Our Chief Investment Officer William Henderson talks about very important topics this week – he explains the recession meter used by VNFA, talks about inflation, and shares some tips on the differences between Bull and Bear markets.

Daily Archives: November 1, 2022

Did You Know…?

November is Alzheimer’s Awareness Month

According to The Alzheimer’s Association financial planning often gets pushed aside when a person is dealing with the stress of their diagnose. Here are four steps that will help you when planning.

- Knowing where to begin.

- What care cost?

- How will you pay for care?

- What professional assistance is available?

Want to dive into “Financial Planning” read the full article by The Alzheimer’s Association on what steps to take for your financial future.

Current Market Observations

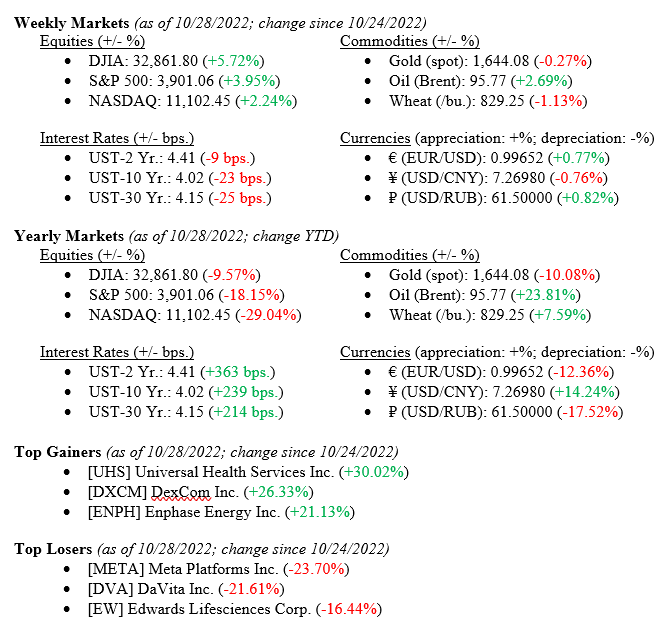

Last week, we saw diverging pressures on the markets resulting in diverging results on equity indexing. Hopes of a FED slowing their aggressive interest rate hikes moved equity markets higher across the board and bond yields lower, but weak earnings releases from “Big Tech” equities (AMZN, GOOG, META) weighed heavily on the tech-heavy NASDAQ. Still, all major indexes moved higher for the week (see details below) and the 10-Year US Treasury ended the week at 4.02%, 23 basis points lower than the previous week.

Weekly Markets (as of 10/28/2022; change since 10/24/2022)

Global Markets

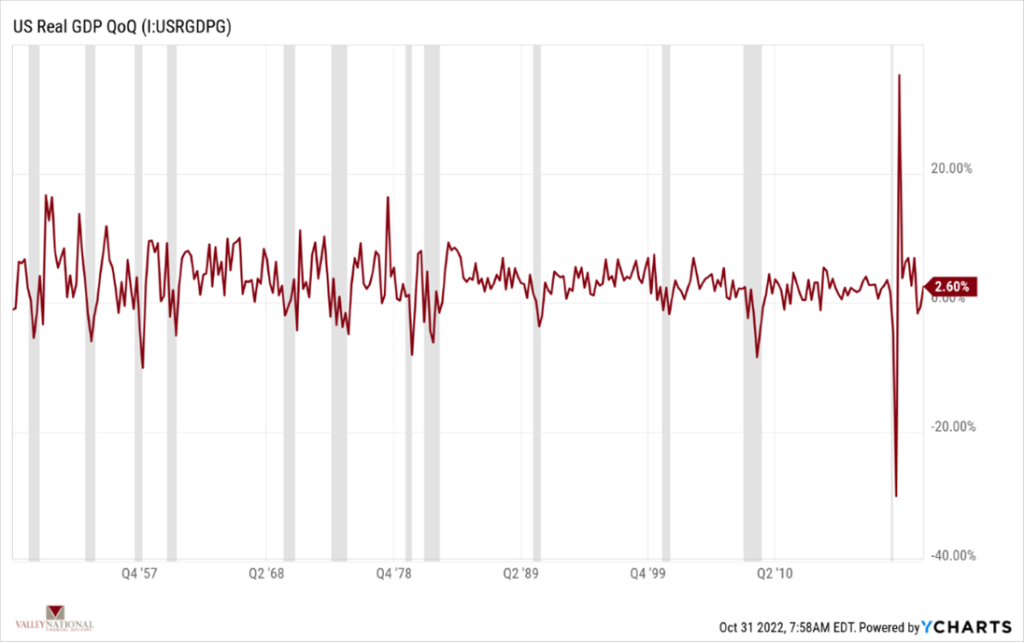

As noted above, weekly returns were favorable across all major indexes and returns for the full month of October 2022 are shaping up to be some of the best monthly returns in decades. Solid consumer spending, as evidenced by earnings releases from Visa and American Express, continue to fuel economic growth. Last week, U.S. Real GDP (Gross Domestic Product) for the 3rd quarter was released and the number came in at +2.60%, compared to -0.60% for the 2nd quarter of 2022 and +2.70% for the full year 2021. (See Chart 1 below from Valley National Financial Advisors & Y Charts). What we found telling was how GDP has now normalized moving closer to recent historical averages compared to wild pandemic-related swings we saw previously.

