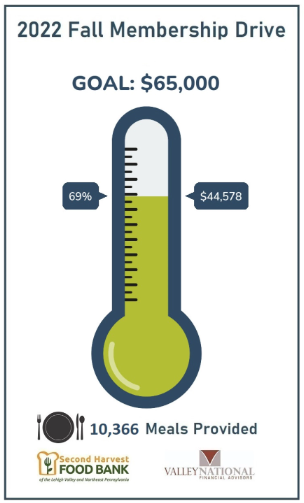

The WDIY Fall Membership Drive continues this week, and Team VNFA’s partnership has so far resulted in more than 10,000 meals to be funded for Second Harvest Food Bank.

For every $100 pledged to WDIY during the membership drive, Valley National Financial Advisors will donate to allow Second Harvest to provide 21 meals to individuals and families in our community.

October is Cybersecurity Awareness Month AND Financial Planning Month

THE REAL VALUE OF A FINANCIAL PLAN by Jonathan Ritter, CFP®, CPA “The process of financial planning can help guide you through complicated financial decisions so you can have less stress and more time to focus on the things that matter to you. The time you don’t have to spend worrying about financial uncertainty can be devoted to activities that bring you enjoyment rather than anxiety and frustration.”

Clients are most appreciative and thankful when we prepare a plan and provide them with strategies to accomplish their financial goals.

CYBERSECURITY TIP by Robert Ziobro, AVP Technology Do you know about Phishing? Phishing is a cybercrime in which a target or targets are contacted by email, telephone, or text message by someone posing as a legitimate institution to lure individuals into providing sensitive data such as personally identifiable information, banking and credit card details, and passwords. The information is then used to access important accounts and can result in identity theft and financial loss.

Here are some common features to look for:

Too Good To Be True – Lucrative offers and eye-catching or attention-grabbing statements are designed to attract people’s attention immediately. For instance, many claim that you have won an iPhone, a lottery, or some other lavish prize. Just don’t click on any suspicious emails. Remember that if it seems to good to be true, it probably is!

Sense of Urgency – A favorite tactic amongst cybercriminals is to ask you to act fast because the super deals are only for a limited time. Some of them will even tell you that you have only a few minutes to respond. When you come across these kinds of emails, it’s best to just ignore them. Sometimes, they will tell you that your account will be suspended unless you update your personal details immediately. Most reliable organizations give ample time before they terminate an account, and they never ask patrons to update personal details over the Internet. When in doubt, visit the source directly rather than clicking a link in an email.

Hyperlinks – A link may not be all it appears to be. Hovering over a link shows you the actual URL where you will be directed upon clicking on it. It could be completely different, or it could be a popular website with a misspelling, for instance www.bankofarnerica.com – the ‘m’ is actually an ‘r’ and an ‘n’, so look carefully.

Attachments – If you see an attachment in an email, you weren’t expecting or that doesn’t make sense, don’t open it! They often contain payloads like ransomware or other viruses. The only file type that is always safe to click on is a .txt file.

Unusual Sender – Whether it looks like it’s from someone you don’t know or someone you do know, if anything seems out of the ordinary, unexpected, out of character or just suspicious in general don’t click on it!

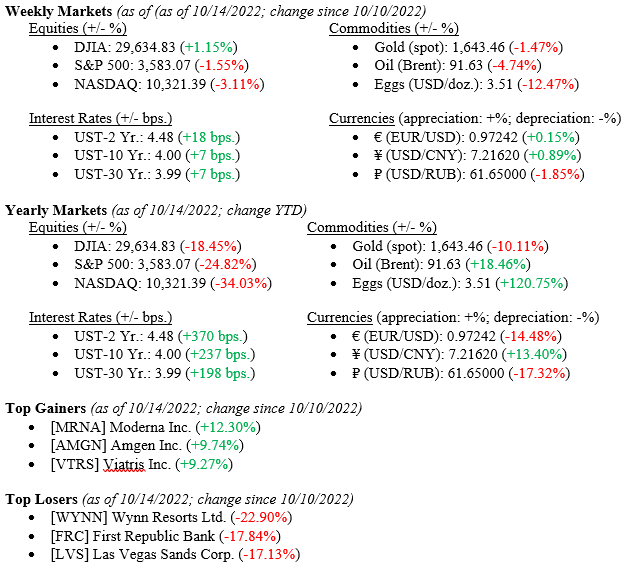

Last week we saw major markets diverge for the first time this year. The Dow Jones Industrial Average notched out a +1.15% return while the S&P 500 Index (-1.55%) and the NASDAQ (-3.11%) each posted negative returns. This divergence of returns is emblematic of the market and economy themselves with economists calling a pending recession while real data – jobs, bank balance sheets, Earnings Per Share (EPS) releases and consumer health – remains healthy if not growing in strength.

