Our team of Financial Advisors is featured in this month’s issue of Lehigh Valley Style magazine. Check out page 39 and share our website with anyone you feel might benefit from learning more about our professional team. Lehigh Valley Style November 2021

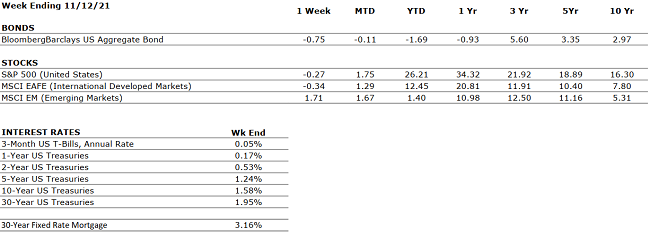

by William Henderson, Vice President / Head of Investments U.S. equities sold off last week as a double dose of poor economic data hit the markets: inflation and consumer sentiment (more on that below). Last week, the Dow Jones Industrial Average rose fell -0.6%, the S&P 500 Index decreased by -0.3% and the NASDAQ dropped by -0.7%. Fortunately, year-to-date returns across all major markets remain strong so last week’s modest sell off did not materially impact returns thus far in 2021. Year-to-date, the Dow Jones Industrial Average has returned +19.8%, the S&P 500 Index +26.2% and the NASDAQ +23.8%. The 10-Year U.S. Treasury moved higher by two basis points closing the week at 1.55% and still well below the 1.74% level reached in March of this year.

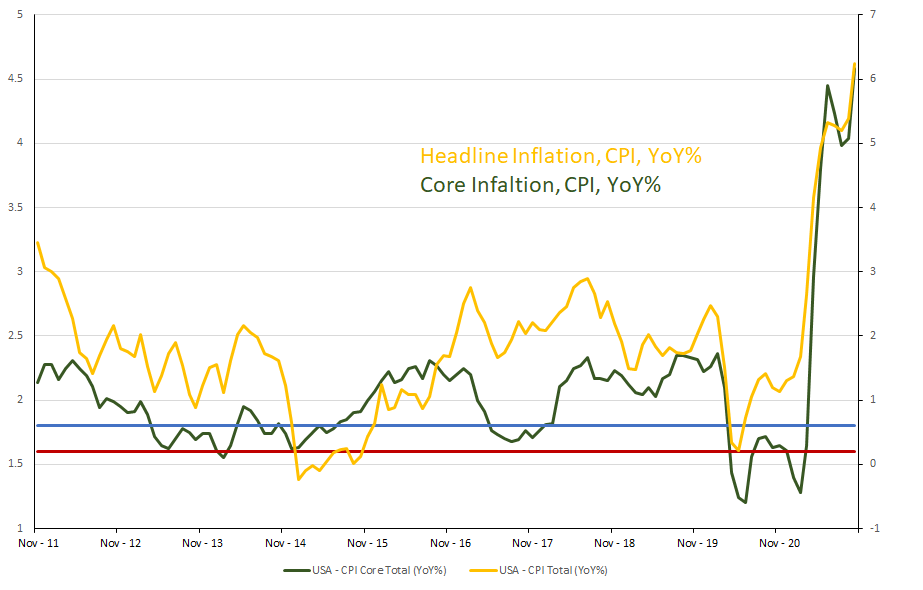

As mentioned, inflation

indicators released last week showed the economy continued to signal

higher prices for many goods and services. Both the Producer Price Index

(PPI) and Consumer Prices Index (CPI)

came in well above economists’ expectations

and reached multidecade highs. The CPI reading was +6.2%, the highest

level since 1991, while the PPI reading was +8.6%,

the highest level since 2010. Some economists shrugged the news off noting

that the data was largely driven by

“transitory” factors like energy and

auto prices but other less transitory factors such as rent, and

wages also showed significant price increases. The markets and consumers

may not like higher inflation, but

this is what the Fed ordered and remember, prior the pandemic

for nearly 10-years, inflation had averaged a paltry

+1.6%, well below the Fed’s mandated target of +2.0%. (See the chart below

from FactSet).

While inflation commonly hangs an

anchor on consumption and growth, we expect higher inflation

to moderate next year as supply chain disruptions, labor

shortages and strong consumer demand eventually

fall back to pre-pandemic, manageable levels. Further, the flexible or

transitory components of inflation, energy, autos, and

food, have

been hardest from supply problems and should

reverse once global pressures ease. However,

the stickier parts of inflation such as wages, rent and

healthcare are not likely to reverse, for example, it is usually very

difficult to reverse salary

increases, once

implemented. If the Fed manages its mandate

well, there will be a balance of prices

between transitory and sticky that allow inflation to average their +2.0% goal.

