Our Founder & Chairman, Thomas Riddle is among the 2020 ICON honorees being celebrated by Lehigh Valley Business. The second annual ICON Honors recognizes the Greater Lehigh Valley’s business leaders over the age of 60 for their notable success and demonstration of strong leadership, both within and outside their chosen field. A virtual awards celebration will take place on November 5 from 5-6 p.m. Visit lvb.com/events for more information.

This 2020 recognition coincides with the 35th anniversary of Valley National Financial Advisors. Tom founded the firm in 1985 and is an active member of our team today as we continue his mission to help clients make the right financial choices in pursuit of their long-term financial goals.

by William

Henderson, Vice President / Head of Investments Markets

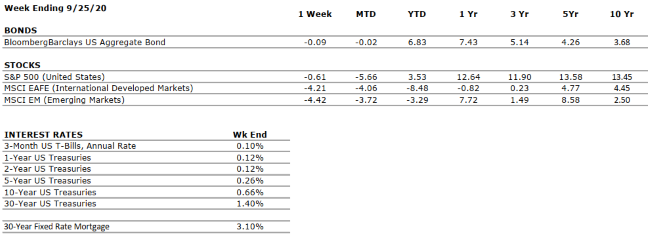

ended the week of September 25, 2020 in mixed territory with the Dow Jones

Industrial Average down (1.8%), the Standard & Poor’s 500 Index down (0.60%)

and the NASDAQ up 1.1%. While mixed markets are always confusing, it bears

understanding why there is a divergence. Industrial companies are struggling,

and we saw that with the Durable-Goods Orders number released last week by the

Commerce Department, rising only 0.40% in August; which was much lower than

economists’ predictions of 1.80%. Yet, technology companies continue to do well

as online shopping, virtual connectivity and other e-commerce related equities

helped push the NASDAQ higher. Wall Street and Main Street are seeing different

things.

The good-news, bad-news stories do not really mask the

continued ongoing uncertainty impacting the economy. Few of our market

disruption events have been quelled. COVID-19 pandemic is waffling between a vaccine

and a spike; and which one will come first. The presidential election is no

one’s guess. As of September 28, 2020, the top battleground state’s

average according to Real Clear Politics shows Joe Biden winning by a thin 3.8

points. Is that enough to cover the “silent majority Trump vote?” The recession

is lingering but good news abounds with record-low mortgage rates fueling a

booming housing market. Last week, the Commerce Department said sales of new

single-family homes rose 4.8% in August to a seasonally adjusted annual rate of

1.01 million! August 2020 sales were 43% above the year-earlier level. Low

rates continue to fuel mortgage refinancing as well. Social unrest and protests

continue and could actually increase as the Senate moves ahead with the

confirmation of Judge Amy Coney Barret to fill the SCOTUS seat vacated with the

death of Ruth Bader Ginsburg. The byproduct of the confirmation battle and

the concomitant unrest is that any hope of a third round of fiscal stimulus

gets tossed aside while both parties wrestle with the issue of the week

instead.

While the lack of further fiscal stimulus is a drag on

the economy, a bright spot is the strength of the private sector and huge pent

up cash reserves sitting in money market funds and bank deposits. Private

sector cash holdings have surged during the pandemic. According to the St.

Louis Federal Reserve Bank, the personal savings rate as a percent of disposable

income was nearly 18% as of July 2020, a surge from January 2020’s level of

7.6%. Further, the sum of U.S. money market assets plus commercial bank

deposits has grown by nearly $4 trillion, to $20 trillion, during the pandemic

and now sits at more than 100% of GDP. This cash hoard can easily fill the

void that a missing third fiscal stimulus package leaves. Being locked down as

the U.S. consumer has been since March 2020, has allowed a massive buildup of

ready cash and reserves, that once released, could fuel the economic rebound we

need. Watch for cash to flow into the economy as each of our unknowns gets

worked out or fizzles away. With the election just 36 days away, that

unknown may become a known fairly soon. Lastly, Speaker of the House, Nancy

Pelosi, is scheduled to meet with Treasury Secretary Stephen Mnuchin this week

to continue discussions of a third fiscal stimulus package. We expect markets

to continue to waffle, with pull backs and rallies each week because

uncertainly is bad for traders and the markets and there is simply too much

uncertainty going around these days. A long-term perspective must be taken

in conjunction with a balanced, well-designed investment portfolio.

October 15, 2020 is the filing

deadline for 2019 federal tax returns on extension. Even though the initial tax

filing deadline was pushed back this year from April 15 to July 15, the standard

six-month window for filing extended returns has shrunk to three months from

July to October, and October 15 remains the final due date for filing 2019

federal returns in 2020.Read more about extension reminders at Forbes.com.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

GDP declined at an annualized rate of 32.9% in Q2, the fourth-largest fall in the last 100 years. In mirror opposition, Q3 GDP is expected to represent the greatest quarter-over-quarter increase in history, coming in somewhere between 25-35% on an annualized basis.

CORPORATE EARNINGS

VERY NEGATIVE

S&P 500 earnings fell by around 1/3 in Q2, the sharpest year-over-year decline since 2008. However, some companies in certain sectors have reported strong results, such as in Retail and Cloud Computing.

EMPLOYMENT

VERY NEGATIVE

About 1.4 million U.S. jobs were added in August, in-line with market expectations. The American economy has now added back roughly half of the 22 million jobs lost since March. The unemployment rate remains well above historical averages, at 8.4%.

INFLATION

POSITIVE

Core inflation has come in at 1.7% over the last twelve months. The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

VERY POSITIVE

Weekly unemployment benefits are now being disseminated on a state-by-state basis, through applications to a Federal slush fund, and total $300 per week, versus the previous rate of $600 under the now-expired Federal plan.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve has supported asset markets with unprecedented speed and magnitude in response to COVID-19. In our view, Fed President, Jay Powell, reaffirmed the central bank’s accommodative stance in his virtual address “at Jackson Hole”.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

The relationship between the US and China, the world’s two largest economies, was already weakened by the trade war but has deteriorated further as a result of COVID-19.

ECONOMIC RISKS

VERY NEGATIVE

The impacts from COVID-19 were as swift and pronounced as any shock in modern times. Robust monetary and fiscal stimulus stabilized the system, however, economic activity remains well- below that in 2019, and uncertainty remains high.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.