Tune in Wednesday, 6 PM, “Your Financial Choices” on WDIY 88.1 FM. Laurie and special guest Daniel Banks, President of Silver Crest Insurance, will be discussing: Medicare Open Enrollment- Continued.

As we approach Veterans Day, we’d like to share some fascinating facts about this important holiday and offer some suggestions for how you can celebrate this memorable holiday.

Interesting Facts:

Veterans Day, originally known as Armistice Day, was established to commemorate the end of World War I in 1918.

In 1954, President Dwight D. Eisenhower signed a bill renaming it Veterans Day to honor veterans of all U.S. wars.

A moment of silence is observed at 11 a.m. on 11/11 to remember veterans.

The U.S. Department of Veterans Affairs hosts a National Veterans Day Poster Contest for students, featuring the winning design on Veterans Day materials.

Ways to Celebrate:

Visit a State Park or Museum.

Attend a Veterans Day Parade.

Join the nation in observing a moment of silence.

Consider volunteering your time at a local veterans’ organization.

Remember, the most important thing you can do on Veterans Day is to genuinely thank veterans for their service and sacrifice. It’s a day to honor and show respect to those who have defended our country and its values. For more information on Veterans Day, please visit the U.S. Department of Veterans Affairs.

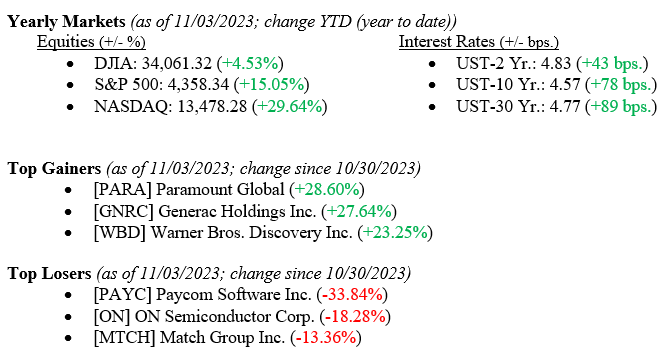

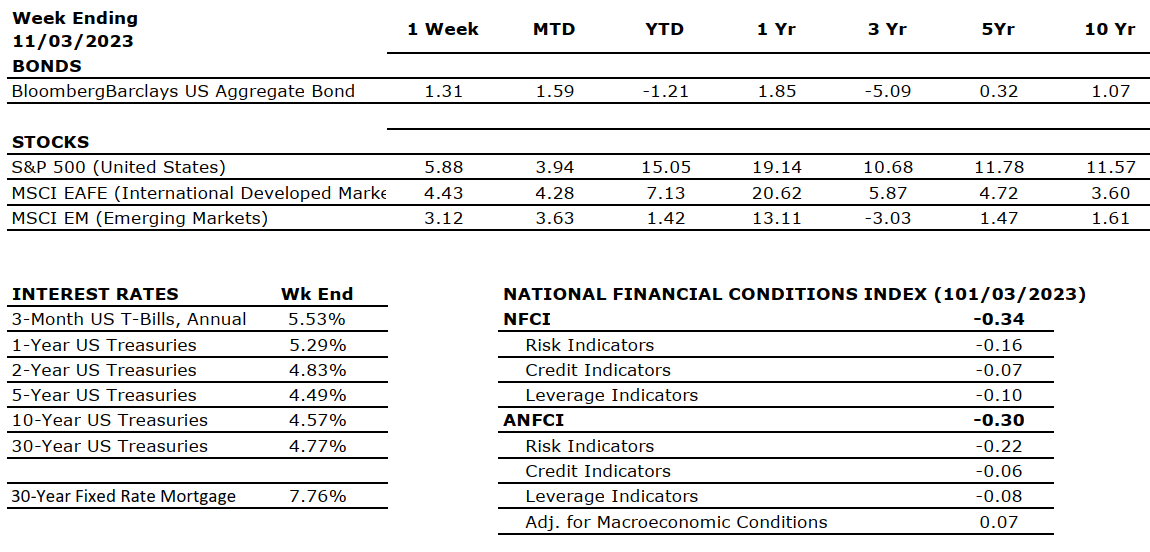

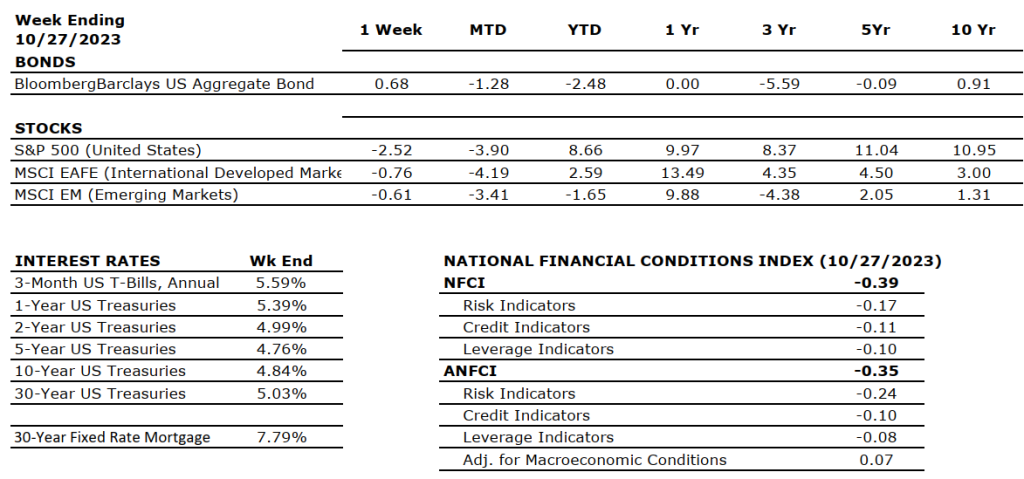

Oh, what a difference a week makes! Last week, you could read the financial press and see phrases like: “Sinking Stocks,” “Correction Territory,” and “The Bear Market is Here.” And then this week, we hear Fed Chairman Jay Powell repeat his previous month’s “We are going to listen to the data, but we are pausing rate hikes at this time.” Throw in a jobs number that showed hiring in the U.S. slowed a bit in September, and the stock market is off to the races with the largest one-week rally in 2023. See the weekly data below that shows each major market index returning 5%+ for the week, and even the oft-forgotten Russell 2000 Index of Small Cap stocks returned a positive +7.6%. Here at Valley National Financial Advisors, we have been cautiously optimistic all year by following the data and realizing there was too much good news and positive momentum to permit a recession in 2023. It seems the other economists, market prognosticators, and even the market itself have finally realized it, too. The 10-year U.S. Treasury closed the week at 4.57%, 27 basis points lower than the previous week.