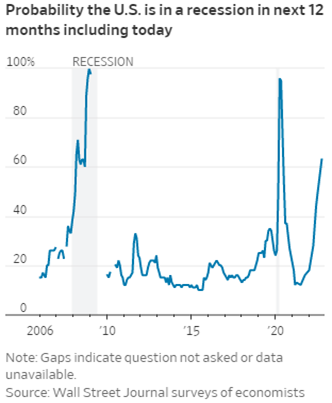

Global Economy U.S. economists are beginning to increasingly predict a recession within the next 12 months. On average, economists put the probability of a coming recession at 63%, up from 49% in July. This is the first time since July 2020 that the survey has yielded a result above 50%. Additionally, the survey suggests that GDP (Gross Domestic Product) will contract at

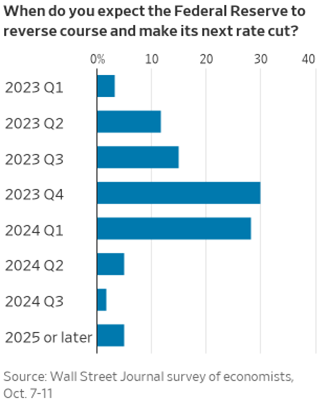

-0.2% on an annual basis during Q1 2023 and -0.1% in Q2 2023. These predictions come as doubts heighten over the Fed’s ability to tame inflation without inducing increased unemployment. Two-thirds of those surveyed believe the Federal Reserve will pivot in either Q4 2023 or Q1 2024.

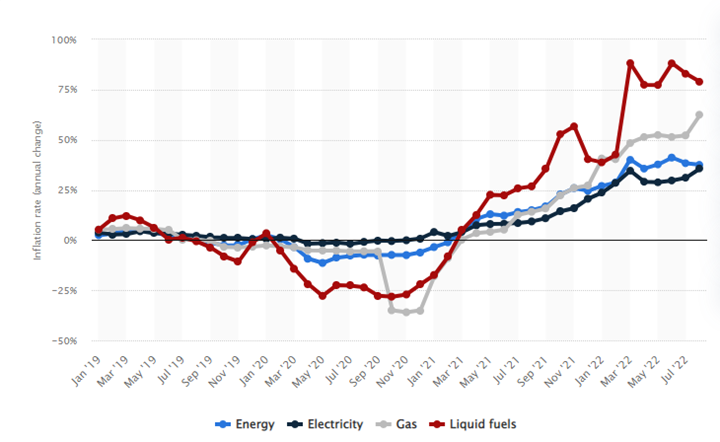

European Union leaders are meeting on October 20 and 21 to discuss potential implementation options for a cap on gas prices. After Russia’s invasion of Ukraine, the Kremlin vastly reduced gas exports to Europe as retaliation for the economic sanctions the country received. Energy in the EU is becoming prohibitively expensive, raising concerns for a rough winter over the next few months. The annual inflation rate for energy is currently standing at 37.5%, with electricity at 35.7%, gas at 62.5%, and liquid fuels at 78.9%.

What to Watch

Monday, October 17th

4:30PM: US Retail Gas Price (Prior: $4.034/gal.)

