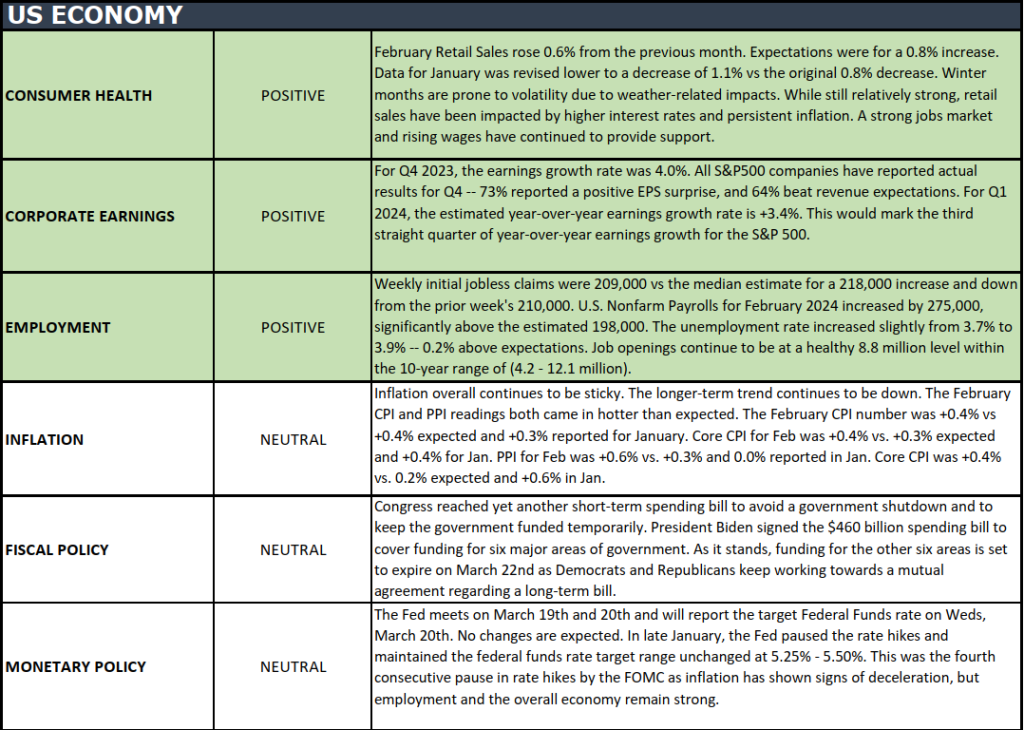

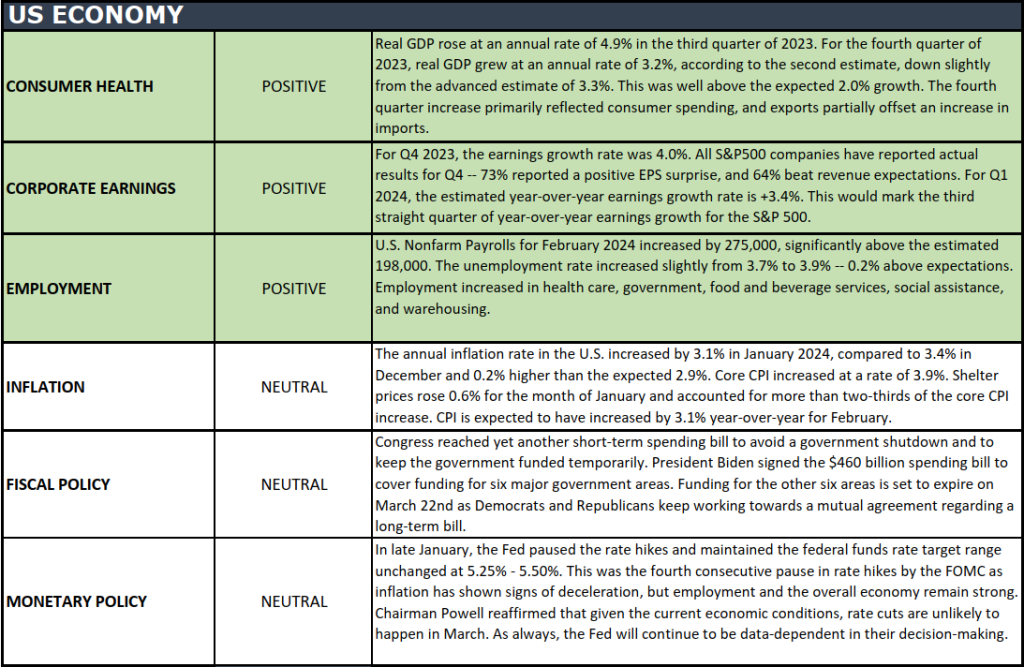

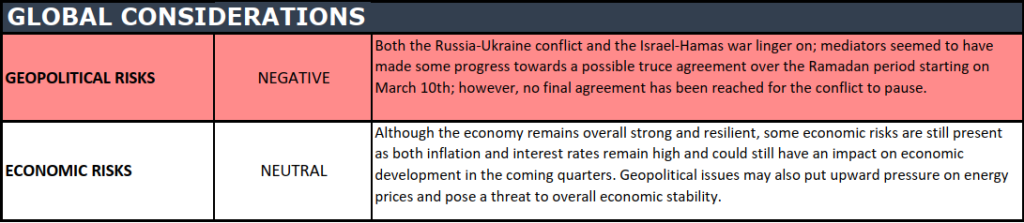

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

“If we had no winter, the spring would not be so pleasant: if we did not sometimes taste of adversity, prosperity would not be so welcome.” -Anne Bradstreet

Join us in welcoming Christopher Holland to the newly created Director of Research & Investments position!

Chris brings an extensive wealth of experience to our team, showcasing a remarkable career spanning over 25 years. Most recently, he dedicated his expertise to private market investing as a Senior Investment Professional with the Public-School Employee Retirement System. Chris has held distinguished roles, including Managing Director at Galt’s Gate and Senior Equity Analyst/Portfolio Manager at Delaware Funds by Macquarie. His contributions also extend to his time as a Municipal Credit Analyst at BlackRock. His impressive background reflects a consistent track record of successfully steering research and investment initiatives to fruition.

“Chris’s role will be instrumental in shaping our research initiatives and driving investment strategies, contributing significantly to the success and growth of VNFA. His strategic acumen and proven accomplishments make him a valuable and timely addition to our investment team as we continue to navigate the ever-evolving landscape of the financial markets,” said William Henderson, Chief Investment Officer.

Anchored in the Lehigh Valley, Chris is a true Bethlehem native, born and raised. Beyond research and investments, he finds joy in skiing and working in his backyard vegetable garden. Chris is based out of our Bethlehem headquarters, and he can be reached at 610-868-9000 ext. 123 or cholland@valleynationalgroup.com.

What a great evening of community connection and culinary delights! Thank you, LINC & Butterhead Kitchen, for allowing #TeamVNFA to collaborate on this exceptional community cooking class. LINC’s mission, centered around fostering a sense of welcome and building a supportive community for newcomers, aligns seamlessly with VNFA’s values. We take immense pride in contributing to this remarkable mission, which is dedicated to assisting individuals in settling into the community and flourishing.

