VNFA Partners with WDIY Again to Support Second Harvest Food Bank This week kicks off WDIY’s Fall Membership Drive during which Valley National Financial Advisors will again donate to provide meals through Second Harvest Food Bank. VNFA has supported the partnership since 2017 and last year was able to fund 12,128 meals for those in need across the Lehigh Valley.

Every dollar donated to WDIY during this year’s Fall Membership Drive will help provide meals to those in need in the Lehigh Valley. For every $100 WDIY receives in donations, Second Harvest Food Bank of the Lehigh Valley will provide 21 meals to individuals and families in our community. READ MORE

October is Cybersecurity Awareness Month AND Financial Planning Month

Cybersecurity TIP by Rob Ziobro, AVP Technology What is the one thing keeping people from gaining access to your accounts? Your PASSWORD! So, would you feel protected when using a generic password like Password or 123456? And so many people do just that. We recommend using the most secure password as possible. Something with UPPER case, lower case, numbers, and symbols is great, and the longer the better. Did you know that a longer password is can technically be stronger than a shorter, complex password? It’s due to its Entropy! Entropy is a calculation of password randomness in bits. Next week: find out how we can add another layer of security on to your accounts.

Financial Planning TIP by Jaclyn Cornelius, CFP®, EA – VP / Financial Advisor In times like we are currently experiencing (current market downturn), we suggest that clients be in more communication with us (their financial advisor). Everything from their thoughts, big financial decisions, upcoming cash flow needs or any other potential changes. We find that increased communication is an important key to weathering storms like what we are all going through right now. We often check back against the Financial Plan we prepared and that helps calm a client’s nerves to see that they are still on track given current market conditions.

While market volatility was more modest than the previous two weeks, major U.S. stock indexes fell nearly 3%, declining for the sixth time in the past seven weeks. Further, the Dow Jones Industrial Average on Monday joined the S&P 500 and the NASDAQ in bear market territory, as the Dow declined more than 20% from its level of early January. In contrast, U.S. bonds rallied as the yield on the 10-Year U.S. Treasury fell five basis points during the week to close at 3.83% and well off its recent high of 3.95%. Multiple concerns continue to plague markets including lingering inflation, Russia/Ukraine war, impacts of Hurricane Ian in Florida and greater chances of a modest recession.

