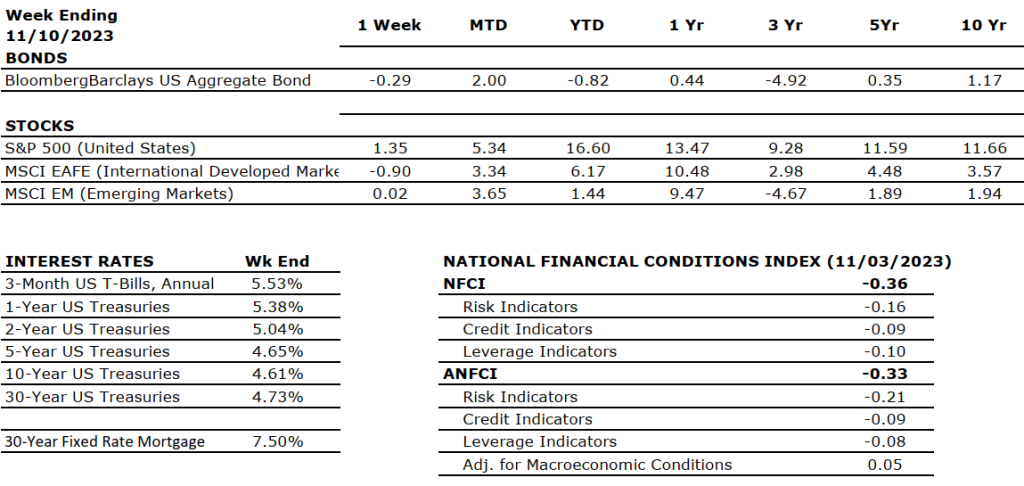

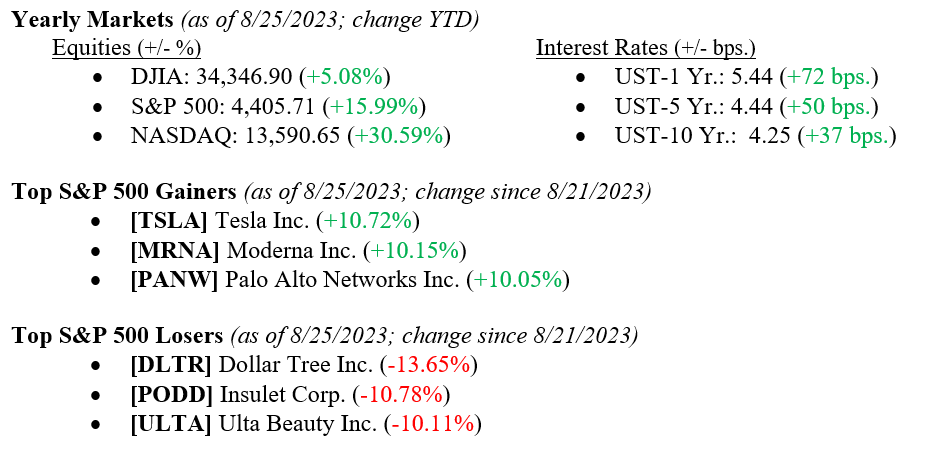

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

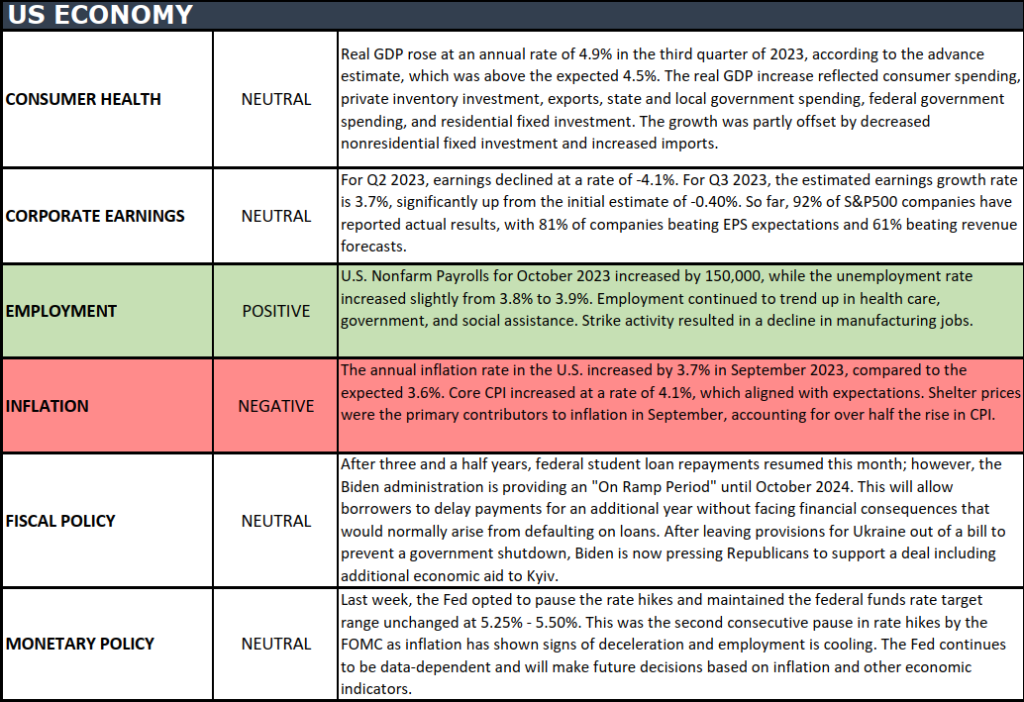

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Oh, what a difference a week makes! Last week, you could read the financial press and see phrases like: “Sinking Stocks,” “Correction Territory,” and “The Bear Market is Here.” And then this week, we hear Fed Chairman Jay Powell repeat his previous month’s “We are going to listen to the data, but we are pausing rate hikes at this time.” Throw in a jobs number that showed hiring in the U.S. slowed a bit in September, and the stock market is off to the races with the largest one-week rally in 2023. See the weekly data below that shows each major market index returning 5%+ for the week, and even the oft-forgotten Russell 2000 Index of Small Cap stocks returned a positive +7.6%. Here at Valley National Financial Advisors, we have been cautiously optimistic all year by following the data and realizing there was too much good news and positive momentum to permit a recession in 2023. It seems the other economists, market prognosticators, and even the market itself have finally realized it, too. The 10-year U.S. Treasury closed the week at 4.57%, 27 basis points lower than the previous week.