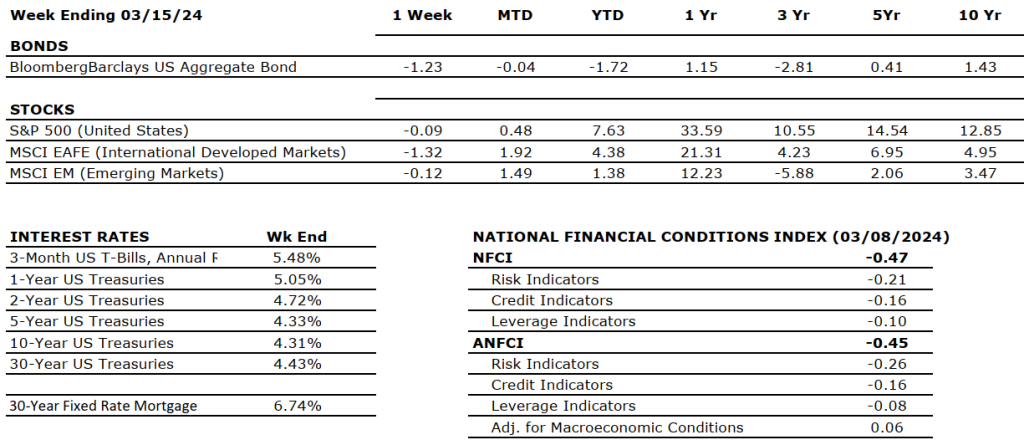

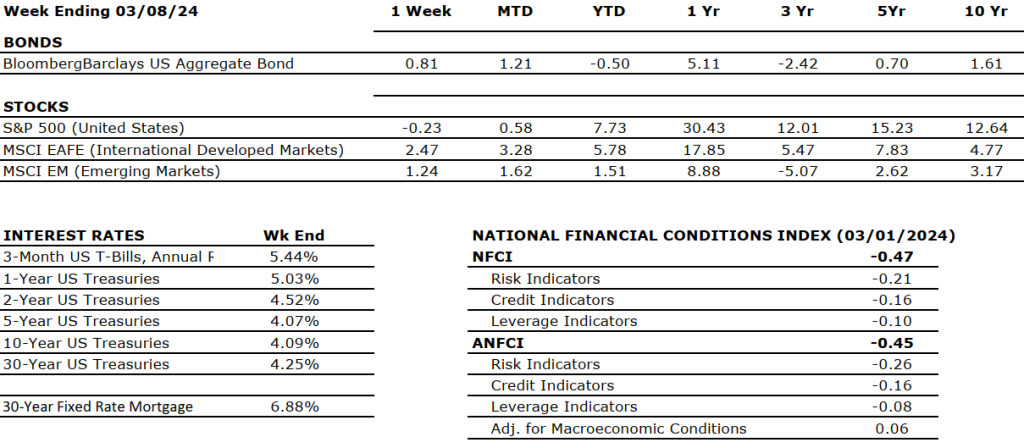

Equity markets were down last week, with all three major indexes reporting negative results. The S&P 500 Index fell –0.26%, the NASDAQ -1.17%, and the Dow Jones Industrial Average –0.93%. Fixed income markets saw lower yields last week as Fed Chair Powell gave an indication that rate cuts are “not far” off. Also impacting rates was the February jobs number, which showed lower wage pressure and revisions lower than the hot January jobs numbers. A big test for bond markets will come later this week when the CPI (Consumer Price Index) and PPI (Producer Price Index) numbers are reported for January. The 10-year U.S. Treasury bond yield fell 9.4 basis points last week to close at 4.09%.

U.S. Economy

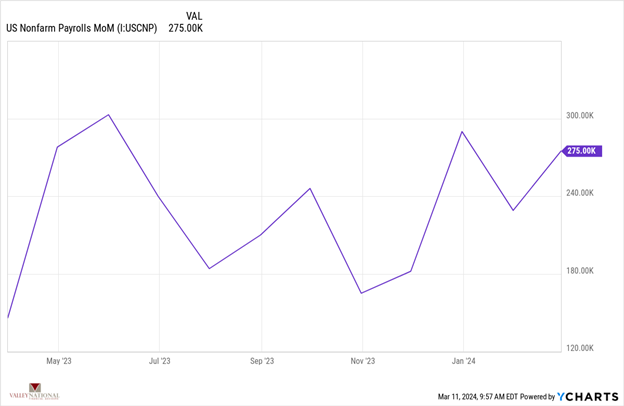

The February jobs report from Friday indicates job growth remains healthy, with nonfarm payrolls increasing 275,000 jobs, above consensus expectations for a rise of 198,000. This follows a downwardly revised 229,000 increase in January. Despite encouraging headline figures, prior estimates of job expansion in December and January were revised down to 167,000 jobs. The unemployment rate rose to a two-year high of 3.9%, and wage momentum cooled, indicating less inflationary pressure.

