Questions can be submitted at yourfinancialchoices.com in advance of the live show. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

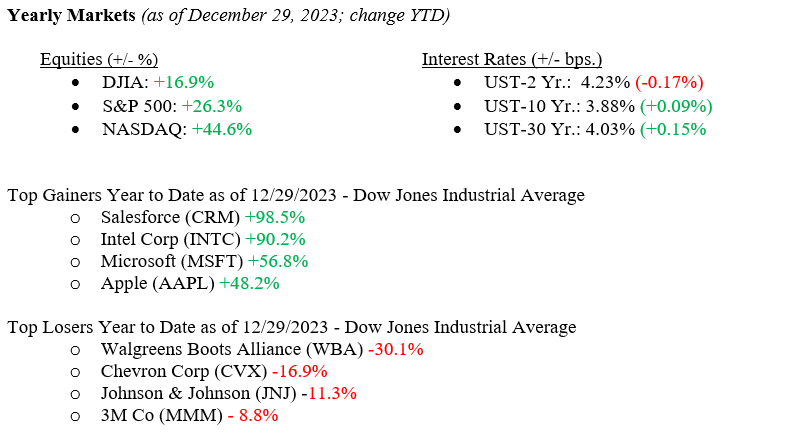

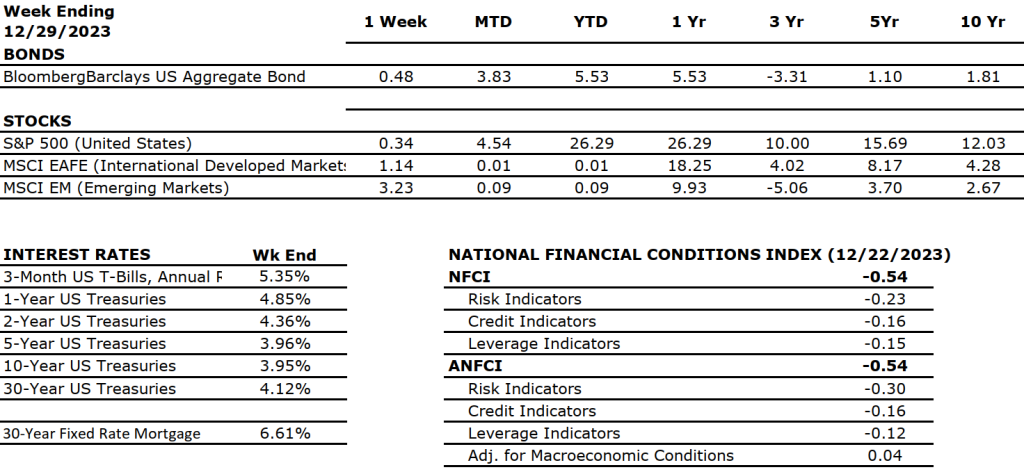

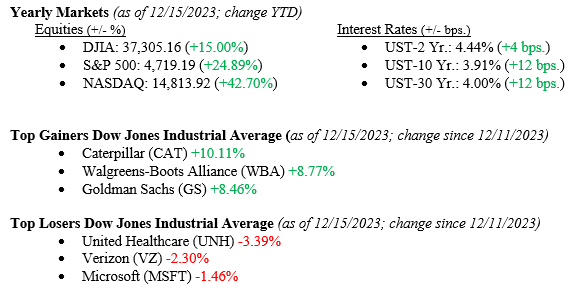

Equity markets proved resilient for one week and ended the year on a positive note for the week and year. The Dow Jones Industrial Average notched higher by +0.80%, the S&P 500 Index moved higher by +0.49%, and the NASDAQ moved higher by +0.32%. This was the ninth positive week for major stock indexes in 2023 and wrapped up a banner year overall for markets (see year-to-date figures immediately below). Another important data point is that 2023 marked the fourth positive year of the previous five years for the broadly followed S&P 500 Index, with only 2022 showing negative results. Also, important to note for 2023 was the positive impact on the bond market. The Bloomberg U.S. Aggregate Index (a widely followed barometer for the bond market) returned +5.53% for 2023, giving those investors counting on fixed-income returns a welcomed result.