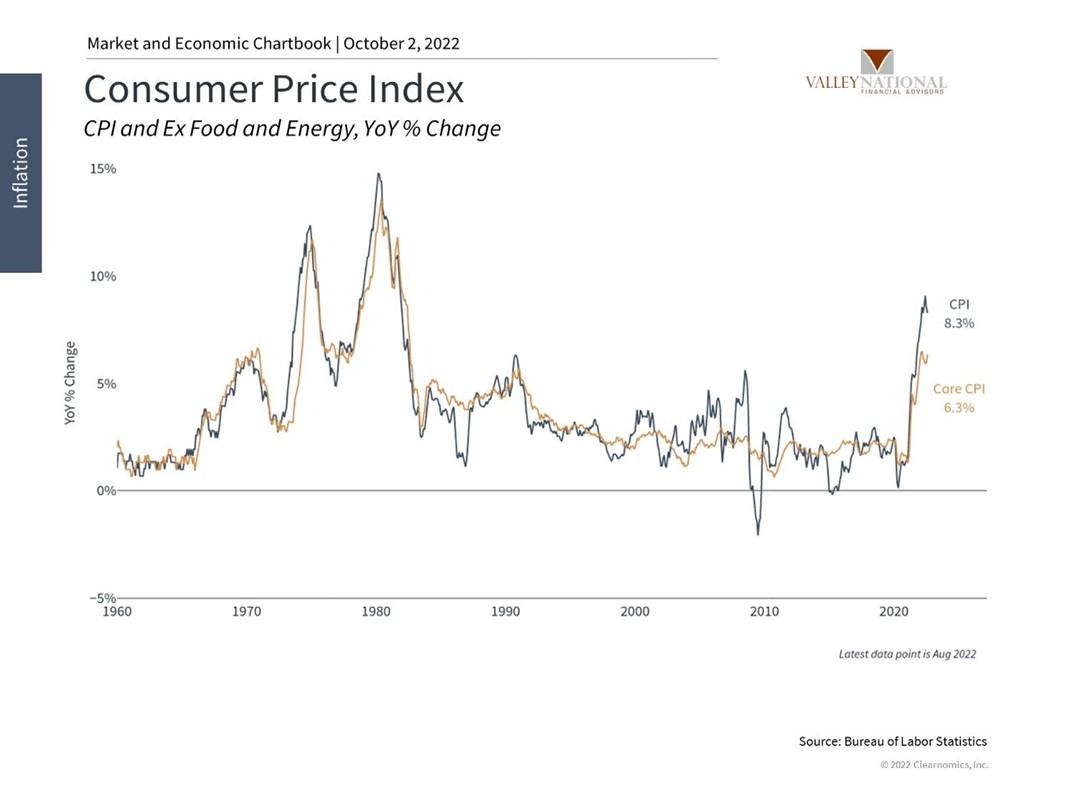

Global Economy Global inflation certainly is the major issue impacting markets and until we see tangible results of the FED’s interest rate tightening policy on inflation, the market will remain volatile and data dependent from week to week. Massive cash creation at the Federal level, global supply chain issues and pent-up demand as a result of COVID-lockdowns, created inflation in the form of increased prices for goods and services. Inflation got us here; deflation is the cure.

Thankfully, we are starting to see “behind the scenes” deflationary signals. Major commodities, such as lumber, are down in price to pre-pandemic levels, Trans-Pacific shipping rates are down 75% from a year ago, and Oil (as measured by WTI) is down to $83/bbl. from $123/bbl. in March of this year. (See Chart 1 from Valley National Financial Advisors & Clearnomics showing CPI.) As lower prices work their way through the supply chain to producers, prices offered to consumers should decline as well and the FED will start to see tangible results from their inflation combat efforts.

Policy and Politics The newly elected Prime Minister Truss of the U.K. was forced to do a U-turn on her recently announced plan to scrap the 45% tax rate. The humiliating retracement was due to outrage by Tory MPs at a tax-cut during a time of energy shortages, high prices and market uncertainty.

Russia annexed portions of Ukraine while Vladmir Putin vowed to use all means necessary to assure victory in the war. Meanwhile, Russian forces withdrew from the eastern Ukrainian port city of Lyman, in an obvious defeat. There seems little end to this conflict. Instead, further escalations by both sides does not bode well for Eurozone countries that rely on energy supplies from Russian and Ukraine.

What to Watch

U.S. Job Openings for August 2022, released 10/4/22 (prior month 11.24M)

U.S. Initial Claims for Unemployment for Week of October 1, 2022, released 10/6/22 (prior 193k)

U.S. 30-year Mortgage Rate for Week of October 6, 2022, released 10/6/22 (prior 6.7%)

U.S. Unemployment Rate for September 2022, released 10/8/22 (prior 3.70%)

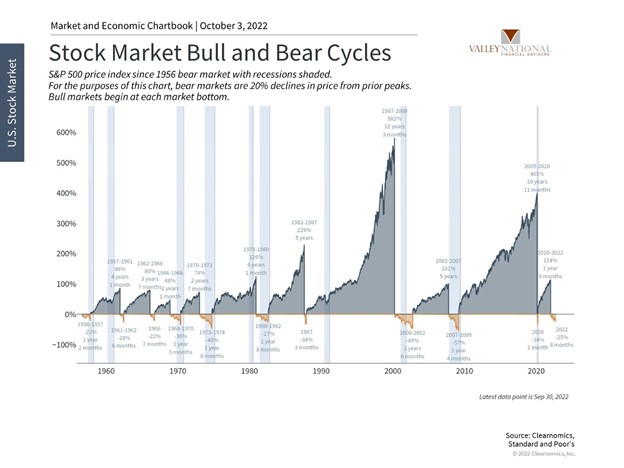

While it seems a tall order to recommend investors “stay the course” or “remain committed” but that remains our recommendation as we advise that true wealth creation happens over long periods of time. Certainly, while being down double-digits across all markets and over nine long months is painful, it is time to steel one’s resolve and stay invested. This tenet is even more relevant when the very definition of a risk-free investment, three-month U.S. Treasuries, are paying 3.23%, and enticing investors to flee the markets rather than stay invested. Bull Markets are always punctuated by Bear Markets and Bear Markets last, on average, 14 months, while Bull Markets last, on average, five years or more (See Chart 2 from Valley National Financial Advisors & Clearnomics showing Stock Market Cycles 1960-current).