Policy and Politics

During testimony last week, Fed Chair Powell indicated a softening of banking rules, specifically stating that proposed new rules to force lenders to strengthen their balance sheets (Basel III) would be scaled back or reworked. This comes in response to complaints from industry leaders about the overall cost and economic impact of enacting the original proposed changes.

What to Watch This Week

U.S. Consumer Price Index released 3/12/24, prior +0.3%

U.S. Retail Sales released 3/14/24, prior –0.8%

U.S. Producer Price Index released 3/14/24, prior +0.3%

U.S. Consumer Sentiment (prelim) released 3/14/24, prior 76.9%

In the current market landscape, the stock market and the broader economy demonstrate robust performance buoyed by several factors. Healthy corporate earnings bolstered by resilient consumer spending, economic productivity gains, and increased business technology spending are driving equities to continued new highs. Additionally, recent data pointing to a soft landing for the economy continues to provide a supportive backdrop, instilling confidence among investors. With a healthy labor market combined with the prospects for lower rates later this year, the overall economic and market outlook remains optimistic. It should provide help to the housing market. However, prudent risk management and close monitoring of potential inflationary pressures, geopolitical tensions, and trade disputes remain essential. Overall, the positive momentum in both the stock market and the economy reflects a favorable environment for investors.

In navigating volatile markets, it is important to maintain a long-term perspective grounded in the fundamentals of the economy and industry-leading companies. While short-term fluctuations and unforeseen challenges may arise, staying committed to well-thought-out investment strategies is key. As we move forward, let us remain optimistic about the future and recognize that overly emotional markets often pave the way for opportunities and growth.

Tune in Wednesday, 6 PM, “Your Financial Choices” on WDIY 88.1 FM. Laurie will be discussing Listeners’ Tax Questions.

Questions can be submitted to yourfinancialchoices.com before the live show. Recordings of past shows are available to listen to or download at yourfinancialchoices.com and wdiy.org.

