February is National Cancer Prevention Month, which presents a wonderful opportunity to increase awareness and promote positive action toward living happier, healthier lives. Although cancer is still a leading cause of death, it’s essential to focus on the steps we can take to prevent cancer and improve our overall well-being.

Visit AACR for more information on cancer prevention.

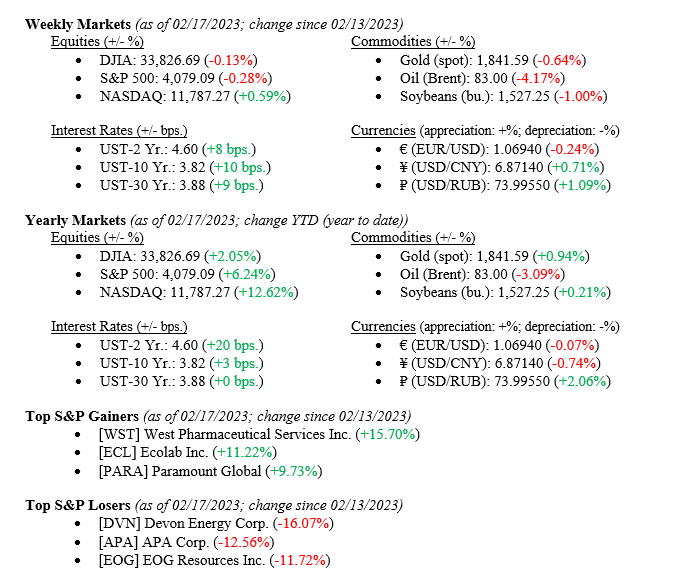

Equity market returns were mixed last week ahead of the President’s Day Holiday weekend, with the NASDAQ posting a modest gain of +0.59%. The S&P 500 Index moved lower by –0.28%, and the Dow Jones Industrial Average lost –0.28%. Mixed signals from the economy continue to foil investors and Wall Street Economists. Last week, we saw continued decreases in inflation indicators as measured by the U.S. Consumer Price Index and the U.S. Core Consumer Price Index. This tells the story the Fed is looking for: a slowing economy and inflation. However, behind that data release, the U.S. Retail Sales report (remember, ~70% of the U.S. Economy is consumer driven) came in higher-than-expected, hinting that the economy is still running at full steam. Overnight, economists moved over to our ongoing thesis here at VNFA, that a recession in 2023 is less likely.

US Economy

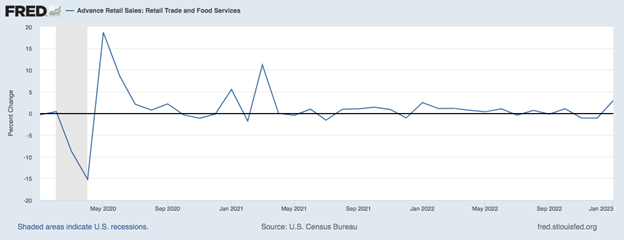

As mentioned above, last week showed us that the U.S. Economy continues to hum along nicely, with solid retail sales data proving that the consumer is not backing down and continues spending. Chart 1 below from the Federal Reserve Bank of St. Louis shows U.S. Retail Sales. Advanced Retail Sales (Trade & Services) increased by 3.0% in January 2023 versus a decline the prior month of –1.1%. This unexpected increase in consumer activity shows that not only is the U.S. Consumer remaining resilient, but they are also not concerned very much about the future economy to curtail their spending.