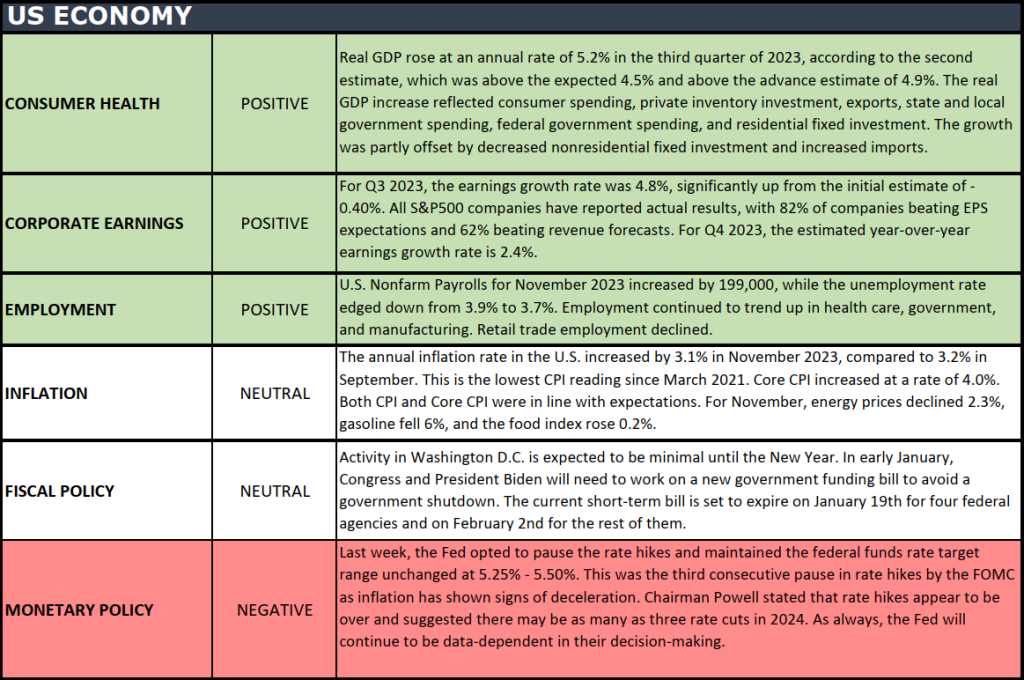

U.S. Economy

As we mentioned each week last year, the U.S. Consumer remained resilient and carried the U.S. Economy for much of the year. We saw strong annual spending in travel & leisure and overall retail spending. Early reports for the 2023 holiday season show retail sales growing by +3.1% and online shopping rose by +6.3%. While these numbers were lower than in 2022, they still show robust consumer spending.