Did you miss the last show, 2024 Tax Planning Now? Listen Here

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

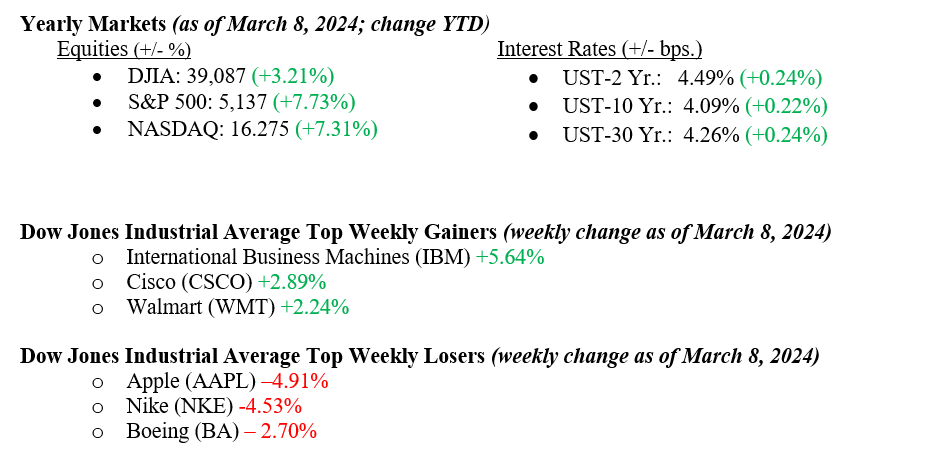

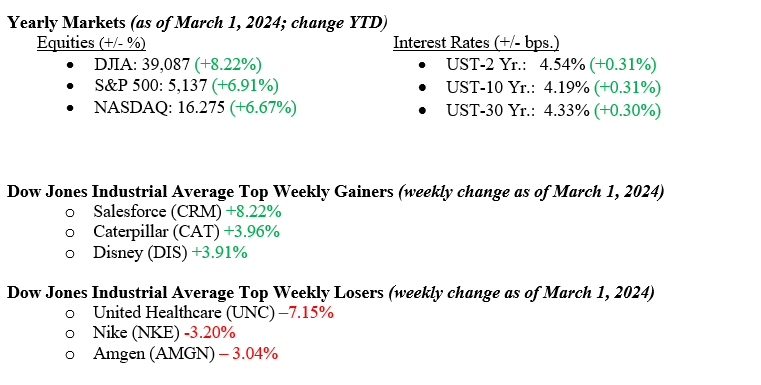

Equity markets were mixed last week, with two of the three major indexes reporting positive results and only the Dow Jones Industrial Average falling for the week. The S&P 500 Index rose +0.95%, the NASDAQ rose +1.74%, while the Dow Jones Industrial Average fell –0.11%. Critically important to a needed broadening in equity returns, the Russell 2000 Index of Small Capitalization stocks rose +3.00%. We do not typically report on the Russell 2000, but this week’s move higher has put some breadth into the market rather than keeping returns concentrated in the “Magnificent 7.” Concentrated markets tend to rise and fall quickly and are usually based on a small piece of information rather than sound fundamentals. Fixed-income markets were quiet last week as traders and markets have accepted that interest rate cuts by the Federal Reserve are further off than previously thought. The 10-year U.S. Treasury bond yield fell seven basis points to close the week at 4.19%.

