By: Chief Investment Officer, William Henderson

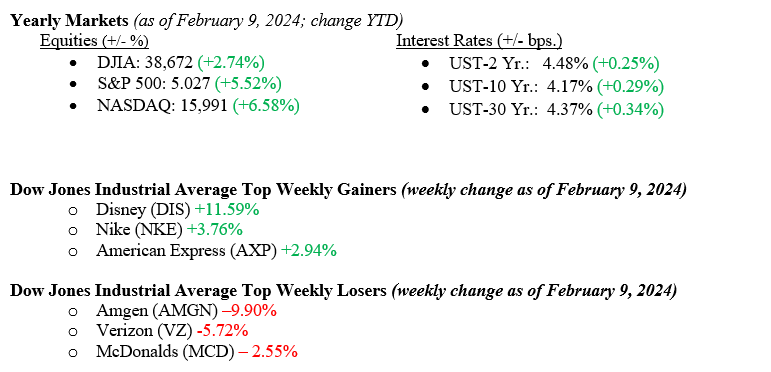

The verdict is still out on which city is happier at this point: Kansas City for clinching another Super Bowl victory or Wall Street for closing the S&P 500 Index over 5,000 for the first time in history. Given the historic volatility offered up by Wall Street, we would take the permanence of the Super Bowl victory. However, last week proved to be another winning week for the markets, with each major market index closing higher. The Dow Jones Industrial Average was barely higher by +0.04%, while the S&P 500 Index was +1.37% and the NASDAQ higher by +2.44%. Keeping with the Super Bowl theme here, equity markets seem much more content thinking about wins than losses, and the thoughts of a recession have now moved to the way back burner. Readers of The Weekly Commentary know we have believed in the strength of the US economy for well over a year now and still believe we are in a growth phase, albeit potentially trending downward, but slowly. Fixed income markets performed poorly last week, with the 10-year U.S. Treasury bond yield increasing by 14 basis points to 4.17%.

U.S. Economy

As mentioned above, the S&P 500 Index, widely understood to be a fair gauge of large capitalization stocks, closed above 5,000 for the first time in history. This is important because it truly shows the strength and resilience of the U.S. economy. See Chart 1 below from Valley National Financial Advisors and Y Charts showing the S&P 500 Index and the U.S. Gross Domestic Product since 1940. Market prognosticators and experts love to talk about the “Wall of Worry” or “the coming recession,” neither of which really matters over the long term, as you can see from the chart. The U.S. consumer, who continues to be gainfully employed, spends prolifically and churns out massive economic activity as a result. Our economy is consumer-driven, and overall, consumers are healthy, cash-rich, eager to spend, shop, and travel. If Punxsutawney Phil is correct and spring comes soon, we should continue to see healthy economic activity in the U.S.

Patrick Mahomes was the Super Bowl LVIII MVP, but the Wall Street MVP is the U.S. Consumer.

Policy and Politics

Washington seems content to flounder and argue rather than pass any meaningful legislation regarding the border crisis or additional aid to Ukraine or Israel. With the presidential election starting to take center stage, we believe Washington will be less likely to pass anything not directly tied to the important government funding bill coming in March. Meanwhile, Fed Chairman Jay Powell is marching to his own drum chorus and staying put on rate cuts at least through March 2024. All the main Fed speakers that were out last week parroted Chairman Powell’s message: “We need to see inflation come down a bit more to make sure we are not cutting rates too soon.” This week, we will see important inflation data that will give the FOMC (Federal Open Market Committee) their sought-after data.

What to Watch This Week

- U.S. Core Consumer Price Index YoY for Jan ’24, released 2/13/24, prior 3.90%

- U.S. Inflation Rate for Jan ’24, release 2/13/24, prior 3.35%

- U.S. Job Openings Total Nonfarm for Jan ’24, release 2/14/24, prior 9.026M

- U.S. Core Producer Price Index YoY for Jan ’24, released 2/16/24, prior 1.76%

New records are reached every year whether in sports, industry, or Wall Street. We love to see records broken as much as the next person, but the real story is the one where investors stick to their long-term investment plan thereby building truly generational wealth. There are plenty of reasons to expect equity markets to grow this year but there are always risks. Risk drives returns, and the management of risk over prolonged periods increases returns. The goal of a true investor is to increase returns while managing and limiting risk. Reach out to your financial advisor at Valley National Financial Advisors for assistance.