Global Economy

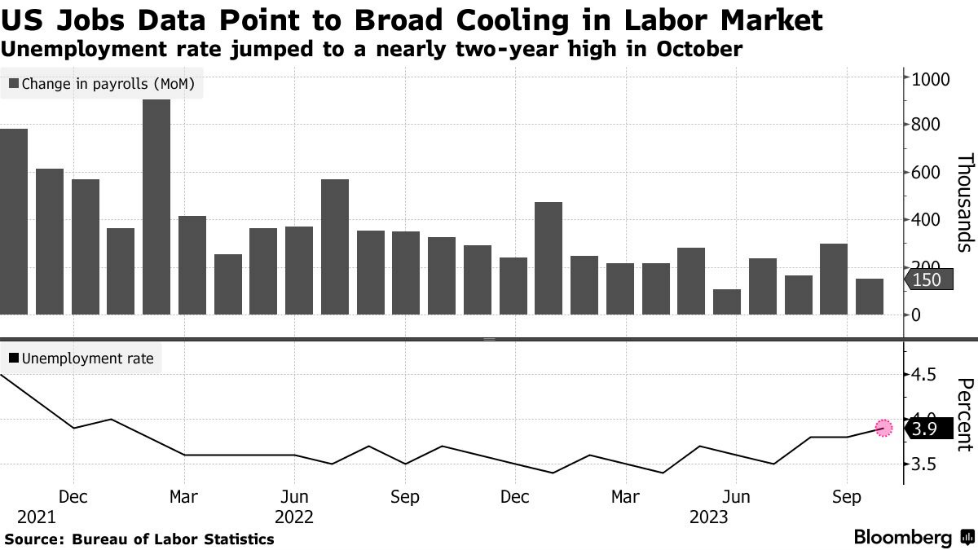

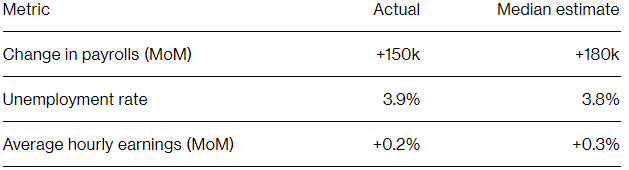

On Wednesday, the FOMC (Federal Open Market Committee) announced that it would be keeping rates at a 22-year high of 5.25-5.50% until at least their next meeting. However, economic data released on Friday surrounding nonfarm payrolls and unemployment suggest a cooling economy and that the Fed could be tightening in the near future. Nonfarm payrolls increased by 150,000 last month, less than expected, following a downwardly revised advance of 297,000 in September, according to the BLS (Bureau of Labor Statistics). Additionally, the unemployment rate climbed to 3.9% in October from 3.8% in September. Chart 1 below shows the last two years of month-over-month changes in payrolls and unemployment rate. Chart 2 shows actual data versus the median estimates.

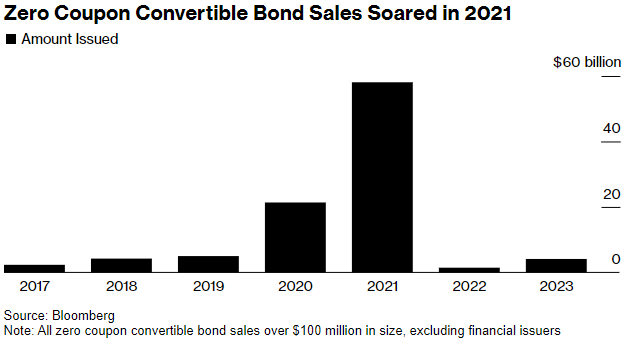

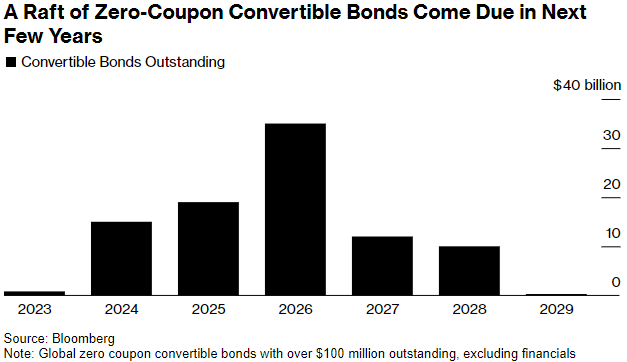

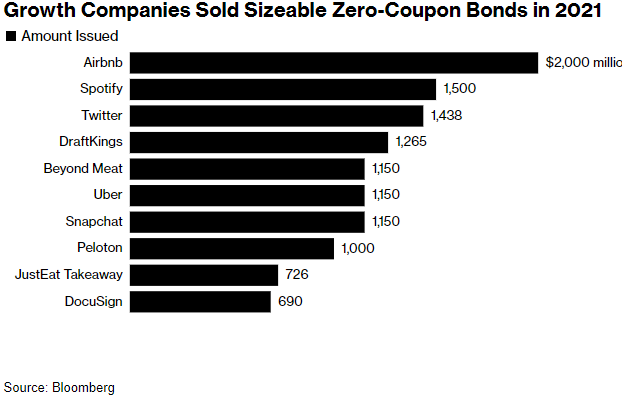

$69 billion of cheap and free debt issued during the pandemic is coming due within the next three years. During 2021, $58 billion of zero-coupon convertible bonds were issued, which was an increase of 1,100% over the two years prior. The need to refinance these bonds in a high-interest rate environment could pose a significant challenge to growth companies with low levels of cash generation. Chart 3 shows sales of zero-coupon convertible bonds since 2017. Chart 4 shows the maturation schedule of these debt obligations through 2029, and Chart 5 shows which companies had the largest issues.

