Tune in Wednesday, 6 PM for “Your Financial Choices” show on WDIY 88.1FM. Laurie will discuss: ‘Ping-Pong’ Planning – Financial planning in an ever-changing environment.

Welcome Back! We are emerging stronger and our offices are reopening. All our office spaces are now available for in-person meetings. Masks are no longer required for fully vaccinated individuals in our offices. Appointments to visit the office are no longer required, but contactless arrangements are still available.

As we all navigate our new normal, we will continue to follow CDC guidance and respect personal safety and preferences. If you wish for our team to wear masks on a visit to our offices, just ask. We ask in return that you reschedule your appointment if you or anyone in your household is not feeling well in any way. We will continue to maintain safe social distances whenever possible in shared spaces and follow rigorous cleaning protocols.

If you have any questions about our current practices or policies, please do not hesitate to ask. We are thrilled to be taking this first step with you. Let’s emerge stronger together!

We are hiring! Our team is seeking to fill client service positions with professional, experienced individuals. Do you know someone who would make a great addition to our Bethlehem office? VNFA – JOIN OUR TEAM

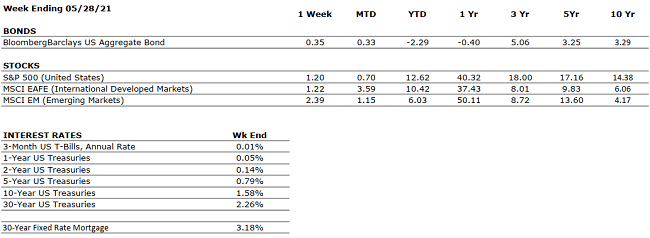

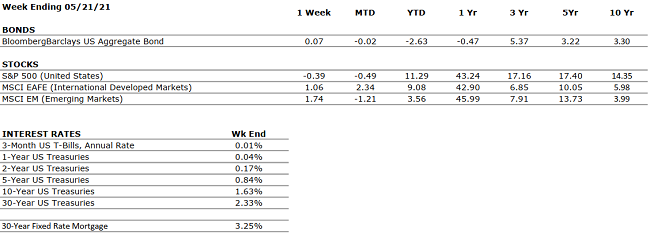

by William Henderson, Vice President / Head of Investments The markets notched another week of gains across all three broad market indices last week. For the week that ended May 28, 2021, the Dow Jones Industrial Average added +0.9%, the S&P 500 Index added +1.2% and the NASDAQ posted +2.1%; all solid gains for a relatively quiet week of trading in front of the Memorial Day Holiday. For the second week in a row, growth stocks easily outperformed their value counterparts; however, on a year-to-date basis, value still leads the pack. For the full year of 2021, returns on all market indices remain very healthy. Year-to-date, the Dow Jones Industrial Average has returned +13.8%, the S&P 500 Index +12.6% and the NASDAQ +7.0%. Bonds were relatively unchanged for the week, with the 10-year U.S. Treasury Bond remaining at 1.62% as of May 28, 2021.