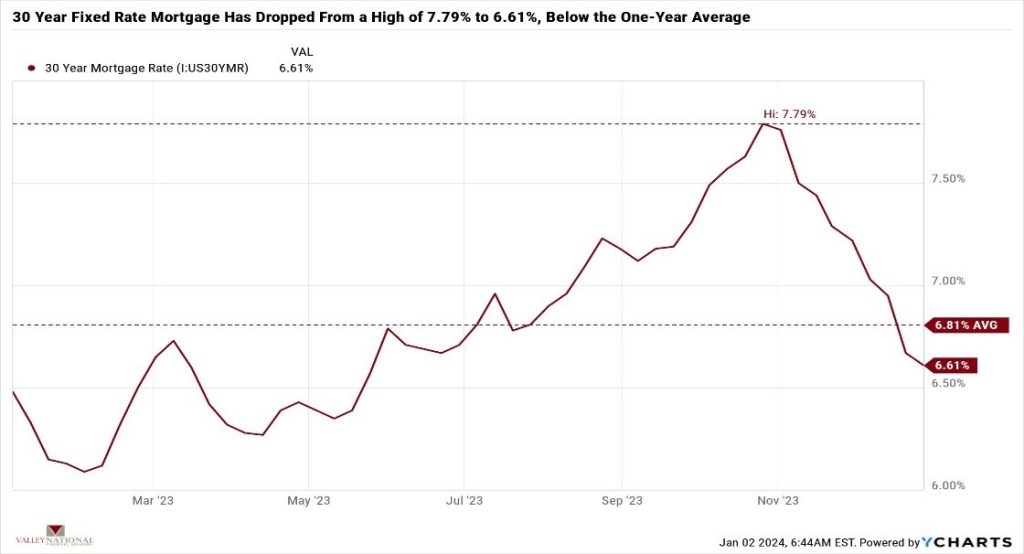

Financial markets are already pricing in rate cuts by the Fed for 2024. One area where we are seeing moving in rates is mortgage rates, which have fallen from recent highs near 7.80% to 6.61% before any actual cuts in rates by the Fed. See Chart 1 from Valley National Financial Advisors and Y Charts showing the 30-year mortgage rate over the past year. As mortgage rates fall, the housing industry will get a boost as affordability for new or existing homes will increase for all consumers.

Policy and Politics

Legislators and policymakers do not return to Washington, DC, until next week. Top on their agenda will be working out a funding agreement for the U.S. Government. The current funding agreement ends on January 19, and a new budget is needed to avoid a partial government shutdown. With 2024 being a major election year, we expect lawmakers to avoid looking any worse than they already do and, therefore, avoid embarrassing events like government shutdowns. Super Tuesday (the day when the greatest number of U.S. states hold presidential primary elections) is just 63 days away!

What to Watch

U.S. Initial Claims for Unemployment Insurance for week of Dec 30, 2023, released 1/4/24.

30-year Mortgage Rate for week of Jan 4, 2024, released 1/4/24, prior 6.61%

U.S. Unemployment Rate for Dec 2023, released 1/5/24, prior 3.70%

U.S. Labor Force Participation Rate for Dec 2023, released 1/5/23, prior 62.80%

U.S. Non-farm Payrolls MoM for Dec 2023, released 1/5/24, prior 199,000.

U.S. Recession Probability for Dec 2024, released 1/5/24, prior 51.8%

While it may be fitting for readers of The Weekly Commentary to take a victory lap after 2023’s stellar returns for stock and bond markets, we would rather readers continue to follow the data. All year in 2023, we followed the data – watching the consumer, understanding the housing market, reading employment numbers, and understanding that if Americans are working – they are spending, and consumption is critical to the U.S. economy. Long-term investors were rewarded in 2023 for sticking to their plan and understanding that consistency and patience are the key to investing and gathering long-term wealth. Wall Street prognosticators and economists waited for a recession in 2023 that never arrived. Meanwhile, cautious optimism prevailed simply by following the data. 2024 is just starting, but our advice remains the same, stay invested, stay focused, and follow the data. Happy New Year.