8:30AM: Initial Claims for Unemployment Insurance (Prior: 217,000)

12:00PM: 30 Year Mortgage Rate (Prior: 7.76%)

Friday, November 10th

10:00AM: Index of Consumer Sentiment (Prior: 63.80)

Certainly, last week was a good week for stocks and bonds, as both rallied significantly. We know one week does not make a year, but the news from the labor department showing slowing job growth was well received by investors. Perhaps the Fed is done raising rates, but one more 0.25% rate hike will not matter as much in the grand scheme of things anyway, and we have seen the economy easily absorb 550 basis points of rate hikes. The movement in the 10-year US Treasury (see above) was impressive, and clearly, the big money has already moved in favor of lower interest rates from here. November tends to be one of the best months for equities (just behind April), and Wall Street loves a December Santa Claus Rally as traders scramble for year-end performance. We will remain cautiously optimistic and follow the data because data is not emotional, but investors are. Please reach out to your financial advisor at Valley National Financial Advisors for help or questions.

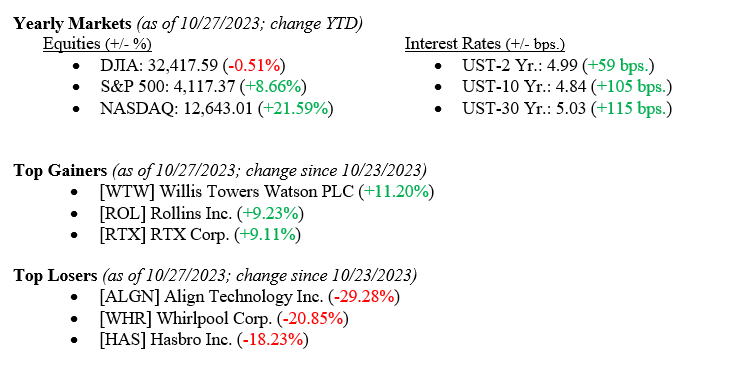

U.S. Equity markets were battered again last week across all sectors, even in the face of strong economic data released that showed 3rd quarter GDP rose +4.90%. Weak and mixed earnings reports and continued global turmoil weighed more heavily on the markets than a strong GDP report. For the week, the Dow Jones Industrial Average fell -2.1%, the S&P 500 Index dropped -2.5% and the NASDAQ fell -2.62%. Meanwhile, the 10-year U.S. Treasury bond yield fell nine basis points to close the week at 4.84% as several large investment houses either lifted their short trade on treasuries or recommended an outright buy for the sector. Both moves rallied bond prices.