Global Economy

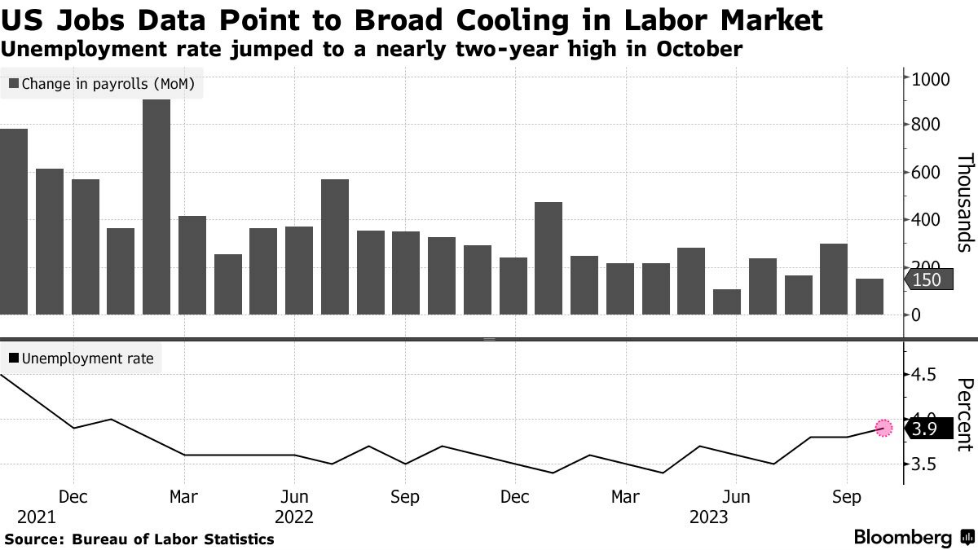

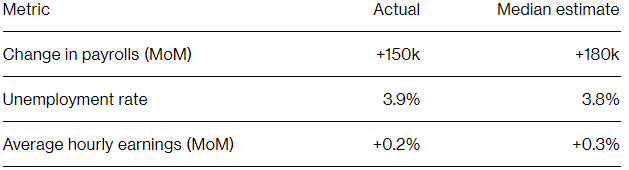

On Wednesday, the FOMC (Federal Open Market Committee) announced that it would be keeping rates at a 22-year high of 5.25-5.50% until at least their next meeting. However, economic data released on Friday surrounding nonfarm payrolls and unemployment suggest a cooling economy and that the Fed could be tightening in the near future. Nonfarm payrolls increased by 150,000 last month, less than expected, following a downwardly revised advance of 297,000 in September, according to the BLS (Bureau of Labor Statistics). Additionally, the unemployment rate climbed to 3.9% in October from 3.8% in September. Chart 1 below shows the last two years of month-over-month changes in payrolls and unemployment rate. Chart 2 shows actual data versus the median estimates.

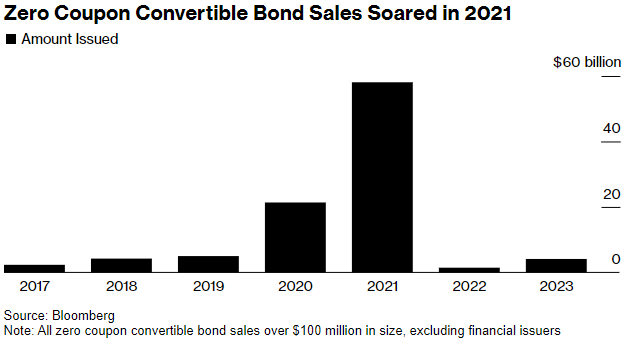

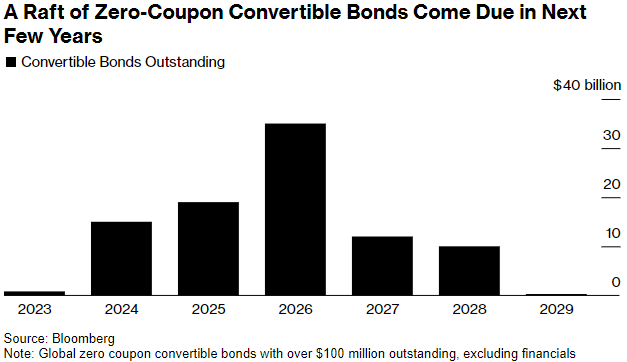

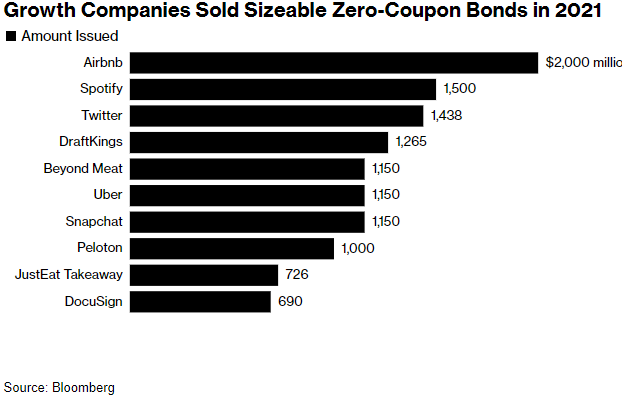

$69 billion of cheap and free debt issued during the pandemic is coming due within the next three years. During 2021, $58 billion of zero-coupon convertible bonds were issued, which was an increase of 1,100% over the two years prior. The need to refinance these bonds in a high-interest rate environment could pose a significant challenge to growth companies with low levels of cash generation. Chart 3 shows sales of zero-coupon convertible bonds since 2017. Chart 4 shows the maturation schedule of these debt obligations through 2029, and Chart 5 shows which companies had the largest issues.

