Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie will answer a fourth installment of Listener Tax Questions.

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

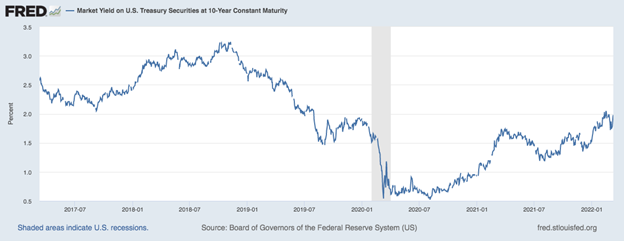

by William Henderson, Chief Investment Officer All major market indexes fell last week adding to an already poor start of the year in equity markets. Even a wild upward rally on Wednesday was not enough to thwart negative returns across the board. The Dow Jones Industrial Average fell -2.0%, the S&P 500 Index fell -2.9% and the NASDAQ lost -3.5%. Year-to-date returns have stayed well into negative territory for all three major market indexes. Year-to-date, the Dow Jones Industrial Average is down -8.9%, the S&P 500 Index is down -11.5% and the NASDAQ has moved into technical “Bear Market” territory being down -17.8%. The Russia / Ukraine war has taken a triple toll on the markets: pushing oil higher, further impacting overall inflation, and finally impacting U.S. Consumer Sentiment. Inflation fears and this week’s FOMC (Federal Open Market Committee) meeting, where markets are expecting the Fed to raise interest rates for the first time in three years, negatively impacted U.S. Treasury bonds leaving us with a very volatile week in fixed income markets. After finishing the previous week at 1.73%, the yield on the 10-Year U.S. Treasury bond jumped last week by 27 basis points to close at 2.00%. (See the chart below from the Federal Reserve Bank of St. Louis).

The yield on the 10-Year U.S.

Treasury is now well off the dramatic all-time low of 0.50% hit during the peak

of the COVID-19 outbreak and is working its way back to pre-pandemic levels.

However, even as market participants are seeing higher yields, remember that if

fear and uncertainty exist investors will need the risk management provided by

fixed income securities.

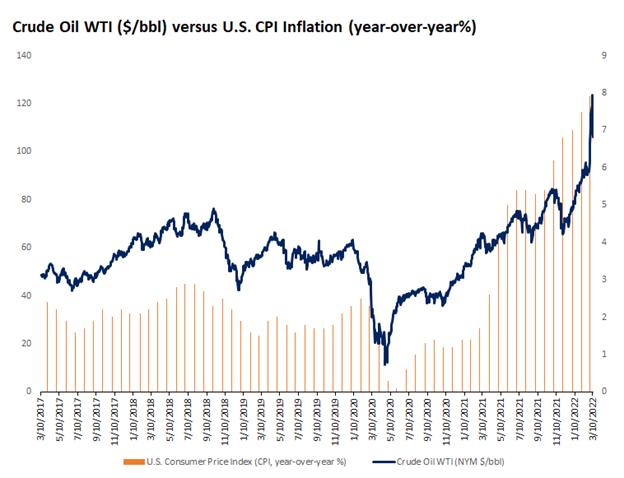

As mentioned, inflation, as

measured by the U.S. CPI (Consumer Price Index), for February 2022 came in at

7.9% versus 2021, a 40-year high. All sectors, led by higher energy prices, showed

increases including food and rent. See the chart below from FactSet showing oil

prices (WTI Crude – left scale) and Inflation (U.S. CPI – right scale) and

their close correlation.

Critically, understand that the

inflation data is backward looking information from February 2022 and therefore

has not even considered the recent run up in oil prices during the month of

March. This gives us a lot more confidence around the Fed’s plan for higher

interest rates soon.

Another data point that has us

worried was last week’s release of the March preliminary University of Michigan

Consumer Sentiment Index (previously called Consumer Confidence Index), which

came in lower than expected at 59.7, versus a Bloomberg estimate of 61.0. At

that level, the measure of consumer sentiment is the lowest since 2011 and well

off the highs hit at the beginning of 2021 when COVID-19 was waning, and the

geopolitical climate was a lot calmer. Throw in significantly higher oil prices

and you get a worried consumer. (See the chart below from YCharts and Valley

National Financial Advisors showing U.S. Consumer Sentiment since April 2021).