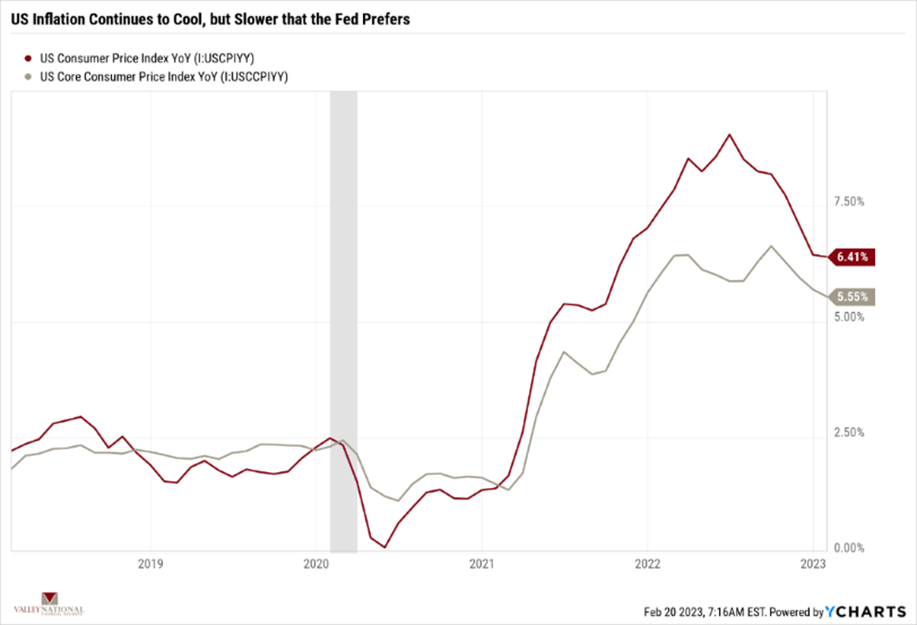

Chart 2 below from Valley National Financial Advisors and Y Charts shows U.S. Consumer Price Index and U.S. Core Consumer Price Index. As can be seen in Chart 1, inflation continues to cool as it had been doing since the 9% peak rate in June 2022. However, the pace of the slowing is what concerns the Fed. Fed Chairman Jay Powell would like to see inflation hit its target rate of 2%, as we all would, but it is taking longer, and more rate hikes will be needed. Futures markets are now pricing in a 50% chance of a June rate hike of +0.25%, which would be on top of +0.25% rate hikes at the March and May 2023 FOMC (Federal Open Market Committee) meetings. While concerning to us that further rate hikes are needed, we also believe that the economy continues to be strong enough to sustain higher interest rates and still grow at a modest pace, and the markets all seem to agree.

Policy and Politics

The Great China “Re-opening” of 2023 gives foreign markets reasons to hope that a pent-up, Covid-lockdown, Chinese consumer is about to unleash their spending on the global economy and fuel a solid rebound in economic activity. The Russia / Ukraine War rages on with neither side capitulating. U.S. President Biden’s surprise visit to Ukraine on February 20 pointed to symbolic support from the U.S., and a $500 million check from the U.S. offered real support. As spring comes into focus, the war could hurt global food supplies (Ukraine) and fertilizer (Russia). Lastly, instability in South America with regional democratic powerhouses such as Argentina always offers us a little worry and uncertainty.

What to Watch

Tuesday, February 21st

Existing Home Sales at 10:00 AM (Prior: 4.02M)

Existing Home Sales MoM (Month Over Month) at 10:00 AM (Prior: -1.47%)

Retail Gas Price at 4:30 PM (Prior: $3.502/gal.)

Thursday, February 23rd

Real GDP (Gross Domestic Product) QoQ at 8:30 AM (Prior: 2.90%)

Total Vehicle Sales at 10:30 AM (Prior: 16.20M)

30 Year Mortgage Rate at 12:00 PM (Prior: 6.32%)

Friday, February 24th

Core PCE Price Index YoY at 8:30 AM (Prior: 4.42%)

PCE Price Index YoY at 8:30 AM (Prior: 5.02%)

Personal Income MoM at 8:30 AM (Prior: 0.22%)

Personal Spending MoM at 8:30 AM (Prior: -0.23%)

Index of Consumer Sentiment at 10:00 AM (Prior: 66.40)

