Welcome Zaesha Boirard to Team VNFA! She will be working remotely from the Bethlehem office as Administrative Assistant for the Tax Department. She will be responsible for coordinating processes across the tax team, and managing client data, documents and communications. Zaesha joins the team with many years of administrative and client service experience, and she is committed to the VNFA client -first culture.

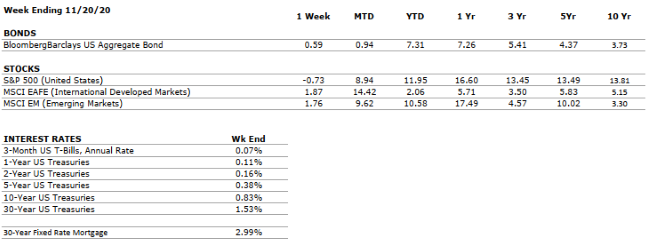

by William Henderson, Vice President / Head of Investments Equity markets were mixed last week as headlines threw bad news after good news. Early in the week, positive COVID-19 vaccine news improved investor sentiment, but rising new cases and increased activity restrictions across states cast concerns on the economic recovery. The potential for a divided U.S. Government which could drag on any new fiscal stimulus is also weighing on the markets. For the week, the Dow Jones Industrial Average returned -0.3%, the Standard & Poor’s 500 Index returned -0.8%, while the NASDAQ returned +0.2%. The benchmark 10-year U.S. Treasury note stood at 0.88% at the end of the week.

As

noted above, the short-term market moves are impacted by headline news

events. That said, parts of the economy continue to do very well, such as

the U.S. housing market. October existing home sales were +4.3% year over year

and new starts were +4.9% year over year, both beating economists’ expectations. Further,

according to Goldman Sachs, the NAHB housing market index reached a record high

of 90 for November. Housing remains a resilient and sturdy foundation of

the economic recovery. The American consumer continues to show strong

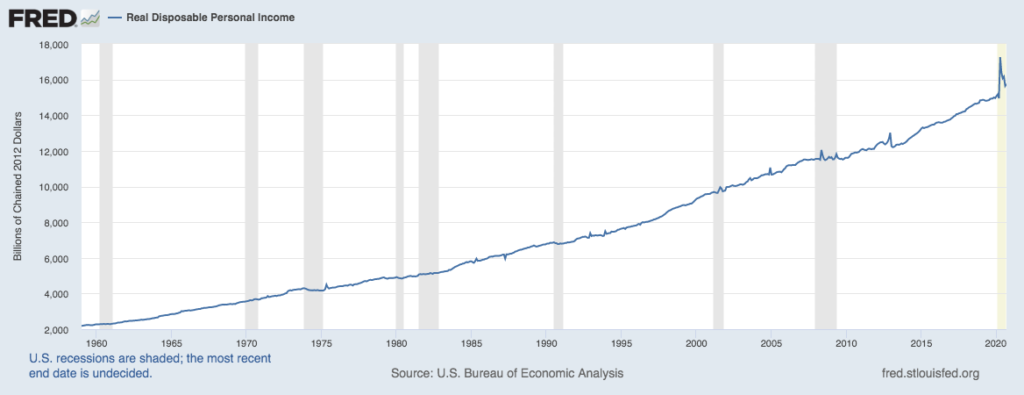

financial wherewithal. According to the Federal Reserve Bank of St. Louis,

Real Disposable Personal Income stood at $15.8 trillion in September 2020, up

from $15.0 trillion in September 2019.

Further,

Average Hourly Earnings of All Private Employees was $29.50/hour, up from

pre-COVID-19 March 2020 at $28.69/hour. Lastly, according to Bloomberg,

consumers have used their cash piles to pay down debt and secure record-low

mortgage rates due to an ultra-easy Fed policy fueling a steady wave of

refinancing.

The Thanksgiving holiday will give us a shortened work week and potentially quieter trading days. The Christmas shopping season will kick-off with Black Friday this week but what does that mean when the shopper is confined to their home? Watch for online retailing to explode this year with firms that have the logistics for effective online shopping benefiting most. Black Friday could morph into Cyber Friday as working from home collides with closed malls and a consumer flush with cash.

We

have three pharma companies announcing a vaccine: AstraZeneca, Pfizer, and

Moderna. The Fed remains on guard to supply as much liquidity and

stability needed to fuel the economic recovery. A COVID-weary consumer

stands on the sidelines flush with cash but locked down as COVID-19 cases

spike. In the short term, the markets continue to waffle on good news/bad

news headlines but year-to-date, all three broad indices remain positive: the Dow

Jones Industrial Average at +2.5%, the Standard & Poor’s 500 Index at 10.1%,

and the NASDAQ at +32.1%. Remain committed to long-term goals, see through

the noise and watch the markets prove they are more efficient than the

consumer.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

GDP increased at a 33.1% annualized pace in Q3. The U.S. economy has now recovered about 2/3 of its output lost to the COVID-19 pandemic.

CORPORATE EARNINGS

NEGATIVE

As more than 90% of S&P 500 constituents have reported Q3 results, the index’s earnings are down 7-8% from the year-ago period. This compares to Q2 2020, in which S&P 500 earnings were down by 1/3 from the comparable 2019 quarter.

EMPLOYMENT

NEGATIVE

As of October’s end, the U.S. unemployment rate stood at 6.9%, well below where most expected the metric to be at this point some months ago. The unemployment rate has consistently declined since peaking above 14% in April.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

VERY POSITIVE

A second major COVID-19 stimulus bill is likely to be passed over the coming months.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve has supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

The relationship between the US and China, the world’s two largest economies, was already weakened by the trade war but has deteriorated further as a result of COVID-19.

