We are Hiring! Valley National Financial Advisors is seeking a full-time Financial Technology and Trading Associate to manage our investment databases and assist with operational securities trading and support. Learn more and find the application link at our website: https://valleynationalgroup.com/about-vnfa/join-our-team/

VNFA In the Community Although it looked very different this year, without a wrapping party or group delivery, our team put together 35 Holiday Hope Chests for Volunteer Center of the Lehigh Valley. We were also able to sponsor additional online gift purchases and wrapped boxes to help the program supply a happy holiday to thousands of local children through non-profit distributions. “Our goal was 35 boxes as a nod to our 35th anniversary as a local and independent business this year,” said Judianne Harris, Chief Marketing Officer. “Members of our team really went above and beyond using creative and safe approaches to make a meaningful contribution.”

Thank you to

everyone who helped support our commitment to community!

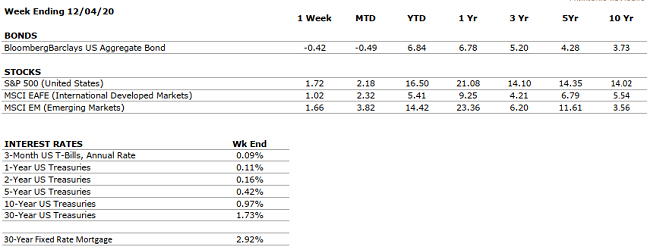

by William Henderson, Vice President / Head of Investments For the week that ended December 4, 2020, stocks reached further into record territory with the Dow Jones Industrial Average closing comfortably above 30,000, at 30,218. For the week, The Dow returned +1.1%, the Standard & Poor’s 500 Index returned +1.7%, and the NASDAQ returned +2.1%. The weekly gains piled onto previous gains to put year-to-date figures well into the positive zone. Year-to-date, the Dow has returned +5.9%, the S&P 500 +14.5%, and the NASDAQ a staggering +38.9%. These numbers are all the more remarkable when factored in to what 2020 threw at the markets: a global pandemic, a huge double-digit recession and a complicated and costly U.S. Presidential Election.

Last week, news of European Union (EU) regulators

considering emergency authorization for Pfizer/BioNTech’s COVID-19 vaccine for

wide-spread release sparked a rally early only to be stymied later in the week

after Pfizer acknowledged supply chain problems. The general flip-flop has

plagued the markets all year. We get good news that is quickly followed by bad

news. We’ve seen this with 1) the vaccine but increasing COVID-19 case

abound; 2) a stimulus package is discussed but not passed by congress; 3)

a decided presidential election but a run-off in Georgia for two senate

seats. It should not be news to readers of this report that we always talk

about one clear constant that the markets are relying on for support – the

Federal Reserve. The Fed has lowered rates to zero, announced monetary

policy steps to sure up the bond markets and stated over and over that it will

provide all needed stability and liquidity to assure the economic recovery.

Sure, the news and economic reports are as negative as

they are positive, but the markets seem to be seeing past this noise and

looking to 2021 when a vaccine for COVID-19 could be widely available and

distributed around the world. Consumers, who have been storing up cash,

will then be released to spend again and we could see a very strong economic

rebound following 2020. The larger macroeconomic risks that exist today

make it more important than ever for investors to keep their goals front and

center and stick with their investment plans. It is much better to focus on

long-term results over full market cycles.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

GDP increased at a 33.1% annualized pace in Q3. The U.S. economy has now recovered about 2/3 of its output lost to the COVID-19 pandemic.

CORPORATE EARNINGS

NEUTRAL

As more than 90% of S&P 500 constituents have reported Q3 results, the index’s earnings are down 7-8% from the year-ago period. This compares to Q2 2020, in which S&P 500 earnings were down by 1/3 from the comparable 2019 quarter.

EMPLOYMENT

NEGATIVE

In November, the unemployment rate declined to 6.7%. This continued the month-over-month improvements seen since April, when the metric was above 14%. However, the pace of hiring slowed greatly in November as COVID-19 cases surged.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

A second major COVID-19 stimulus bill is likely to be passed over the coming months.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

Although economic activity mostly remains below 2019’s levels, improvement has occurred across nearly every measure since the April nadir. With a vaccine on the horizon, a fiscal package probable, and interest rates low, 2021 is positioning to be a strong economic year.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” show on WDIY 88.1FM: Year-End Tax Planning starting with a discussion about charitable giving with a guest from the ArtsQuest Foundation.

Laurie can take your questions live on the air at 610-758-8810, or address those submitted via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.