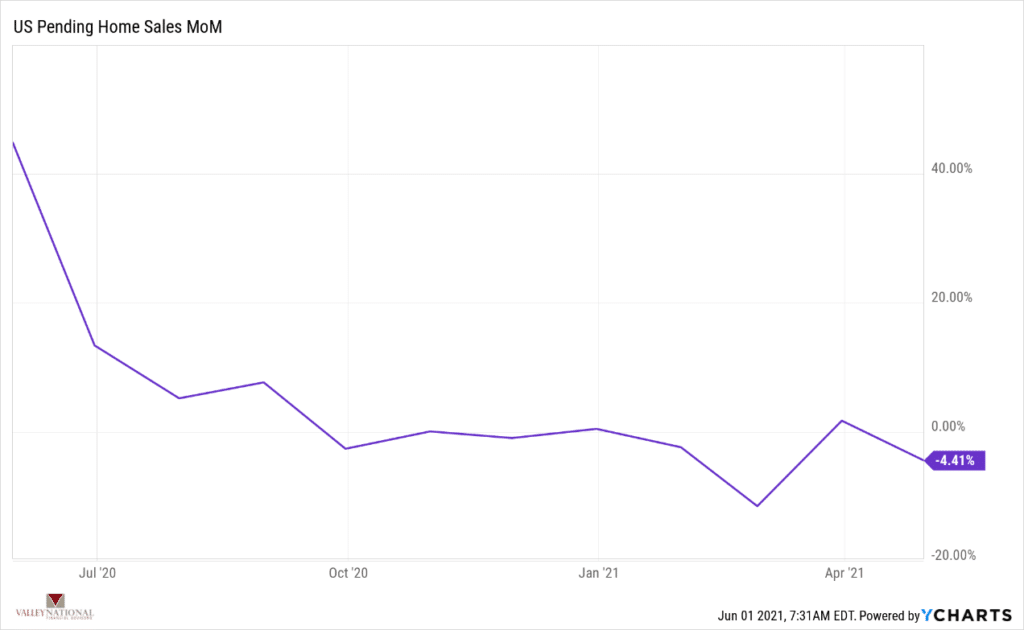

While Fed officials stressed last week that inflationary pressures should prove temporary, consumers continue to worry about real inflationary indications. Supply chain pressures, semi-conductor chip shortages, and housing price increases continue to worry consumers. For example, according to the S&P CoreLogic Case-Shiller Index, average home prices in major metropolitan areas rose 13.2% in the year ended in March 2021, up from a 12.0% annual rate the prior month representing the highest growth rate since December 2005. Conversely, we saw forward indications that housing may be cooling off. Last week, the National Association of Realtors reported that April 2021 pending new homes sales fell 4.4%, month over month (see chart below from YCharts); which was significantly below expectations.

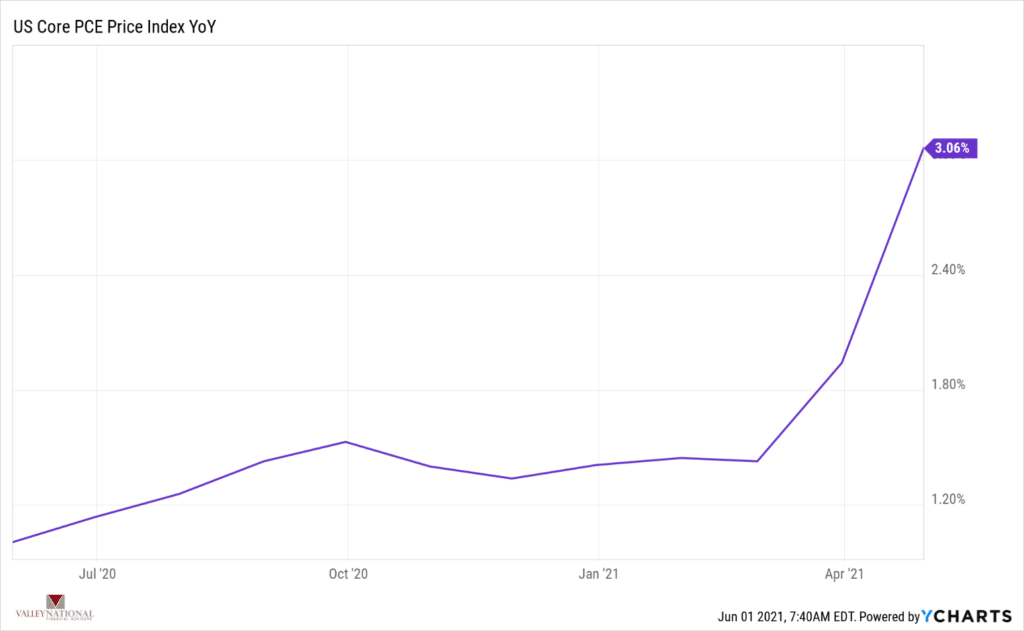

Regardless of what Fed officials are saying, the consumer certainly is seeing the impacts of inflation. For example, the Core PCE Price Index, or Personal Consumption Index, which measures the prices paid by consumers for goods and services, moved higher last week by 3.1%. (See the chart below from YCharts). This measure is a very good indicator of inflation trends as it removes food and energy, two categories where prices tend to swing up and down more dramatically.