ECONOMIC RISKS

VERY NEGATIVE

The impacts from COVID-19 were as swift and pronounced as any shock in modern times. Robust monetary and fiscal stimulus stabilized the system; however, economic activity remains well- below that in 2019, and uncertainty remains high.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Our team is excited to announce that our partnership with WDIY will result in a donation to Second Harvest Food Bank for 12,362 meals. As part of the radio station’s Fall Membership Drive, VNFA sponsored an incentive whereby every $100 pledged to support WDIY triggered a separate, direct gift to Second Harvest. Thank you to everyone who gave in support of both non-profit organizations!

by William Henderson, Vice President / Head of Investments Question: What do you get when you mix $19 trillion of cash with a vaccine for COVID-19 and a divided U.S. Government? Answer: The potential for a seriously bullish market. M2 or the measure of the Money Supply of the United States currently stands at $19 trillion, up from $15 trillion in November 2019. M2 is the sum of all cash held by consumers and companies, plus money market accounts and bank deposits, and all “quasi-cash” balances such as Eurodollar deposits. M2 stands at a record level and represents the cash on sidelines ready to be put to work either by investing or spending. Cash balances are high as a direct result of COVID-19 restrictions and consumers who have simply not been able to spend. On Monday (November 16), Moderna Inc. announced that its vaccine for COVID-19 is 94.5% effective in primary testing. This announcement comes one week after Pfizer announced that their vaccine for COVID-19 was 90% effective in clinical trials. This is good news for consumers who have stayed on the sidelines, not spending or investing, due to fears of contracting the virus. A safe, effective and widely distributed vaccine for COVID-19 has the potential to release $19 trillion into the U.S. Economy.

The U.S. Presidential Election is largely

decided, although we are still awaiting a run-off for two U.S. Senate seats in

Georgia. Currently, Real Clear Politics has both seats leaning Republican

allowing for divided government, which the markets sometimes tend to

favor.

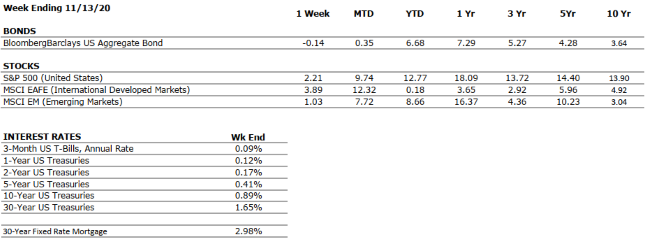

Last week’s market returns were mixed as

investors slowly moved away from tech-heavy NASDAQ equities to more consumer

related equities that make up the broader S&P 500 Index and the Dow Jones

Industrial Average. The week ending November 13, 2020, had the Dow Jones

Industrial Average returning +4.1%, the S&P 500 Index +2.2 and the NASDAQ

(-0.6%). After last week’s moves, year-to-date returns are positive for

all three market averages with the Dow Jones at +3.3%, S&P 500 Index +11.0%

and the NASDAQ at +31.8%. In a year like 2020, with all the uncertainty

and cataclysmic events, to have all three major market averages in positive

territory certainly points to the resiliency of the U.S. economy and the

forward-looking nature of markets. We’ve said before that the market is

far more efficient and forward thinking than investors may give it

credit.

The Federal Reserve remains committed to

providing liquidity and stability to the markets by keeping short-term interest

rates near zero. Conversely, yields on the benchmark 10-year U.S. Treasury

Bond continue to move higher little by little each week. After bottoming

in August 2020 at 0.51%, the 10-year U.S. Treasury Bond stood at 0.92% as of

November 16, 2020; but this level is dramatically lower than year-end 2019,

when it stood at 1.92%. Watch for U.S. Treasury Bonds to fluctuate as the

markets waffle between the news of higher infection rates of COVID-19 and

further information about the release and distribution of an effective

vaccine. The markets are digesting a lot of conflicting and impactful

information all the while pointing to an eventual outcome of a massive release

of cash into the economy. Timing remains uncertain but the outcome does

not; which confirms the value of sound financial planning coupled with clear

long-term thinking.

Team Chat – Trending Topics (November 2020)

Head of Investments, Bill Henderson interviews Tim Richmond, CPA about year-end tax planning and tax lost harvesting. WATCH NOW

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

GDP increased at a 33.1% annualized pace in Q3. The U.S. economy has now recovered about 2/3 of its output lost to the COVID-19 pandemic.

CORPORATE EARNINGS

NEGATIVE

With 90% of S&P 500 constituents having reported Q3 results, earnings are down 7-8% from the year-ago period. This compares to Q2 2020, in which S&P 500 earnings were down by 1/3 from the comparable 2019 quarter.

EMPLOYMENT

NEGATIVE

As of October’s end, the U.S. unemployment rate stood at 6.9%, well below where most expected the metric to be at this point some months ago. The unemployment rate has consistently declined since peaking above 14% in April.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

VERY POSITIVE

A second major COVID-19 stimulus bill is likely to be passed over the coming months.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve has supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

The relationship between the US and China, the world’s two largest economies, was already weakened by the trade war but has deteriorated further as a result of COVID-19.

ECONOMIC RISKS

VERY NEGATIVE

The impacts from COVID-19 were as swift and pronounced as any shock in modern times. Robust monetary and fiscal stimulus stabilized the system; however, economic activity remains well- below that in 2019, and uncertainty remains high.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.