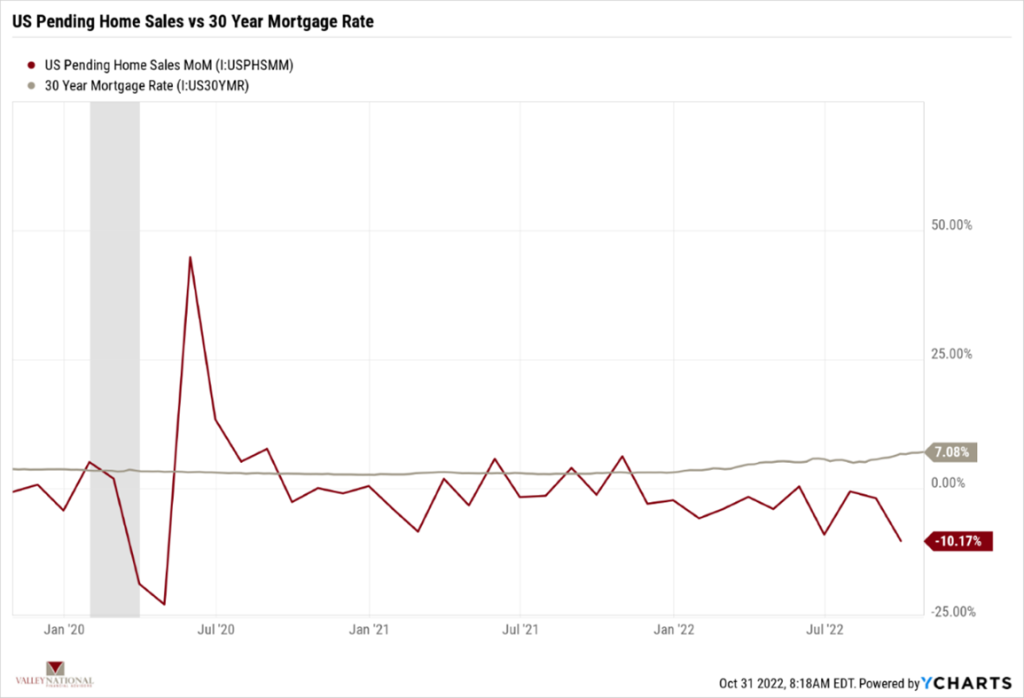

Mortgage rates continue to move higher in response to higher interest rates overall. This has had a drastic impact on the housing market. Last week, the National Association of Realtors released U.S. Pending Home Sales data that was significantly below expectations (-10.17% vs expected of –4.0%) (See Chart 2 below from Valley National Financial Advisors and Y Charts showing the 30 Year Mortgage Rate vs U.S. Pending Home Sales).

While not a devastating impact on the economy, housing is a key component of economic growth especially given the knock-on effects of home sales – additional purchases of appliances, home improvements made, sales of replacement furniture and fixtures all contribute to or detract from economic activity.

This week the Federal Reserve meets, and expectations are for another +0.75% rate hike. This is expected so any move higher or lower will have an impact on the markets because, as we all know, markets hate uncertainty. Additionally, about 1/3 of the S&P 500 Index Companies report earnings this week, which will also have a corresponding impact on the markets if the data is more positive or negative compared to Wall Street analysts’ predictions.

What to Watch

- U.S. Job Openings: Total Nonfarm for September 2022, released 11/01/22 (Prior +10.05m)

- Target Federal Funds Rate by Federal Open Markets Committee released 11/02/22, current upper range 3.25%

- U.S. Initial Claims for Unemployment Ins. for week of 10/29/22, released 11/3/11 (prior 217k)

There has been a modest turnaround in equities and the month of October has rewarded patient investors handsomely. 10-Year US Treasury yields have come off their recent highs (4.33%), moving lower to 4.02% but markets have yet to express optimism that yields have peaked. The FED meets this week and markets have priced in a +0.75% bump in the Fed Funds Target. The language around that move and additional directional information from Fed Chair Jay Powell is what we are really waiting for with Wednesday’s announcement. Global uncertainty is focused on the Russian/Ukraine war and Covid related lockdowns in China – thankfully, these are not new uncertainties, and the markets continue to accurately price in the story. Watch for impactful data this week while also remaining focused on the long-term trends. Reach out to us at Valley National Financial Advisors for any additional information.

