MEET NECC WITH TEAM VNFA You’re invited to a virtual community gathering – July 16, 2:00 p.m.

The

team at Valley National Financial Advisors wants you to help our community

learn more about Northeast Community Center in Bethlehem.

Please join us for a community meeting to discuss the needs of our neighbors

and the programming and services NECC is providing to improve lives.

This

is a free virtual event – your attendance and attention is all we require to

make a difference. Please share this invitation with other community advocates.

View/Download PDF version of Q2 Commentary (or read text below) by Maurice (Mo) Spolan, Investment Research Analyst

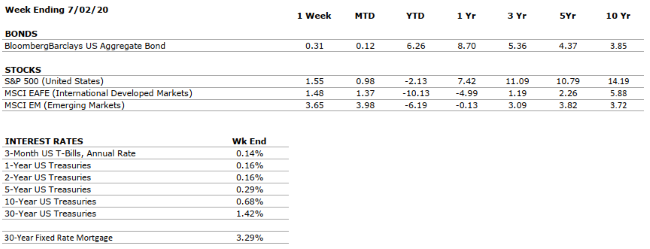

Equities The S&P 500 posted a greater than 20% gain during Q2. For the 50 days ended June 3rd, the U.S. stock markets experienced the greatest two-month rally in history, increasing nearly 40%. The breadth of the equity climb was also apparent, as the Russell Mid-Cap and Small-Cap indices reported yet greater performance than did the S&P 500, signaling an embrace of potentially riskier stocks. International stocks also attended the rally, although gains abroad were milder than those in The States.

There are three important points about the rally on the front of our minds. First, the equity performance in Q2 is all-the-more extraordinary when contrasted to what occurred at the conclusion of Q1, when the stock market was in the midst of the steepest bear market entry of all time. The dynamics of the last four months illustrate just how challenging an investment strategy is market timing. Second, the Federal Reserve’s commitment to purchase trillions of dollars of fixed income securities was instrumental in the market bounce. The Fed injected an unprecedent degree of liquidity into the markets, which forced interest rates downward and equipped investors with newfound cash, ultimately working to increase the relative attractiveness of stocks versus bonds. In addition, the Fed’s actions allowed companies to issue new debt to weather the COVID-19 storm, increasing investor confidence in the resiliency of many major companies. Last, the stock market rally was encouraged by economic data that improved with rapidity in May and June as social distancing guidelines were relaxed, demonstrating that something akin to a V-shaped recovery may be a real possibility.

Bonds The Barclay’s Aggregate Bond Index returned just under 3% during Q2, while fixed income strategies with risk profiles more analogous to equities – such as those focused on consumer credit or below-investment grade corporations – offered better performance. Interest rates remain near zero as the yield curve – the difference between rates on short-term and long-term treasury instruments – is quite flat. Fed Chairman Jay Powell shared in an interview during Q2 that the U.S. Central Bank is “not even thinking about thinking about raising rates”. Interest rates are likely to remain low for the foreseeable future as monetary actions attempt to facilitate an economic recovery.

Outlook As most states have begun the reopening process, new COVID cases are accelerating while economic data is improving. Several states who have reported the greatest number of new cases, namely Florida, Texas and Arizona, have walked back much of their reopening measures in an effort to mitigate viral spread. If more states experience coronavirus surges and pivot to stricter social distancing guidelines in response, economic data is likely to worsen, and financial markets may react negatively. In addition, the presidential election will be heating up over the next three months, and asset price volatility has historically heightened during pre-election periods. With this said, the power of the monetary and fiscal stimulus by the Federal Reserve and the U.S. Treasury is not to be discounted, and both forces are near certain to continue to support asset markets over the coming quarters. With uncertainty as pronounced as ever, we believe that investors are best off adhering to their carefully constructed long-term financial plans.

AUDIO: Q2 2020 Market Commentary Our CEO, Matt Petrozelli, offers an analysis of Q2 and a forecast for Q3 for 2020. LISTEN NOW/DOWNLOAD MP3

You can vote every day for #TeamVNFA in the Lehigh Valley Business 2020 Reader Ranking Awards between July 1 and July 29, 2020 (Wealth Management Firm category). CLICK HERE TO VOTE

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

May’s retail sales and consumer spending rebounded at record clips month-over-month, following unprecedented declines in April. However, new coronavirus cases in the US are accelerating as social activity has increased, which threatens to rescind the gains in consumer confidence.

CORPORATE EARNINGS

VERY NEGATIVE

Coming into the year, analysts were expecting mid to single digit earnings growth, but the spread of COVID-19 is likely to have a substantial impact on near-term earnings forecasts. However, earnings could bounce back quickly once the pandemic has run its course.

EMPLOYMENT

VERY NEGATIVE

Non-farm payroll increased by 4.8 million jobs in June, led by the Leisure & Hospitality sector, as the unemployment rate declined to 11.1%. However, the unemployment rate remains historically high and is still 7.6% higher than it was in February.

INFLATION

POSITIVE

The deflationary environment created by COVID-19 should provide additional room for robust stimulus from both fiscal and monetary policy initiatives. However, we will be watching closely in the intermediate term for second and third order effects leading to a return of inflationary pressure.

FISCAL POLICY

VERY POSITIVE

The US Government has passed a series of fiscal measures to combat the economic impacts of the COVID-19 pandemic. The largest of these measures, known as the CARES Act, provides approximately $2.2 trillion of support for businesses and families that are impacted by business closures and unemployment.

MONETARY POLICY

VERY POSITIVE

In response to the threat of COVID-19, the Federal Reserve has implemented two emergency rate cuts and has moved its target interest rate back to zero. Additionally, it has announced its intention to conduct further asset purchases to support markets. We believe that the Fed is doing all it can to support the economy and markets.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

Western opposition to China’s National Security Law, legislation that reduces Hong Kong’s autonomy, has amplified the discord already present between the US and China as a result of COVID-19. In addition, demonstrations across the US evidence considerable domestic unrest.

ECONOMIC RISKS

VERY NEGATIVE

The economic impacts of the COVID-19 pandemic are likely to be substantial. However, we believe that the eventual economic recovery (which will be aided by historically large economic stimulus) may occur more swiftly than from previous economic shocks.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie has returned to the studio which means she can

take your questions live on the air at 610-758-8810, or address those submitted

via yourfinancialchoices.com.