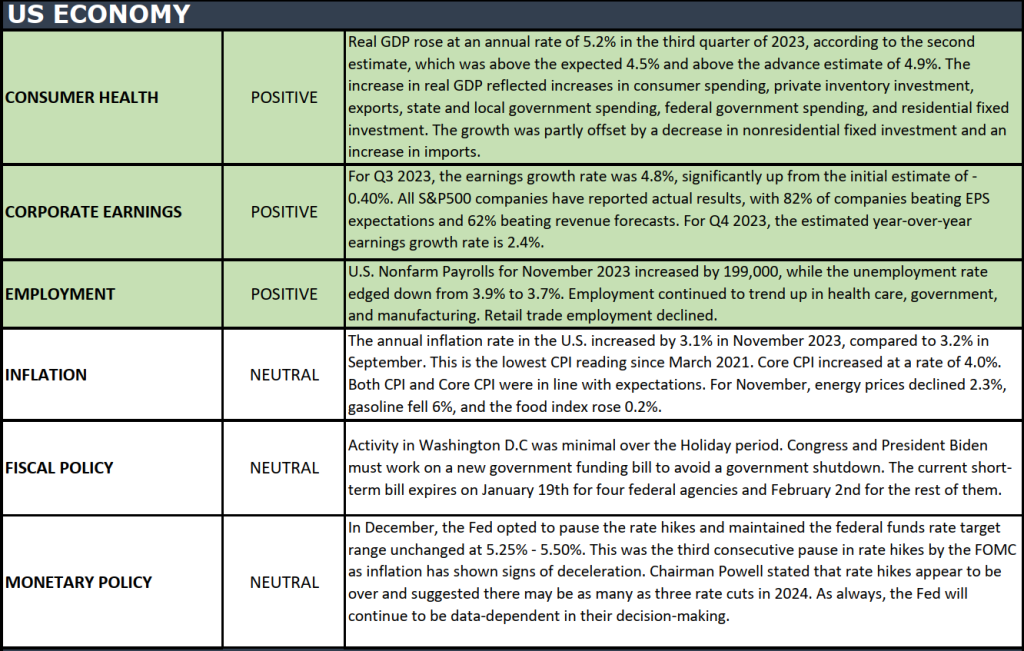

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Questions can be submitted at yourfinancialchoices.com in advance of the live show. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

If it were not so close to Christmas, we would suggest we put a red stocking cap on Fed Chairman Powell and call him “Santa Claus,” given the Santa Rally we have had over the last seven weeks. Last week, we added another 3.0% to the major stock market indexes, bringing each well into double-digit territory on a year-to-date basis (see figures immediately below.) Of course, I am referencing Chairman Powell’s press conference last week after the FOMC (Federal Open Market Committee) meeting, where he reaffirmed the notion that inflation does not need to reach 2.00% for the Fed to start cutting rates. This comment gave the markets all they needed to prepare for lower rates in 2024. This will help all major market indexes, especially small capitalization stocks that rely heavily on borrowing for standard business activities. Further, in a stunning move lower, the 10-year US Treasury dropped 32 basis points on the same news to close the week at 3.91%.

U.S. Economy

As mentioned above, the FOMC kept interest rates unchanged for the third meeting in a row, signaling the long-awaited “Fed Pivot,” meaning monetary policy moves from a tightening stance (increasing interest rates) to an accommodating stance (lowering interest rates). The Fed Funds Futures markets are pricing in rate cuts as soon as March 2024, yet the FOMC members do not see rate cuts until September 2024. Our moves in 2023 were all based on the data, particularly our call for “no recession in 2023.” We will continue to follow the data as we assess the true path of rate cuts in 2024. All parts of the U.S. economy continue to point to growth and expansion, at least into early 2024. Our thoughts are that the Fed will watch the data as well.

Policy and Politics

While Washington, DC, is closed for the holidays, we are looking to January 2024, when budget talks will need to start quickly to avoid the risk of a government shutdown. Next year remains a presidential election year, so we also expect minimal disruption from Washington so President Biden can point to the healthy U.S. economy while campaigning for reelection.