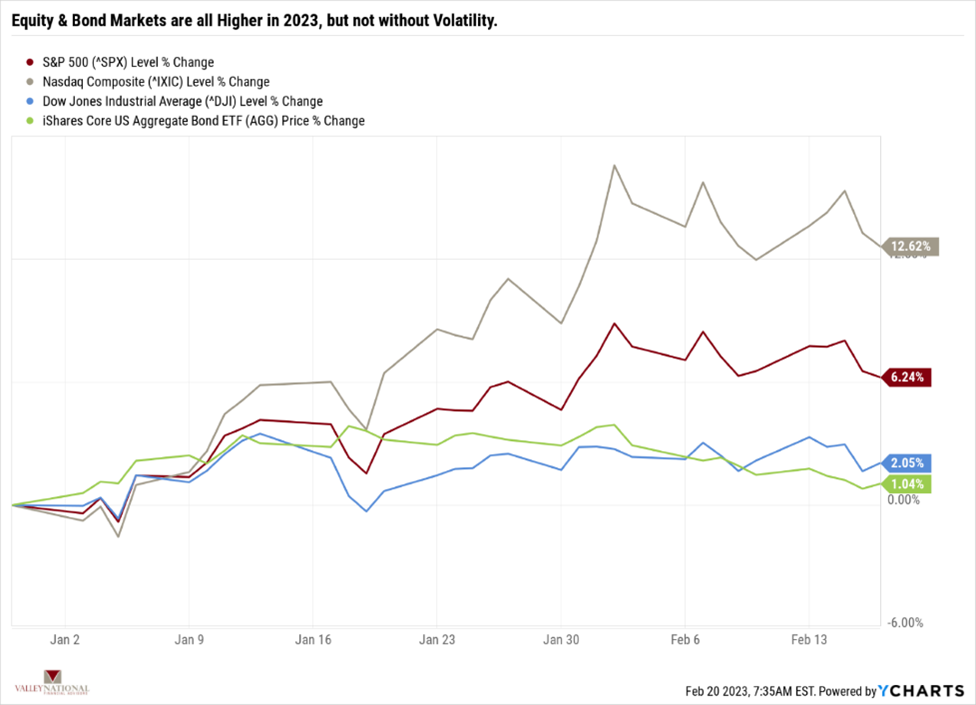

The Federal Reserve and Chairman Powell are on a mission to combat inflation with a target of 2%. Chart 2 above shows the progress the Fed has made thus far. A slowing pace in this regard simply puts more rate hikes on the horizon. Solid labor growth, falling unemployment, increasing consumer activity, and corporate “belt-tightening” show us that the U.S. economy remains healthy and will power through the current rate-hiking cycle. Further, a brief look at the equity and bond markets year-to-date shows that they are living up to their function as wonderful future economic indicators. Chart 3 below from Valley National Financial Advisors shows all three major equity market indicators and the iShares Core U.S. AGG Bond ETF. Year-to-date, each indicator is modestly higher, with the tech-heavy NASDAQ topping them all at +12.6%.

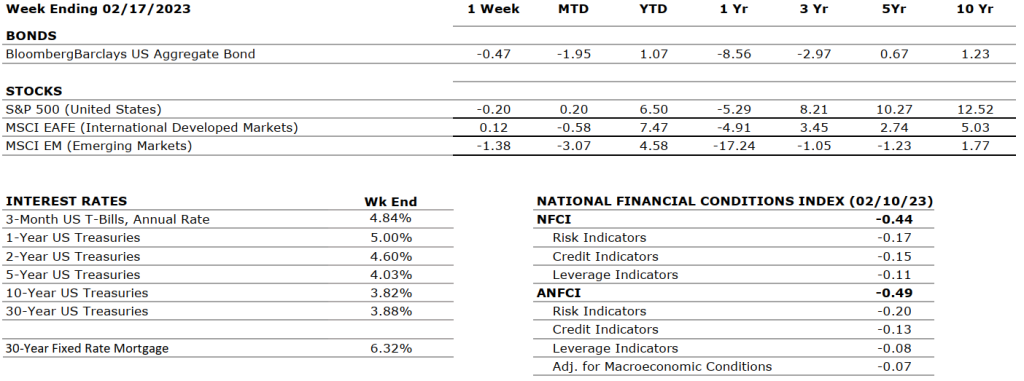

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Real gross domestic product (GDP) increased at an annual rate of 2.9 percent in the fourth quarter of 2022 after increasing by 3.2 percent in the third quarter. The increase in the fourth quarter primarily reflected increases in inventory investment and consumer spending that were partly offset by a decrease in housing investment.

CORPORATE EARNINGS

NEUTRAL

The earnings growth rate for Q3 2022 was 2.4%. For Q4 2022, earnings are expected to decline by -4.7%, up from the previous estimate of -4.9%. This would be the first negative growth since Q3 2020 (-5.7%). So far, 82% of S&P 500 companies have reported actual results — 68% of companies beat EPS estimates and 65% beat revenue expectations.

EMPLOYMENT

POSITIVE

U.S. Nonfarm Payrolls for January 2023 increased by 517,000, almost three times the expected number of 187,000. The unemployment rate fell to 3.4% from 3.5% and is now the lowest in 50 years. Leisure and hospitality, health care, professional services, and government were among the sectors with the most notable gains.

INFLATION

NEGATIVE

The annual inflation rate in the U.S. increased by 6.4% for January 2023 compared to the December 2022 reading of 6.5%. This is the lowest CPI value since October 2021. Core CPI increased to 5.6% versus 5.7% in December. The primary contributors to the increase in inflation were shelter, food, gasoline, and natural gas. On the other hand, indexes for used vehicles, medical care, and airline fares decreased over the month.

FISCAL POLICY

NEUTRAL

A few weeks after taking control of the chamber, GOP lawmakers are pushing for austerity measures in hopes of improving the nation’s fiscal health. Democrats have responded with harsh criticism and stressed that they would not negotiate a deal with Republicans involving reductions of benefits. Meanwhile, the latest CBO projections show that rising interest rates and spending bills are adding to deficits as the U.S. is on track to add $19 trillion of new debt over the next decade.

MONETARY POLICY

NEGATIVE

Earlier this month, the Fed approved a 25-bps rate hike taking its target range to 4.50%-4.75%. Although the magnitude of rate hikes has been decreased, rates are likely to be kept higher through 2023 with no reductions until 2024. The FOMC has also reiterated its strong commitment to return inflation to its 2% objective.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

While the Russian-Ukraine conflict does not show signs of abating, additional geopolitical issues have arisen in South America with the violent protests that hit the capital of Brazil. Following the October 2022 elections won by the left party, Jair Bolsonaro’s far-right supporters stormed Brasilia accusing the winning candidate and party of corruption. Bolsonaro is currently in Florida and has communicated little publicly.

ECONOMIC RISKS

NEUTRAL

Although the afore-mentioned geopolitical risks remain prevalent in everyday news, their effects on the global economy seem to have subsided. China abandoned its zero-Covid policy, which will positively impact the supply chain and the economy as a whole. The European economy also appears to be healthier than expected, partly due to an unusually warm winter that has provided some relief on increasing energy prices.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.