Certainly, there are issues that concern consumers and investors such as inflation, supply shortages and variants of the COVID-19, but a return to normal activities and relaxing of travel and gathering restrictions seems to be impacting the markets’ upward trajectory. The consumer, with the help of stimulus funds and an easy Federal Reserve Bank, will continue to propel the economic recovery throughout 2021 and well into 2022.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

The economy expanded at a 6.4% annualized pace in Q1. At the current rate, U.S. GDP will return to pre-COVID levels by midyear.

CORPORATE EARNINGS

POSITIVE

S&P 500 Q1 sales and earnings growth were very strong.

EMPLOYMENT

POSITIVE

The unemployment rate increased to 6.1% in April, from 6% in March.

INFLATION

POSITIVE

Inflation was 4.5% in April. The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has generally been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

President Biden recently unveiled a stimulus package directed towards infrastructure that would total more than $2 trillion over eight years. President Biden is also considering a significant capital gains tax increase.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve continues to indicate that the monetary environment will remain very accommodative for the foreseeable future.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

With multiple vaccines in distribution and highly accommodative fiscal and monetary policies in place, 2021 may be one of the strongest economic years on record.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

by William Henderson, Vice President / Head of Investments Markets ended mixed last week with a reversal of the technology and value sectors for the first time in a while. The tech-heavy NASDAQ returned +0.3% for the week that ended May 21, 2021, while the Dow Jones Industrial Average lost –0.5% and the S&P 500 Index lost –0.4% over the same period. With the Fed on hold for interest rate movements and some weaker than expected employment and economic information, the bellwether 10-year U.S. Treasury Bond remained well below its 2021 high of 1.74% to close the week at 1.62%. Rising bond yields can be indicative of improving economic conditions. For the full year of 2021, returns on the stock market remain solidly positive. Year-to-date, the Dow Jones Industrial Average has returned +12.6%, the S&P 500 Index +11.3% and the NASDAQ +4.8%.

Inflation concerns have cast a

pall on the

markets over past weeks. One

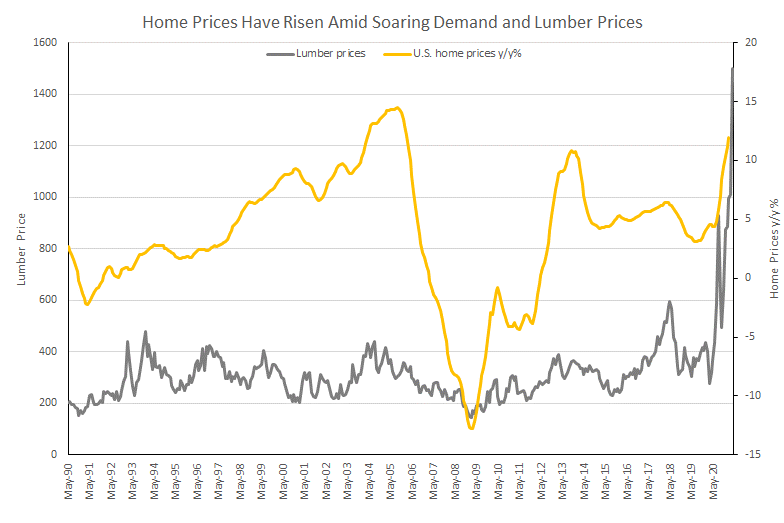

such area of noted inflation can certainly be seen in the housing market. Due

to a significant jump in demand,

home prices have skyrocketed in many regions of the country. Lower

inventories and dramatically rising building-materials costs

have impacted home

prices. Higher

lumber

prices, for example, have had a

substantial impact on new

home construction prices. The

chart below from Bloomberg, shows the gain in

housing prices and lumber after the COVID-related recession.

While the spike is reminiscent of

the housing crisis of 2008-09 that led to the Great Financial Crisis, it is not

likely to have a similar effect this time around. This time, we have

falling unemployment rates, an increase in “work from home” demand, record low mortgage

rates, and tight new housing construction trends. Conversely, the current

housing climate gives the economy a sound foundation for a continued

recovery.