U.S. Economy

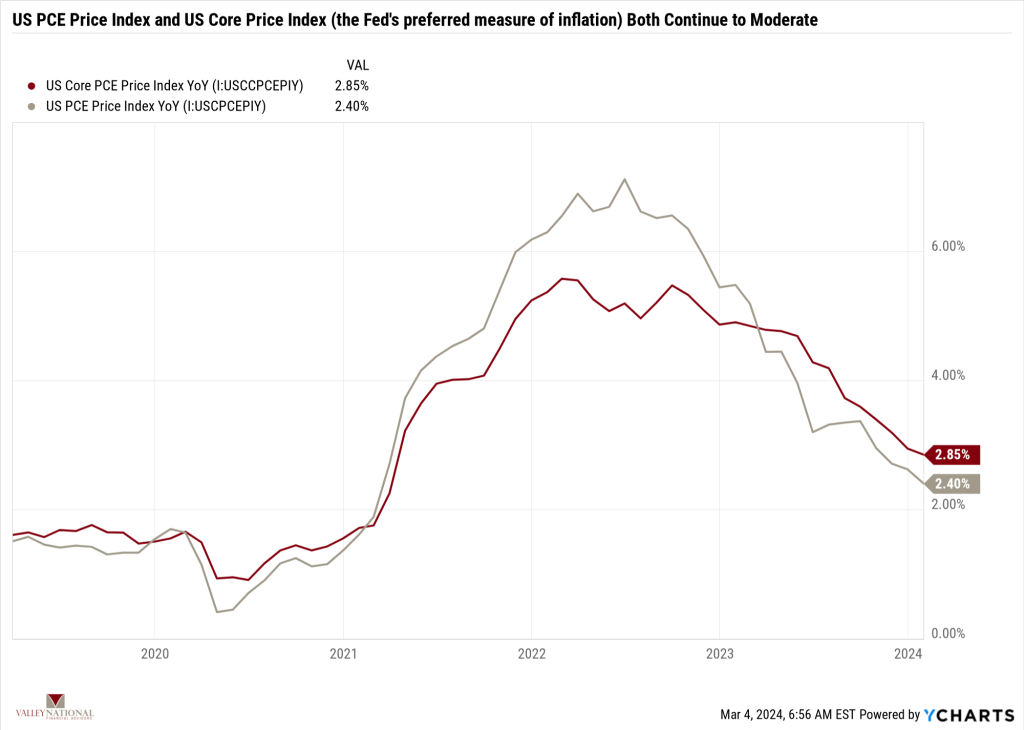

Last week’s inflation data showed that prices on consumer goods continue to fall. See Chart 1 from Valley National Financial Advisors and Y Charts showing U.S. Core PCE (Personal Consumption Expenditures) and US PCE YoY. The recent U.S. Core reading is at 2.85%, compared with 2.94% last month and 4.90% last year. This recent reading is lower than the long-term average of 3.24%. While the U.S. Inflation Rate is currently at 3.09%, below the Fed’s target of 2.00%, Fed Chairman Jay Powell has stated that interest rates could move before the inflation rate reaches their target. A Fed pivot (moving from raising rates to cutting rates) will help broaden out equity returns beyond the “Magnificent 7” because small-cap and mid-cap U.S. companies tend to be more interest rate sensitive than large-cap companies.

Corporate profits continue to be strong, and forward-looking estimates suggest we will see profit growth over the next year. Thus far, 90% of S&P 500 Index companies have reported 4th quarter earnings, and according to Bloomberg, revenue growth was +3.8%, while earnings growth was a healthy +7.5%. While much of the growth was attributable to the “Magnificent 7,” if the Fed does eventually pivot on interest rates (we expect not until the second half of 2024), cyclical sectors of the economy will benefit. Thus, economic growth will continue at a robust pace.

Policy and Politics

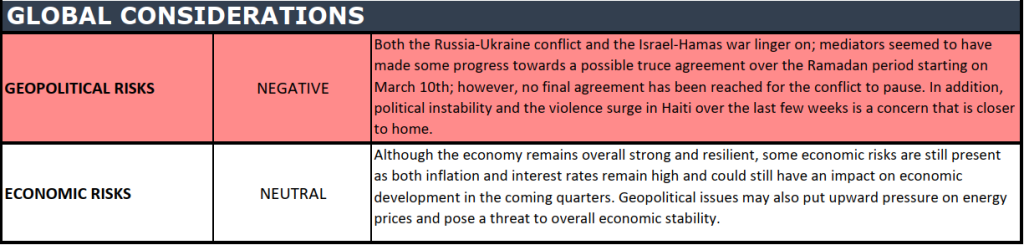

March 5th is Super Tuesday, with 15 U.S. states holding primaries on the same day. We expect that the 2024 U.S. presidential primary race will be determined after this date, and whether we have Trump v Biden or Haley v Biden, the next 8+ months will be chock full of the nonsense that sadly surrounds major U.S. elections these days. In the meantime, lawmakers have reached a tentative agreement (to be voted on this week) to fund the government, thereby avoiding another embarrassing shutdown.

We continue to watch the saga playing out with New York Community Bank, where last week they restated their previous earnings results and disclosed potential “weaknesses in internal accounting practices” (emphasis ours!). Banks can be fragile places because confidence in management means confidence in where one places their money for safekeeping. We are confident that the Federal Reserve Bank, the FDIC, and the Treasury know NYCB’s problems and will provide needed guidance and assistance.

What to Watch This Week

U.S. Job Openings: Total Nonfarm, released 3/6/24, prior 9.026M

U.S. Initial Claims for Unemployment Ins. for the week of 3/2/24, released 3/7/24, prior 215.000.