8:30AM: Initial Claims for Unemployment Insurance (Prior: 217,000)

12:00PM: 30 Year Mortgage Rate (Prior: 7.76%)

Friday, November 10th

10:00AM: Index of Consumer Sentiment (Prior: 63.80)

Certainly, last week was a good week for stocks and bonds, as both rallied significantly. We know one week does not make a year, but the news from the labor department showing slowing job growth was well received by investors. Perhaps the Fed is done raising rates, but one more 0.25% rate hike will not matter as much in the grand scheme of things anyway, and we have seen the economy easily absorb 550 basis points of rate hikes. The movement in the 10-year US Treasury (see above) was impressive, and clearly, the big money has already moved in favor of lower interest rates from here. November tends to be one of the best months for equities (just behind April), and Wall Street loves a December Santa Claus Rally as traders scramble for year-end performance. We will remain cautiously optimistic and follow the data because data is not emotional, but investors are. Please reach out to your financial advisor at Valley National Financial Advisors for help or questions.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

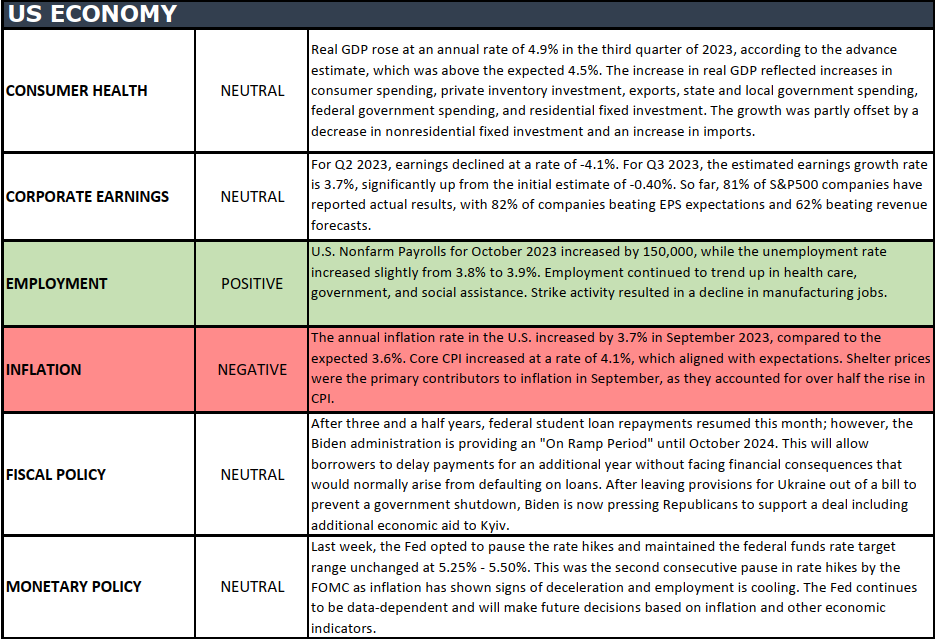

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM, “Your Financial Choices” on WDIY 88.1 FM. Laurie and special guest Stan Reinford, Loan Officer at Movement Mortgage, will be discussing: Mortgage Market Update and Stories to Share.

U.S. Equity markets were battered again last week across all sectors, even in the face of strong economic data released that showed 3rd quarter GDP rose +4.90%. Weak and mixed earnings reports and continued global turmoil weighed more heavily on the markets than a strong GDP report. For the week, the Dow Jones Industrial Average fell -2.1%, the S&P 500 Index dropped -2.5% and the NASDAQ fell -2.62%. Meanwhile, the 10-year U.S. Treasury bond yield fell nine basis points to close the week at 4.84% as several large investment houses either lifted their short trade on treasuries or recommended an outright buy for the sector. Both moves rallied bond prices.