We always talk about the

efficiency of the markets, and we believe this to be the case today as

always. Last week’s wild ride in the markets saw a 650-point (+2%) swing in the

Dow Jones Industrial Average on Tuesday based on rumors of positive comments

from Russian leader Vladmir Putin and hints of a ceasefire. This upward move

was quickly reversed when peace talks fell apart and instead Russian invasions

efforts into Ukraine intensified. As we write this report, ceasefire whispers

are again underway, and markets are rallying. The international pressure on

Russia and by decree on Vladmir Putin are enormous. Aside from blocking

monetary transactions on SWIFT, an oil embargo by the west and severe sanctions

elsewhere, the U.S. Department of Justice announced an intense “hunt” for

assets held in the U.S. belonging to Russian Oligarchs. Putin was desperate

enough to ask China for military and economic aid for its Ukraine war.

This action was met swiftly with rebuke from Washington strongly advising China

against any assistance whatsoever with Russia. In fact, this week, Washington

officials are scheduled to meet with Chinese counterparts in Rome to discuss

the war.

It is difficult to see any

outcome for Russia that ends well. The only plausible endgame is for a

negotiated solution between Ukraine and Russia that gives Putin something yet

allows Ukraine to remain and independent state. Unfortunately, if the war drags

on, uncertainty and fear will persist, and the markets will react accordingly.

Beyond the humanitarian impact the war is having, prices of such commodities as

oil, natural gas and palladium are skyrocketing and inflation is the result

which further impacts consumers and eventually economic growth. Expect

inflation to continue for longer but the Fed will be on the move this week and

their new objective will be to combat inflation. This week’s FOMC meeting will

be important for reasons beyond the expected 25 basis point rate hike. The

markets will be watching for language around the pace of future hikes and the

scope of balance sheet reduction. This may add some calm and clarity to the

markets, but it could be overshadowed by any breakdown in peace talks or unwelcomed

involvement from China.

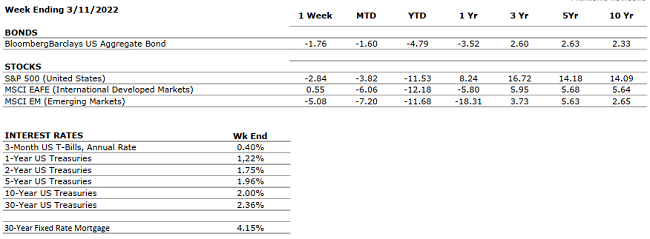

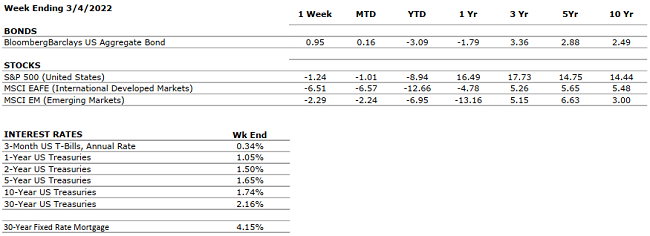

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. Real GDP growth for Q4 2021 increased at an annual rate of 7.0% compared to 2.3% in Q3 (according to second estimate). The acceleration was driven primarily by private inventory investment. Real GDP increased by 5.7% in 2021 versus a decrease of -3.4% in 2020. Disposable income saw a slight increase of 0.3% and personal saving rate decreased to 7.4% in Q4 from the previous 9.5% in Q3 highlighting increased consumer spending.

CORPORATE EARNINGS

POSITIVE

Fourth quarter earnings are showing strong results with 76% of companies that reported earnings so far beating estimates by an average of 8.2%. Revenues also well above estimates with 78% of S&P 500 companies reporting actual revenue above forecasts. Blended earnings growth rate for 2021 was 30.7%. So far, 99% of S&P500 companies have reported earnings.

EMPLOYMENT

POSITIVE

Total nonfarm payroll employment rose by 678,000 in February, and the unemployment rate edged down from 4% to 3.8%. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, health care, and construction.

INFLATION

NEGATIVE

CPI rose 7.5% year-over-year in January 2022, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Inflation concerns are clearly impacting the markets, the FED and consumer behavior. February inflation numbers to be released on March 10th.

FISCAL POLICY

NEUTRAL

President Biden is shifting from the Build Back Better Bill to a four-point economic rescue plan. Emphasis on reducing deficits and containing inflation will be critical to sway Senator Manchin. The four points will be: moving goods cheaper and faster, reducing everyday costs, promoting competition, and eliminating job barriers.