US Economy

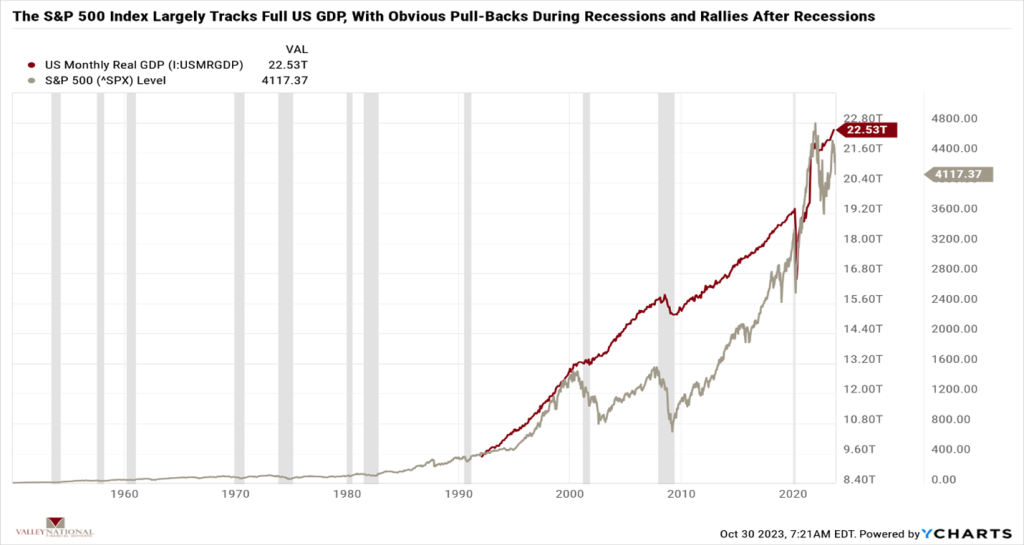

As mentioned above, the 3rd quarter U.S. GDP was released last week and showed that the U.S. economy grew by 4.90%, which was more than double the 2nd quarter rate and led by consumer spending on Travel & Leisure and Retail Goods & Services. The economy has been bolstered by a strong labor market and consumer savings accumulated during the pandemic. See Chart 1 below from Valley National Financial Advisors and Y Charts below showing the U.S. GDP and S&P 500 Index since 1950. We purposely picked an exceptionally long-dated chart to show why it is important to think about investing over extended periods rather than over very volatile short periods of time. You will see from the chart that, over time, the S&P 500 Index grows with the U.S. economy, and we continue to believe that the U.S. economy has a long way to go from here, especially over an extended period. Remember, time is an investor’s partner, not their enemy, and it is easy to get caught up in the volatile short-term noise and miss the big picture.

This week, we will look at the latest FOMC report after their two-day meeting ends on November first. Futures markets and traders are currently pricing in another “pause” in interest rate movements, which would be welcomed, but alone not enough to move markets higher. However, if that announcement is paired with a more dovish statement or language akin to “we believe the current interest rate levels are sufficient to combat inflation,” we could see the fear leave the markets to be replaced by positive investor sentiment.

Policy and Politics

Last week, we emphasized our concerns impacting markets: global regional turmoil, fear of the Fed continuing to raise interest rates and uncertainty related to our political spectrum. With the election of Congressman Mike Johnson (R-LA) as U.S. Speaker of the House, the political sideshow and uncertainly related to it has been lifted, and Washington (rightly or wrongly) can now get back to work with focus on a spending bill that avoids another embarrassing government shutdown.

What to Watch

Target Fed Funds Rate from the FOMC meeting, released 11/1/23; current upper limit 5.50%

U.S. Initial Claims for Unemployment Insurance for week of 10/28/23, released 11/2/23, prior 210,000 new claims.

U.S. Unemployment Rate for October 2023, released 11/3/23, prior rate 3.8%

Certainly, the economy continues to grow at a healthy pace despite interest rates rising from 0.00% to 5.50%. However, we are seeing sanguine earnings releases from companies and, along with that, language from CEOs and CFOs pointing to less-than-stellar earnings going forward. We stated before that interest rate hikes take time to work through the economy (typically 9-18 months). The first-rate hike in this cycle was in March 2022, about 18 months ago. We believe the FOMC is close to being finished with rate hikes as inflation continues to creep towards their 2% target (the September 2023 rate was 3.7%). As usual, watch for dovish (lower rates) or pivot (hike to cuts) language from Fed Chairman Jay Powell during the press conference after the FOMC meeting and announcement this Wednesday. We understand there is a lot of conflicting data: a growing economy, healthy consumer spending, strong labor market, less than stellar earnings, high-interest rates hurting the real estate market, and, of course, all equity markets continuing to sell off each week. Sometimes, it is not easy to be an investor. Please reach out to your financial advisor at Valley National Financial Advisors for questions or help.