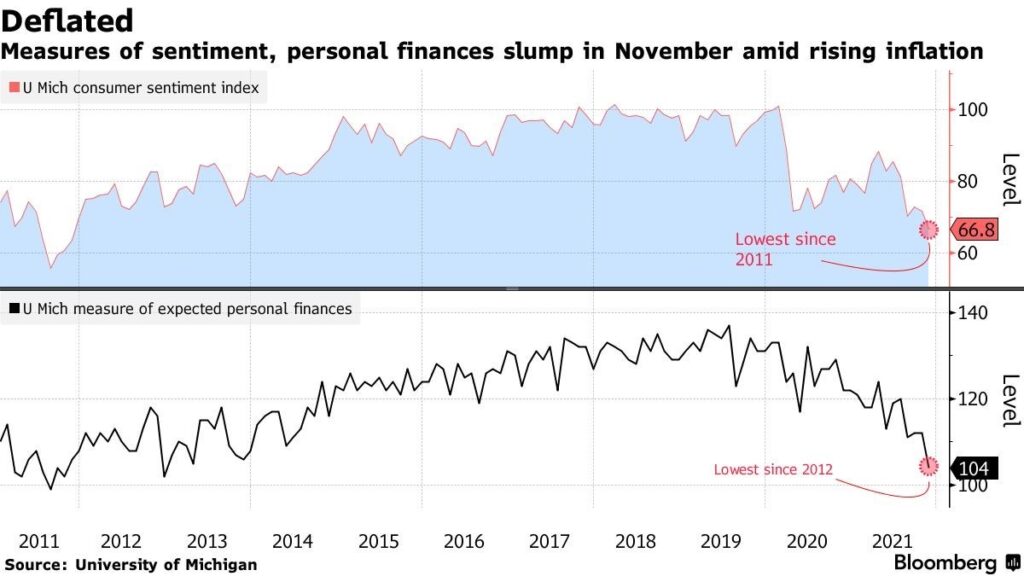

One number released last week that is worrisome was U.S. Consumer Sentiment (previously called Consumer Confidence). The U.S. Consumer Sentiment, as measured by the University of Michigan unexpectedly fell in early November as Americans grew understandably concerned about rising prices and the inflationary impact on their finances. The University of Michigan’s preliminary sentiment index decreased to 66.8 from 71.7 in October. The November figure was well below all Wall Street Economists’ expectations according to a survey by Bloomberg which had called for an increase of 72.5. (See chart below from U Michigan and Bloomberg).

As we have

stated many times, the consumer is the most important factor in the U.S.

economy as consumption makes up approximately 68-70% of GDP in any given year. A

worried consumer is not what an economic

doctor would ever order. With the holiday season kicking off in about one week,

or earlier if you believe TV ads, it will be

interesting to see if the pent up, cash-flush consumer gets out there and

spends money this year. If there is another twist

to this story, it will certainly be what impact

the supply chain disruptions and

clogged ports will have on holiday shopping and

Santa Wish Lists.

From

an investors point

of view, a perfect hedge against inflation,

and a way to protect one’s portfolio from the impact of rising prices is

to invest in equities, which generally outpace

inflation over time. 2021 is a perfect year to demonstrate this. While

expert

economists are crowing about

the +6.2% inflation rate this year, the

S&P 500 Index is up a stunning +26.2%. Always

remain focused on the big picture.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. GDP growth decelerated to a 2% annualized pace in Q3. The slowdown was driven primarily by supply chain constraints. Economists expect a modest acceleration in Q4.

CORPORATE EARNINGS

POSITIVE

With 92% of S&P 500 companies having reported Q3 results, sales and earnings are up 17.5% and 39%, respectively. However, company commentary suggests that the supply chain has been and will continue to be problematic in the coming quarters.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 4.6%, as of October. The labor market is very tight at present many employers, particularly in the Leisure and Logistics sectors, are struggling to fully staff because the labor participation rate remains below pre-COVID levels. The labor shortage is one of the causes of the global supply chain glut.

INFLATION

NEUTRAL

CPI rose 6.2% year-over-year in October, the highest increase since 1990, driven by the global supply chain backlog.

FISCAL POLICY

POSITIVE

A $1.2 trillion infrastructure bill was passed by Congress. An additional $2 trillion tax and stimulus bill proposed by the Democrats will next be voted on by the House & Senate.

MONETARY POLICY

POSITIVE

The Fed will begin bond tapering by November’s end. By mid-2022, all Fed bond purchases will halt. The Fed’s bong buying program works to keep interest rates low.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

Although the Taliban’s control in Afghanistan is concerning, it is unlikely to have a meaningful economic impact.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions are hampering the economy; however, demand remains very strong. While global logistics are operating far below normal efficacy, it appears the supply chain is slowly improving and may reach normalcy by mid-to-late-2022.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie will discuss: Year-End Tax Planning

Laurie can address questions on the air that are submitted either in advance or during the live show via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.