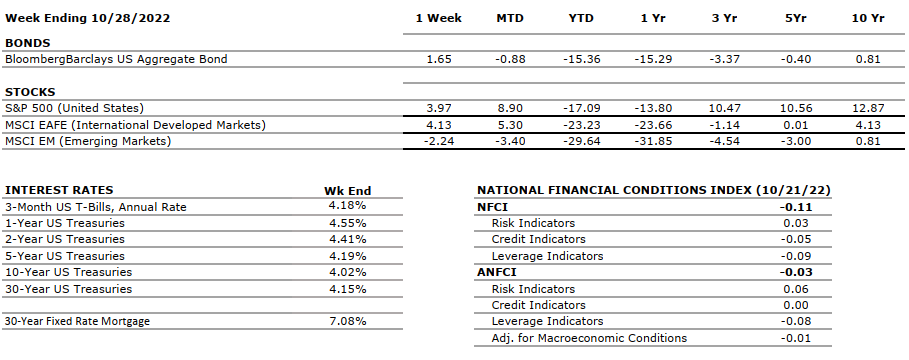

The Numbers & “Heat Map”

THE NUMBERS

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

|

US ECONOMY |

||

|

CONSUMER HEALTH |

NEUTRAL | According to the second estimate, real GDP for Q2 2022 decreased at an annual rate of 0.6% (up from the first estimate of -0.9%) marking the second consecutive quarter of declining GDP. The advance estimate for Q3 2022 shows Real GDP to have increased by an annual rate of 2.6%. |

|

CORPORATE EARNINGS |

NEUTRAL | The estimated growth rate for Q3 2022 is 2.2%, which was adjusted downward from 9.8% in June and 2.4% two weeks ago. So far, with 52% of S&P500 companies reporting actual results, 71% of them reported a positive EPS surprise and 68% beat revenue expectations. |

|

EMPLOYMENT |

NEUTRAL | U.S. Nonfarm Payrolls for September 2022 increased by 263,000 and the unemployment rate fell back to the June and July level of 3.5% after spiking slightly in August to 3.7%. Professional and business services, health care, and leisure and hospitality were among the sectors with the most notable job gains. |

| INFLATION | NEGATIVE | The annual inflation rate in the U.S. increased by 8.2% for September 2022 — down slightly from 8.3% in August but still a stubbornly high result and above expectations. Core CPI increased by 6.6% year-over-year marking the highest gain since August 1982. Food and shelter were the main contributors to the increase in CPI, gasoline index fell slightly but overall energy prices are expected to rebound again. Used car prices are also not declining as much as expected. |

|

FISCAL POLICY |

NEUTRAL | Senator Manchin and Majority Leader Schumer reached an agreement on the latest tax and energy bill with incentives for green energy, electric cars, and conversely oil & gas companies for exploration. No changes in private equity taxes or higher tax rates for the very wealthy were enacted. The bill has been officially passed by the Senate. Last week, President Biden announced student loan forgiveness of up to $20,000 subject to income limitations. |

|

MONETARY POLICY |

NEGATIVE | With inflation still running hot, Fed Chairman Jay Powell is clear on his path to slow the economy enough to cool inflation. The Fed raised rates by 0.75% in September, bringing its target rate to 3.00-3.25%, and suggesting that additional 75bps rate hikes are likely in the coming months. The next Fed meeting will be taking place this week. |

|

GLOBAL CONSIDERATIONS |

||

|

GEOPOLITICAL RISKS |

NEGATIVE | Russia held controversial referendums for the annexation of four Ukrainian regions and the Russian Parliament unanimously recognized these regions as part of Russia. Ukraine and Western countries have condemned these actions by Russia by declaring them illegitimate and illegal. Additional sanctions are being imposed on Russia by many countries. |

|

ECONOMIC RISKS |

NEGATIVE | COVID-19 lockdowns in China are persistent and the ongoing Russian-Ukraine war is causing a major energy crisis in Europe. Putin shut down the pipeline that supplies Europe with natural gas indefinitely until all sanctions affecting Russia are lifted. Gas supplies from Russia to Europe have decreased by 88% over the past year and EU countries have agreed to cut gas usage by 15% as gas prices have more than doubled. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Quote of the Week

“Plans are nothing; Planning is everything.” -Dwight D. Eisenhower

“Your Financial Choices”

Tune in Wednesday, 6 PM for “Your Financial Choices” on WDIY 88.1FM. Laurie and her guest Attorney Pete Lorio from Fitzpatrick Lentz & Bubba discuss: Estate Planning Stories.

Questions can be submitted at yourfinancialchoices.com during or in advance of the live show. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.