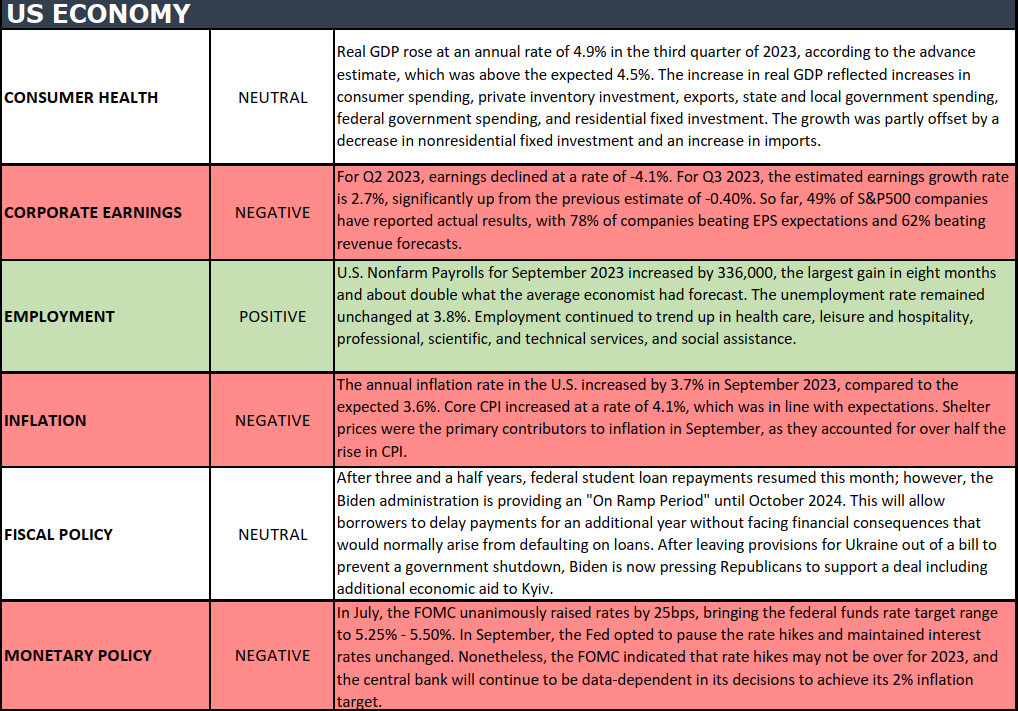

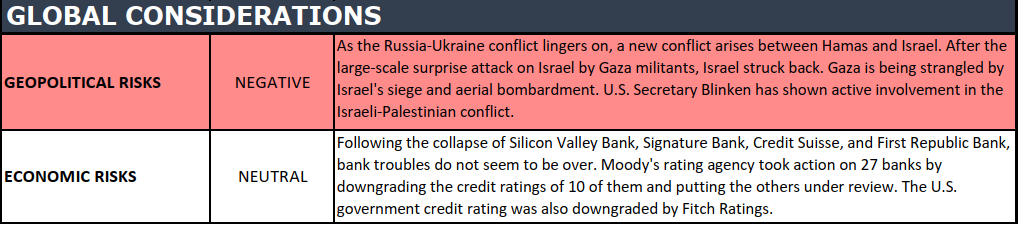

US Economy

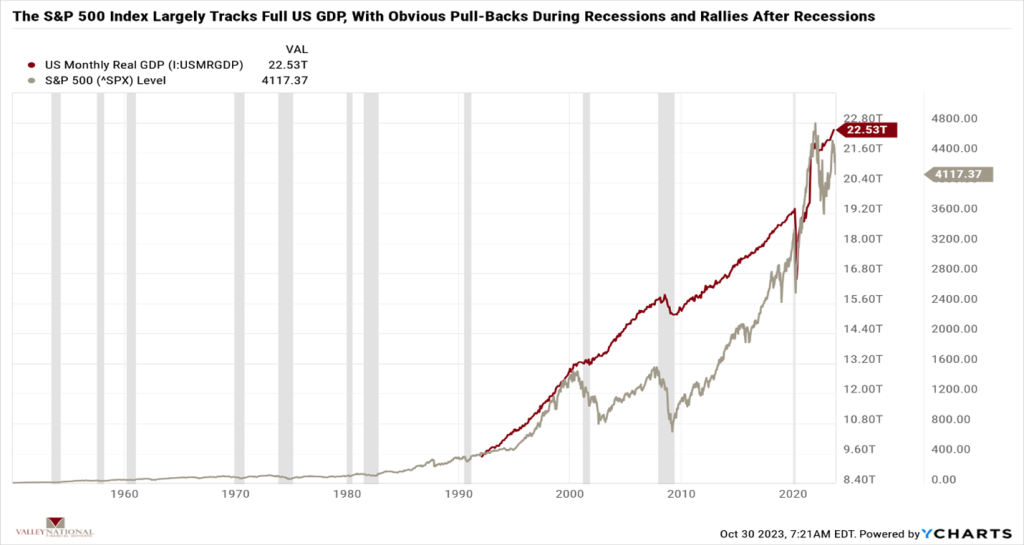

As mentioned above, the 3rd quarter U.S. GDP was released last week and showed that the U.S. economy grew by 4.90%, which was more than double the 2nd quarter rate and led by consumer spending on Travel & Leisure and Retail Goods & Services. The economy has been bolstered by a strong labor market and consumer savings accumulated during the pandemic. See Chart 1 below from Valley National Financial Advisors and Y Charts below showing the U.S. GDP and S&P 500 Index since 1950. We purposely picked an exceptionally long-dated chart to show why it is important to think about investing over extended periods rather than over very volatile short periods of time. You will see from the chart that, over time, the S&P 500 Index grows with the U.S. economy, and we continue to believe that the U.S. economy has a long way to go from here, especially over an extended period. Remember, time is an investor’s partner, not their enemy, and it is easy to get caught up in the volatile short-term noise and miss the big picture.

This week, we will look at the latest FOMC report after their two-day meeting ends on November first. Futures markets and traders are currently pricing in another “pause” in interest rate movements, which would be welcomed, but alone not enough to move markets higher. However, if that announcement is paired with a more dovish statement or language akin to “we believe the current interest rate levels are sufficient to combat inflation,” we could see the fear leave the markets to be replaced by positive investor sentiment.

Policy and Politics