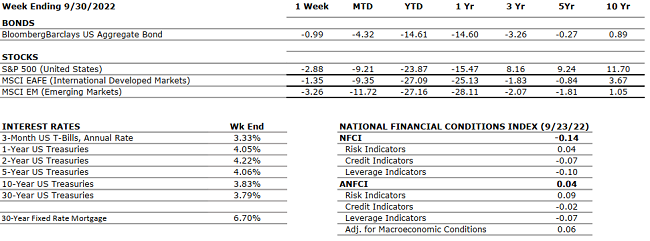

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Q1 2022 Real GDP shrunk at a 1.6% annual rate. The main factors that resulted in a decrease in GDP were a surge in imports and trade deficit highlighting that the U.S. is buying more goods from foreign countries. According to the second estimate, real GDP for Q2 2022 decreased at an annual rate of 0.6% (up from the first estimate of -0.9%) marking the second consecutive quarter of declining GDP.

CORPORATE EARNINGS

NEUTRAL

The earnings growth rate for Q2 2022 was 6.7% (up from previous estimates of 4.3%) which marked a new post-pandemic low; but still solidly in the “growth” stage. The estimated growth rate for Q3 2022 is 2.9%, which was adjusted downward from 9.8% in June. Ten out of 16 S&P 500 companies that reported earnings beat estimated EPS and 10 beat revenue expectations.

EMPLOYMENT

NEUTRAL

U.S. Nonfarm Payrolls for August 2022 increased by 315,000 and the unemployment rate for August rose slightly to 3.7% compared to 3.5% in July. Professional and business services, health care, and retail trade were among the sectors with the most notable job gains.

INFLATION

NEGATIVE

The annual inflation rate in the U.S. increased by 8.3% for August 2022 — below the 8.5% in July but above the expected 8.1%. Food prices saw the largest increases since 1979 (11.4%), shelter and used cars also impacted inflation significantly. Core CPI increased 6.3% year-over-year, the most since March, and up from 5.9% in both June and July.

FISCAL POLICY

NEUTRAL

Senator Manchin and Majority Leader Schumer reached an agreement on the latest tax and energy bill with incentives for green energy, electric cars, and conversely oil & gas companies for exploration. No changes in private equity taxes or higher tax rates for the very wealthy were enacted. The bill has been officially passed by the Senate. Last week, President Biden announced student loan forgiveness of up to $20,000 subject to income limitations.

MONETARY POLICY

NEGATIVE

With inflation still running hot, Fed Chairman Jay Powell is clear on his path to slow the economy enough to cool inflation. The Fed raised rates by 0.75% last week, bringing its target rate to 3.00- 3.25%, and suggesting that additional rate hikes are likely in the coming months.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

Russia held controversial referendums for the annexation of four Ukrainian regions and the Russian Parliament unanimously recognized these regions as part of Russia. Ukraine and Western countries have condemned these actions by Russia by declaring them illegitimate and illegal. Additional sanctions are being imposed on Russia by many countries.

ECONOMIC RISKS

NEGATIVE

COVID-19 lockdowns in China are persistent and the ongoing Russian-Ukraine war is causing a major energy crisis in Europe. Putin shut down the pipeline that supplies Europe with natural gas indefinitely until all sanctions affecting Russia are lifted. European countries are struggling to find alternative energy resources and are starting to implement significant restrictions on the use of energy in households and businesses.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Questions can be submitted at yourfinancialchoices.com during or in advance of the live show. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.