We are excited to introduce the new YourFinancialChoices.com website. The

updated site has the complete archive of the show’s 10+ years on WDIY 88.1FM so

you can listen any time.

The show is live on WDIY and wdiy.org on Wednesday

evenings from 6 p.m. to 7 p.m. During live shows, Laurie Siebert takes calls

with questions on any financial topic. She also accepts questions via the

website to address during the show.

by William Henderson, Vice President / Head of Investments Last week’s holiday-shortened trading week allowed markets to close the week with mixed results. The Dow Jones Industrial Average and the S&P 500 Index both show negative returns for the week at -0.34% and -0.52% respectively, while the NASDAQ closed in positive territory at +0.31%. Year-to-date, the Dow has returned +8.3%, the S&P 500 +16.7%, and the NASDAQ Composite +44.0%. 2020 continues to provide investors with strong returns across the broader markets despite historic headwinds.

President Trump signed the $900 billion COVID-19 Stimulus Bill

which eventually sends $600 to eligible Americans as part of the relief

package. This recent stimulus package coupled with the distribution of the

COVID-19 vaccine and a willing and able FED providing market liquidity

continues to fuel the strong economic recovery. These obvious tailwinds

will be present in 2021 as well, and many economists are now predicting a strong

GDP growth estimate for 2021. We talk more about this in our 2021 Outlook video

above.

Short trading days,

second-string trading desks and actions like tax lost harvesting and window

dressing by portfolio managers could move this week’s thinly traded markets

lower even in the face of positive news. At worst, results will be

confusing.

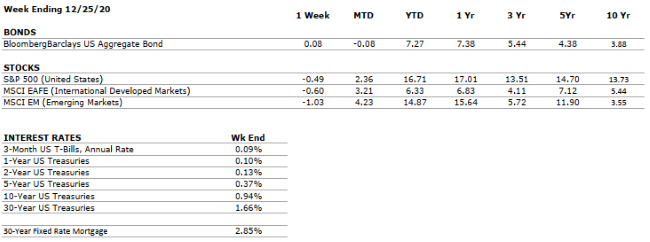

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

GDP increased at a 33.1% annualized pace in Q3. The U.S. economy has now recovered about 2/3 of its output lost to the COVID-19 pandemic.

CORPORATE EARNINGS

NEUTRAL

In Q3, S&P 500 earnings were down 7-8% from the year-ago period. This compares to Q2 2020, in which S&P 500 earnings were down by 1/3 from the comparable 2019 quarter.

EMPLOYMENT

NEGATIVE

In November, the unemployment rate declined to 6.7%. This continued the month-over-month improvements seen since April, when the metric was above 14%. However, the pace of hiring slowed greatly in November as COVID-19 cases surged.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

Congress passed its second major fiscal relief package of 2020, the most recent one amounting to $900 billion in stimulus. President Trump, after a minor delay, signed the Stimulus Bill into law.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

Although economic activity mostly remains below 2019’s levels, improvement has occurred across nearly every measure since the April nadir. With multiple vaccines in distribution, a second fiscal package in place, and interest rates low, 2021 is positioning to be a strong economic year.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, December 30, 6 PM for a recorded episode of “Your Financial Choices” on WDIY 88.1FM: Laurie will return live on air in the new year on January 6, 2021, at which time she will take your questions live on the air at 610-758-8810, or address those submitted prior via yourfinancialchoices.com.

VNFA Team Chat – Trending Topics (December 2020 – PART II) Financial Advisors

Laurie Siebert, CPA, CFP®, AEP® and Tim Roof, CFP®

discuss 2021 planning and the importance of asset rebalancing asset

allocations.

by William Henderson, Vice President / Head of Investments The so-called Santa Rally continued last week as all three major stock market indices turned in positive numbers for the week ended December 18, 2020. The Dow returned +0.4%, the Standard & Poor’s 500 Index returned +1.3%, and the NASDAQ returned +3.1%. Last week’s returns added to what is turning out to be a very strong year for market returns. Returns are also varied across indices proving the importance of a diversified, well-invested portfolio. Year-to-date, the Dow has returned +5.8%, the S&P 500 +14.8%, and the NASDAQ Composite +42.2%. These returns are quite stunning when we think of all that the year 2020 has thrown at the market. The stock market has digested and plowed through a major global pandemic, an economic disaster in the form of a double-digit world-wide recession, and a costly and divisive U.S. presidential election.

Thankfully, in response to the above economic headwinds, we have seen dramatic fiscal and monetary stimulus in the form of relief packages from the U.S. Congress as well as a Federal Reserve that reacted by moving interest rates to near zero and adding as much liquidity to the markets as needed. Beyond repairs to the economy, Operation Warp Speed has allowed the fast-tracking creation and release of a vaccine for COVID-19. Last week, the vaccine was delivered and administered across the United States and will continue to be quickly and widely administered across the nation. Further, the U.S. Congress finally reached an agreement on a $900 billion second stimulus package which includes $600 billion in direct payments to Americans, $300 billion in weekly supplemental unemployment insurance and additional funds for small business assistance.

To

be sure, there are headwinds in front of a continued economic recovery. In

the face of the release and distribution of COVID-19 vaccines, new cases and

hospitalizations across the United States reached all-time highs last week and

several states including, Pennsylvania, New York, and California imposed new or

additional lock down and travel restrictions. These headwinds are offset

by strong performance in the technology and consumer discretionary spending

sectors as working from home, becomes the norm rather than the exception. Working

from home requires a reliable internet connection with strong bandwidth, cloud

applications and virtual software capabilities supplied by companies like Zoom

and Microsoft. Consumers are also showing resilience in spending with

entertainment expenditures being replaced by food delivery options rather than

dining out, for example. Lastly, the Federal Reserve, following a recent

round of stress tests, will allow banks to engage in share buybacks in the

first quarter of 2021. Stringent rules remain in place for dividend payments

and other capital requirements but the lift on buybacks shows there is

significant improvement in bank capital cushions strengthened by record

earnings.

This

week is a Christmas Holiday shortened week, but much will be packed into the

trading periods as tailwinds and headwinds compete for directionality of the

economy and markets. Remain focused on the long-term outcome and a

diversified portfolio and let’s hope for a continued Santa Claus Rally into

2021.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

GDP increased at a 33.1% annualized pace in Q3. The U.S. economy has now recovered about 2/3 of its output lost to the Coronavirus pandemic.

CORPORATE EARNINGS

NEUTRAL

In Q3, S&P 500 earnings were down 7-8% from the year-ago period. This compares to Q2 2020, in which S&P 500 earnings were down by 1/3 from the comparable 2019 quarter.

EMPLOYMENT

NEGATIVE

In November, the unemployment rate declined to 6.7%. This continued the month-over-month improvements seen since April, when the metric was above 14%. However, the pace of hiring slowed greatly in November as coronavirus cases surged.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

Congress has passed a $900 billion stimulus package, following months of negotiation.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

Although economic activity mostly remains below 2019’s levels, improvement has occurred across nearly every measure since the April nadir. With a vaccine on the horizon, a fiscal package probable, and interest rates low, 2021 is positioning to be a strong economic year.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.