Last week, we emphasized our concerns impacting markets: global regional turmoil, fear of the Fed continuing to raise interest rates and uncertainty related to our political spectrum. With the election of Congressman Mike Johnson (R-LA) as U.S. Speaker of the House, the political sideshow and uncertainly related to it has been lifted, and Washington (rightly or wrongly) can now get back to work with focus on a spending bill that avoids another embarrassing government shutdown.

What to Watch

Target Fed Funds Rate from the FOMC meeting, released 11/1/23; current upper limit 5.50%

U.S. Initial Claims for Unemployment Insurance for week of 10/28/23, released 11/2/23, prior 210,000 new claims.

U.S. Unemployment Rate for October 2023, released 11/3/23, prior rate 3.8%

Certainly, the economy continues to grow at a healthy pace despite interest rates rising from 0.00% to 5.50%. However, we are seeing sanguine earnings releases from companies and, along with that, language from CEOs and CFOs pointing to less-than-stellar earnings going forward. We stated before that interest rate hikes take time to work through the economy (typically 9-18 months). The first-rate hike in this cycle was in March 2022, about 18 months ago. We believe the FOMC is close to being finished with rate hikes as inflation continues to creep towards their 2% target (the September 2023 rate was 3.7%). As usual, watch for dovish (lower rates) or pivot (hike to cuts) language from Fed Chairman Jay Powell during the press conference after the FOMC meeting and announcement this Wednesday. We understand there is a lot of conflicting data: a growing economy, healthy consumer spending, strong labor market, less than stellar earnings, high-interest rates hurting the real estate market, and, of course, all equity markets continuing to sell off each week. Sometimes, it is not easy to be an investor. Please reach out to your financial advisor at Valley National Financial Advisors for questions or help.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.