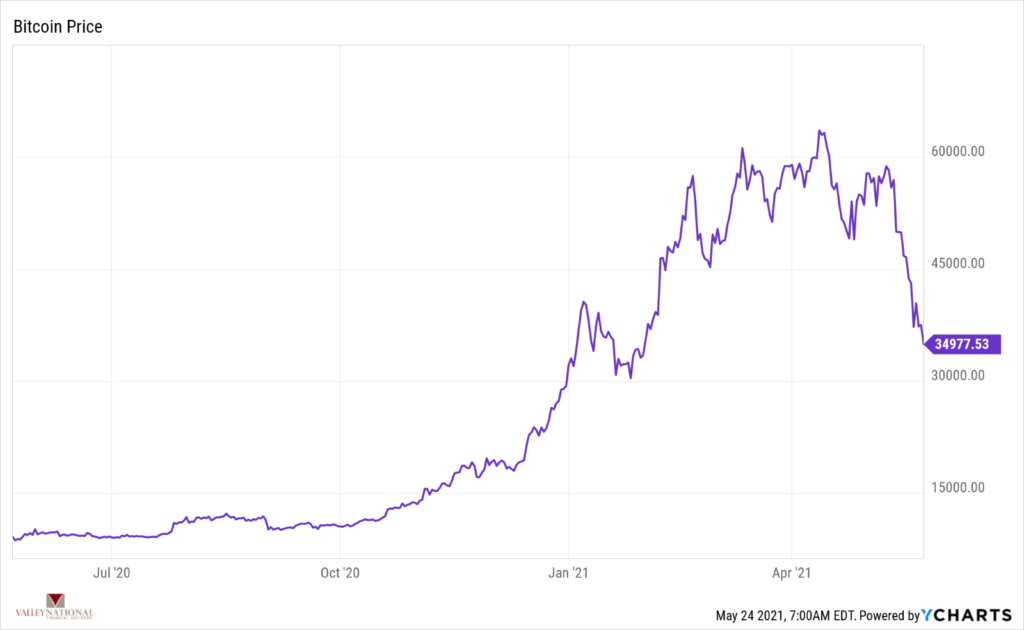

We cannot mention the word

“spike” without a brief discussion of Bitcoin. Bitcoin

and other cryptocurrencies have garnered plenty of attention during this market

bull run, which

is clearly indicative of two

things: market liquidity and excess cash chasing investment opportunities. The

chart below from Y-Charts, shows the run up in Bitcoin to near 60,000 (in

U.S. dollars) and the

recent near-50%

sell-off. While

drastic drops in asset prices are unsettling, Bitcoin

is still a new asset

class and small in

terms of the overall market capitalization. However,

volatility in esoteric areas

of the market have, on

occasion, roiled investors in a wider arena.

This week we will see the final

batch of 1st quarter

earnings reports, with some major retailers and tech names reporting. Important

names like Urban Outfitters, AutoZone, Dick’s Sporting Goods, Best Buy and

Costco report and will give us a glimpse of the consumer’s

move back to shopping whether online or in person. High-flying

tech names like Snowflake, Salesforce, and

Workday all report this week

as well. The

work from home trend has impacted these

names and we will see if the recent push by corporate CEOs back to the

workplace has a

different impact.

Nationally, we have witnessed a

major victory over COVID-19 as we reached

the critical 50% vaccination rate. Further, local economies are opening

and lifting capacity restrictions

on gatherings and restaurants. As

we move into the summer, we will see the last area of the economy: travel

and leisure surge with activity; limited only by constraints

on labor. Our

best friend remains Fed

Chairman Jay Powell and his commitment to low interest rates for longer.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

The economy expanded at a 6.4% annualized pace in Q1. At the current rate, U.S. GDP will return to pre-COVID levels by midyear.

CORPORATE EARNINGS

POSITIVE

S&P 500 Q1 sales and earnings growth have come in at 9% and 45%, respectively, representing extremely strong results.

EMPLOYMENT

POSITIVE

The unemployment rate increased to 6.1% in April, from 6% in March.

INFLATION

POSITIVE

Inflation was 4.5% in April. The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has generally been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

President Biden recently unveiled a stimulus package directed towards infrastructure that would total more than $2 trillion over eight years. President Biden is also considering a significant capital gains tax increase.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve continues to indicate that the monetary environment will remain very accommodative for the foreseeable future.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

With multiple vaccines in distribution and highly accommodative fiscal and monetary policies in place, 2021 may be one of the strongest economic years on record.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.