Wednesday, October 19th

8:30AM: US Housing Starts (Prior: 1.575M)

8:30AM: US Housing Starts MoM (Prior: 12.18%)

10:00AM: US Job Openings, Total Nonfarm (Prior: 10.05M)

Thursday, October 20th

10:00AM: 30-Year Mortgage Rate (Prior: 6.92%)

10:00AM: US Existing Home Sales (Prior: 4.80M)

10:00AM: US Existing Home Sales MoM (Prior: -0.41%)

While calls for a recession mount mostly on economist’s note pads and TV prognosticator’s teleprompters, the underlying fundamentals of the U.S. economy remain solid as we stated above. If we get a recession, the economy starts with a real safety net that did not exist in the 2008-09 recession, thereby guaranteeing said recession is neither deep nor lengthy. Opportunities mount in fixed income (now offering yields north of 4.00%) and equities (now trading ~19x forward EPS & yields ~2.00% on the S&P 500 Index) offering investors good entry points for continued long-term wealth creation.

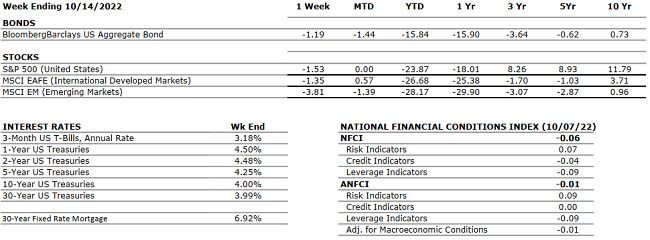

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Q1 2022 Real GDP shrunk at a 1.6% annual rate. The main factors that resulted in a decrease in GDP were a surge in imports and trade deficit highlighting that the U.S. is buying more goods from foreign countries. According to the second estimate, real GDP for Q2 2022 decreased at an annual rate of 0.6% (up from the first estimate of -0.9%) marking the second consecutive quarter of declining GDP. Some retail outlets are reporting excess inventories which could signify a slowdown in consumer demand.

CORPORATE EARNINGS

NEUTRAL

The estimated growth rate for Q3 2022 is 1.6%, which was adjusted downward from 9.8% in June and 2.4% last week. So far, with 7% of S&P500 companies reporting actual results, 69% of them reported a positive EPS surprise and 67% beat revenue expectations.

EMPLOYMENT

NEUTRAL

U.S. Nonfarm Payrolls for September 2022 increased by 263,000 and the unemployment rate fell back to the June and July level of 3.5% after spiking slightly in August to 3.7%. Professional and business services, health care, and leisure and hospitality were among the sectors with the most notable job gains.

INFLATION

NEGATIVE

The annual inflation rate in the U.S. increased by 8.2% for September 2022 — down slightly from 8.3% in August but still a stubbornly high result and above expectations. Core CPI increased by 6.6% year-over-year marking the highest gain since August 1982. Food and shelter were the main contributors to the increase in CPI, gasoline index fell slightly but overall energy prices are expected to rebound again. Used car prices are also not declining as much as expected.

FISCAL POLICY

NEUTRAL

Senator Manchin and Majority Leader Schumer reached an agreement on the latest tax and energy bill with incentives for green energy, electric cars, and conversely oil & gas companies for exploration. No changes in private equity taxes or higher tax rates for the very wealthy were enacted. The bill has been officially passed by the Senate. Last week, President Biden announced student loan forgiveness of up to $20,000 subject to income limitations.

MONETARY POLICY

NEGATIVE

With inflation still running hot, Fed Chairman Jay Powell is clear on his path to slow the economy enough to cool inflation. The Fed raised rates by 0.75% in September, bringing its target rate to 3.00-3.25%, and suggesting that additional 75bps rate hikes are likely in the coming months.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

Russia held controversial referendums for the annexation of four Ukrainian regions and the Russian Parliament unanimously recognized these regions as part of Russia. Ukraine and Western countries have condemned these actions by Russia by declaring them illegitimate and illegal. Additional sanctions are being imposed on Russia by many countries.

ECONOMIC RISKS

NEGATIVE

COVID-19 lockdowns in China are persistent and the ongoing Russian-Ukraine war is causing a major energy crisis in Europe. Putin shut down the pipeline that supplies Europe with natural gas indefinitely until all sanctions affecting Russia are lifted. Gas supplies from Russia to Europe have decreased by 88% over the past year and EU countries have agreed to cut gas usage by 15% as gas prices have more than doubled.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” on WDIY 88.1FM. Laurie and her guest Catherine Bailey of SCORE Lehigh Valley will discuss: Small Business Mentorship

Questions can be submitted at yourfinancialchoices.com during or in advance of the live show. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.