MONETARY POLICY

NEUTRAL

Fed discussed a triple threat of tightening: raise interest rates, halt purchases, and reduce its balance sheet (reducing holdings of Treasurys and mortgage-backed securities). Gradual and steady reduction of liquidity will be key in preserving market performance (fast and sudden changes would most likely result in panic-driven sell offs). Upcoming Fed meeting on March 15- 16.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

The Russian invasion into Ukraine has now turned into a full-blown global event. US, UK and EU authorities are taking many steps to cripple Russia including closing their access to SWIFT. Commodity prices are spiking along with Oil. COVID-19 concerns continue to abate and re- openings are more the norm than closures and lockdowns. The CDC is easing rules.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but the rising cost of oil due to the Russian-Ukraine war is likely to cause additional inflationary pressures not only on gasoline prices but also many other goods and services.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Education Savings Plans Parents with young children, are faced with many rewards and challenges. One of which may be saving for the high cost of a college education. However, there are two tax-favored options that might be beneficial: READ MORE

Education Tax Credits There are two credits available to help taxpayers offset the costs of higher education. The American opportunity tax credit (AOTC) and the lifetime learning credit (LLC) may reduce the amount of income tax owed. Taxpayers who pay for higher education can see these tax savings when they file their tax returns next year. READ MORE

Tune in

Wednesday, 6 PM for “Your Financial Choices” on WDIY 88.1FM. Guest hosts Rodman Young, CPA/PFS, CFP® and Jaclyn Cornelius, CFP®,

EA will discuss: Tax

Planning with Retirement Accounts

by William Henderson, Chief Investment Officer While domestic resiliency was present last week with strong jobs and earnings numbers, volatility related to the war in Ukraine won the week over and all three major market indexes closed lower. The Dow Jones Industrial Average fell -1.3%, the S&P 500 Index also fell -1.3% and the NASDAQ fell by -2.8%. Year-to-date returns continue to be unfavorable across all sectors and indexes. Year-to-date, the Dow Jones Industrial Average is down -7.2%, the S&P 500 Index is down -8.9% and the NASDAQ is down -14.8%. As a result of the uncertainty, fear, and volatility the “risk-off” trade occurred in the bond market and the prices of U.S. Treasury bonds moved dramatically higher sending yields sharply lower. The yield on the 10-Year U.S. Treasury fell 23 basis points from last week to close the week at 1.74% – a stunning move considering the path the Fed has laid out this year for interest rates. What this move tells us is that the safety and liquidity of U.S. Treasury bonds currently trumps everything else, including the Fed’s well-telegraphed plan of raising short-term interest rates.

The move in U.S. Treasury yields

further “flattened” the yield curve. If the yield

curve (the

measure of 10-year yields minus two-year

yields) is flattening, it indicates the yield

spread between long-term and short-term bonds is decreasing. The

yield curve is often a reliable indicator of economic and monetary policy

conditions. The recent yield curve flattening is

a result of two-year Treasury bond rates rising

in

anticipation of Fed policy rate hikes; while 10-year rates

declined, due to the flight to safety trade resulting from increased concerns

over the war in Ukraine. (See the chart below from the Federal Reserve

Bank of St. Louis showing the 10s – 2s spread and the

dramatic decline since mid-year 2021).

While a

downward movement in the 10s – 2s spread has

historically preceded an impending recession, we do not believe this to be the

case now due to the sound underlying fundamentals of the U.S. economy including

strong continued employment gains and near-record

profits by corporations. According to FactSet, with the recent fourth

quarter 2021 earnings season concluding last

week,

companies in the S&P 500 recorded average earnings gains of 31% over the

fourth

quarter of 2020. With such solid underlying economic fundamentals,

why are the markets exhibiting such

volatility and negative returns year-to-date? Fear and uncertainty!

These are and will always be the worst

thing for markets. When you cannot measure the risk, the risk-off trade

prevails, and investors sell stocks and buy bonds. Additionally,

the Ukraine war and resulting severe sanctions on Russia are impacting many

commodity prices, further

exacerbating already hot-running inflation. This reaction again may be

more than necessary, while oil spikes occurring are understood as Russia is a

large supplier of oil to the world, their impact on the global economy is much

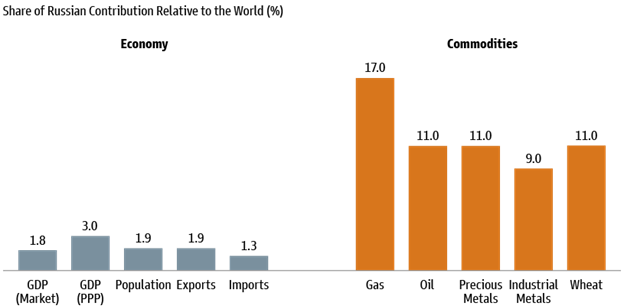

less than one would think. See the chart below from Haver Analytics and

Goldman Sachs showing Russia’s contribution to the global economy and Russia’s

production percent of important commodities.

