expand operations or hire additional employees. As third-quarter earnings releases hit the tape, we will get a better picture of which firms and industries are best dealing with higher interest rates for longer. Large banks Citigroup, JP Morgan, and Wells Fargo all reported earnings better than expected as higher interest rates helped these banks as they continue to remain a bit stingy in passing on the higher rates to their depositors.

A widening or global escalation of the Israel-Palestinian conflict could impact oil prices, but thus far, world oil prices have not been materially impacted. It is important to watch this event to see how various actors on the world stage choose sides. For example, the U.S. has moved the USS Gerald Ford carrier fleet to the region to support Israel. Of course, defense stocks (ex. Northrop Grumman, General Dynamics & Lockheed Martin) have modestly rallied because of the growing conflict.

Policy and Politics

Three government forces are working in the economy right now, and all are impacting the markets, pushing uncertainty and worry into prices:

We have the Fed and its constant fight against inflation. Last week, Federal Reserve Bank Vice Chairman Philip Jefferson noted that higher long bond yields are doing a lot of the work for the Fed in slowing the economy, implying that there is no need for further rate hikes.

U.S. Secretary of State Anthony Blinken is actively involved in the Israeli-Palestinian conflict, which clearly indicates the U.S. is willing to do whatever is necessary to support our allies in the region.

We continue to see a circus in Washington, DC, as lawmakers fall over each other trying to elect a new U.S. Speaker of the House.

Taken together, these government forces are adding uncertainty and worry to the markets, which is quite the opposite of what we expect and desire from our leaders.

What to Watch

• U.S. Retail Gas Price for week of October 13, 2023, released 10/16/23, prior price $3.81/gallon. • U.S. Housing Starts for September 2023, released 10/18/23, prior 1.283 million starts. • U.S. Initial Claims for Unemployment for week of October 14, 2023, release 10/19/12, prior 209k • 30 Year Mortgage Rate as of October 19, 2023, released 10/19/23, prior 7.57% • Key Earnings releases to watch this week: Tesla, Netflix, Goldman Sachs, Lockheed Martin.

We pointed out the wall of worry above with confusion on interest rates, continuing global conflict, and a broken U.S. Congress. Meanwhile, the markets are moving slightly higher each week, and bonds finally offer “real” yields for investors. Instead of worrying about what is happening now, the markets are scaling the wall of worry and moving higher as they filter out the noise and see sectors like big tech, healthcare, and mega banks doing well, even given all the noise. It is easy to get mired down with worry and negativity – that is all we see on TV and hear from so-called experts, but the markets see the future and ignore the noise. Investors interested in creating long-term generational wealth should listen to the markets and ignore the TV. Reach out to your financial adviser at Valley National Financial Advisors for advice or questions.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.