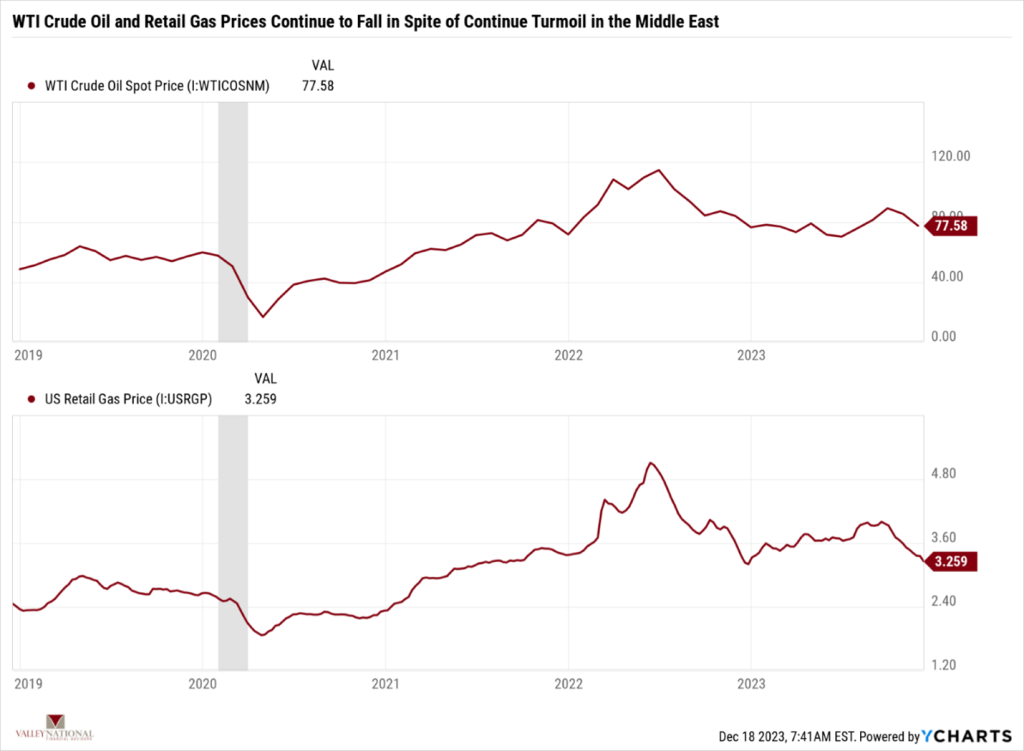

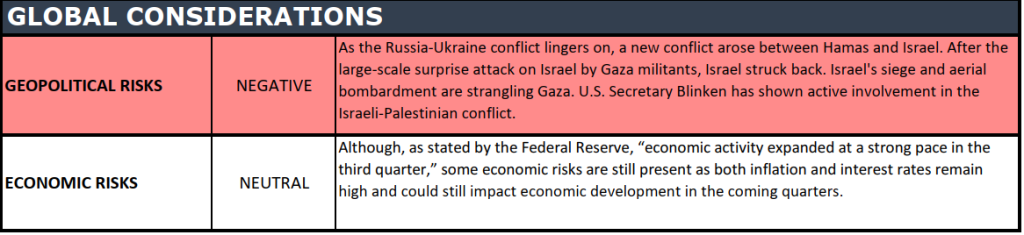

Globally, we are ramping up our concerns about the Israel/Hamas War and the risks of it spreading beyond the localized region. Rockets flying between Israel and Hezbollah in Lebanon and Yemeni militants seizing shipping tankers in the Red Sea have caused enough chaos that shipping firms, including Maersk and B.P., have either paused or re-routed container and oil tankers. While there is not yet a major military escalation, the disruption in shipping and supply chain management will cause problems in the global economy. Thus far, oil, a major commodity of the Middle East, has yet to react to the problems. See Chart 1 below from Valley National Financial Advisors and Y Charts showing WTI Crude Oil and Retail Gas Prices. Both continue to fall, with the U.S. Average retail price of gasoline hitting $3.26/gallon. Petroleum is a critical component of manufacturing and transportation and a key to keeping inflation at bay.

What to Watch

U.S. Real GDP (Gross Domestic Product) Quarter over Quarter for 3rd Quarter 2023, released 12/21/23, prior +5.20%

30 Year Mortgage Rate for week of December 21, 2023, released 12/21/23, prior 6.95%

U.S. Core PCE Price Index Year over Year for November 2023, released 12/22/23, prior 3.46%

U.S. Index of Consumer Sentiment for December 2023, released 12/22/23, prior 69.40.

Thus far, 2023 has rewarded the patient investor with solid gains across all major stock and bond market indexes. We have seen the economy defy all the so-called experts who predicted a recession in 2023 and instead continue to grow and expand at a healthy pace. Employment remains strong, with a national unemployment rate of 3.7%. The housing market has thrived, and 30-year fixed mortgage rates are below 7.00%. This week, we will see earnings from various companies, including Nike and Accenture. Earnings are important as they prove that companies are still making money and, therefore, employing workers. While we appreciate markets’ gains this year, we continue to watch events unfolding in the Middle East with concern. Higher interest rates are off the table, but the markets may be pricing in rate cuts sooner than reality will prove. There are seven trading days left in the year, and Santa is just a few days away. Happy Trading!

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Team VNFA is seeking a Director of Research & Investments, to work as part of our Investment Department. Read more about this opportunity: Director, Research & Investments