Presently, oil is the biggest

shock to the market and the price of WTI Crude has spiked to

$130/barrel. Oil, as we have stated many times,

is a key component in many household

and industrial goods way beyond refined fuels for planes, trains, and

automobiles. Oil is used in clothing (nylon & polyester), plastics,

agriculture (pesticides & fertilizers), tools and toys – frankly – it is

everywhere and when the price of oil rises, inflation is the result. These

events – global slowdown in activity due to sanctions on Russia and the

resulting inflationary impacts – puts the Fed in a quandary. Fed Chairman Jay

Powell must raise rates to combat inflation but now he also risks slowing the

economy at a time when things are precarious as the Russia/Ukraine war

evolves. And thus, we have the uncertainty that the markets hate.

Western nations are united in

sanctioning Russia for starting the

war

with Ukraine. China, a strategic and economic partner of Russia, has not

officially condemned the incursion but has stated succinctly that “all sides

exercise restraint and avoid escalation.” While not a stern rebuke like

the west, it may be the best we can expect from China, who selfishly understands

any global economic slowdown will directly hurt their pocketbook. The

obvious question is which side yields first – Russia led by Vladimir Putin, a

former KGB Officer or Ukraine led by Volodymyr Zelenskyy,

a

former

TV

actor

and his western “allies.” Again – uncertainty, and again – volatility in

the markets.

Balanced

portfolios with risk management tools like bonds help in times like

this. What helps best is a level head and a long-term outlook on

investments.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. Real GDP growth for Q4 2021 increased at an annual rate of 7.0% compared to 2.3% in Q3 (according to second estimate). The acceleration was driven primarily by private inventory investment. Real GDP increased by 5.7% in 2021 versus a decrease of -3.4% in 2020. Disposable income saw a slight increase of 0.3% and personal saving rate decreased to 7.4% in Q4 from the previous 9.5% in Q3 highlighting increased consumer spending.

CORPORATE EARNINGS

POSITIVE

Fourth quarter earnings are showing strong results with 76% of companies that reported earnings so far beating estimates by an average of 8.2%. Revenues also well above estimates with 78% of S&P 500 companies reporting actual revenue above forecasts. Blended earnings growth rate for 2021 was 30.7%. So far, 95% of S&P500 companies have reported earnings.

EMPLOYMENT

POSITIVE

U.S. Payroll Report for January U.S. added 467,000 jobs in January, beating estimates of 125,000. Red-hot private sector hiring drives the payrolls surge. Revisions add 709,000 jobs in prior two months. Unemployment rate rises to 4% from 3.9%.

INFLATION

NEGATIVE

CPI rose 7.5% year-over-year in January 2022, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Inflation concerns are clearly impacting the markets, the FED and consumer behavior.

FISCAL POLICY

NEUTRAL

President Biden is shifting from the Build Back Better Bill to a four-point economic rescue plan. Emphasis on reducing deficits and containing inflation will be critical to sway Senator Manchin. The four points will be: moving goods cheaper and faster, reducing everyday costs, promoting competition, and eliminating job barriers.

MONETARY POLICY

NEUTRAL

Fed discussed a triple threat of tightening: raise interest rates, halt purchases, and reduce its balance sheet (reducing holdings of Treasurys and mortgage-backed securities). Gradual and steady reduction of liquidity will be key in preserving market performance (fast and sudden changes would most likely result in panic-driven sell offs). Upcoming Fed meeting on March 15- 16.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

The Russian invasion into Ukraine has now turned into a full-blown global event. US, UK and EU authorities are taking many steps to cripple Russia including closing their access to SWIFT. Commodity prices are spiking along with Oil. COVID-19 concerns continue to abate and re- openings are more the norm than closures and lockdowns. The CDC is easing rules.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but now there are trucker protests on the Canadian / U.S. border. Canada is the second largest trading partner with the U.S. (after China) but our largest export market.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.