U.S. Labor Force Participation Rate for Feb 2024, released 3/8/24, prior 62.5%

U.S. Unemployment Rate for Feb 2024, released 3/8/24, prior 3.7%

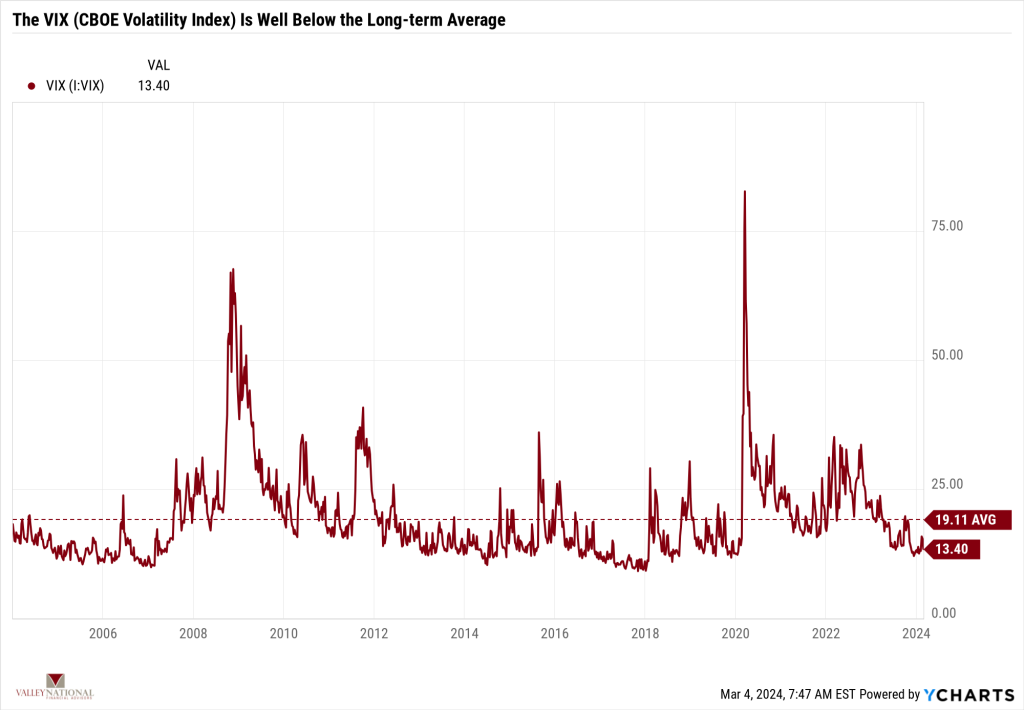

Market volatility remains sanguine, and other than the potential for a government shutdown, news from Washington DC has been muted. Global turmoil exists with Israel/Hamas and Ukraine/Russia, but true market volatility is muted. See Chart 2 below from Valley National Financial Advisors and Y Charts showing the VIX or Volatility Index. The VIX is at 13.40, well below the long-term average of 19.11. Our view on this data point is that true risks to the market, like higher interest rates and a major U.S. economic slowdown or disruption, remain on the sidelines, allowing markets to trade on their own merits.

Among the noise and news, markets continue to set new all-time highs as they efficiently filter out the noise. Low volatility, remaining fiscal stimulus from previous years’ bills (CHIPs Act or Inflation Reduction Act), and growing corporate earnings create real tailwinds for equities. If we get a Fed pivot on interest rates in the second half of 2024, further tailwinds will emerge. It is hard to find unwelcome news these days, but we will keep looking! Reach out to your advisor at Valley National Financial Advisors for help or questions.

Tune in Wednesday, 6 PM, “Your Financial Choices” on WDIY 88.1 FM. Laurie will be discussing: 2024 Tax Planning Now.

Questions can be submitted to yourfinancialchoices.com before the live show. Recordings of past shows are available to listen to or download at yourfinancialchoices.com and wdiy.org.

Did you miss the last show: Avoiding Estate Planning Mistakes with Attorney Peter Iorio? Listen Here