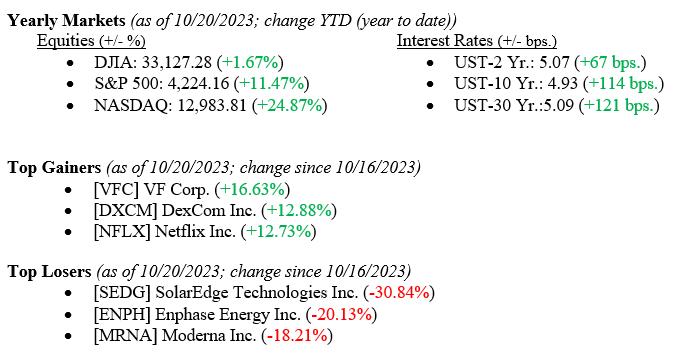

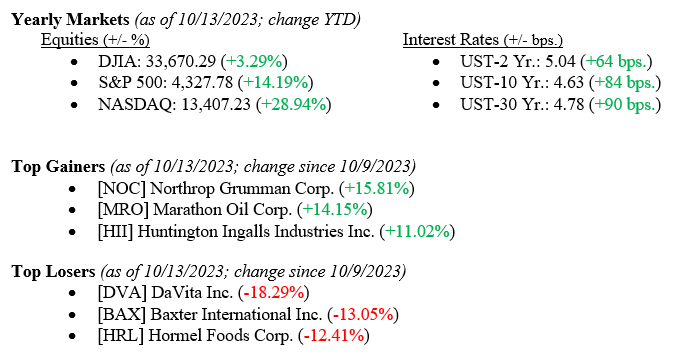

All three major market indexes posted heavy losses for the week, with the Dow Jones Industrial Average falling –1.6%, the broader S&P 500 Index falling –2.4%, and the tech-heavy NASDAQ falling –3.2%. A flurry of uninspiring earnings releases, higher bond yields, and continued global unrest led to the losses. Bond yields meanwhile moved higher, with the yield on the 10-year U.S. Treasury rising 15 basis points to close the week at 4.93%. Early reports this week show a 10-year Treasury yield moving to 5.00%, a level not seen since 2007. Two weeks ago, in this report, we introduced three words in our commentary that we do not take lightly. The words were turmoil, fear, and uncertainty. In this week’s report, we unpack those words and explain why we remain concerned.

Global Economy

The global economy is where turmoil firmly falls on the markets. The Israel/Hamas war continues without any view to a swift or less costly end to the conflict. The Middle East has rarely been a calm place, but relations have certainly been better than they are now among members of the region. For obvious reasons, oil markets and global trade rely on relative calm in the region – major oil producers are located here, and trade through the Suez Canal is a critical route for Asia/Europe trade. The Israel/Hamas War piles onto the Russia/Ukraine War and the China/Taiwan concerns. Hence, our use of the word turmoil – “a state of great disturbance or confusion.”

Policy and Politics

The second word we introduced is fear. Why fear? For the first time in many years, investors are fearing the Fed instead of welcoming the Fed and their concomitant market actions. Last week, in a speech to the Economic Club of NY, where we have two Valley National Group investment associates present, Fed Chairman Powell danced around the future path or direction of interest rates, pointing instead to the data as his compass for what the Fed will do next. Investors hoped to hear language stating that future rate hikes were off the table, but that was not the case in both fixed-income and equity markets sold off because everyone was still waiting for the classic Fed Put. The Fed Put happens when markets expect and price in lower interest rates, not higher ones. So, instead of welcoming Fed actions, markets fear future Fed actions. We believe that the economy remains healthy, which is most evident in the consumer who continues to spend. The labor market, where unemployment remains at a near-record low level of 3.8% and housing, while slower, continues to exhibit resilience.

What to Watch

Merger activity – there are two major M&A (merger & acquisition) deals on the table right now: Exxon/Pioneer Natural Resources and Chevron/Hess. These mega-billion-dollar mergers provide much needed fuel and profits to Wall Street where M&A and IPOs have been quiet recently.

U.S. Single Family Houses sold for September 2023, released 10/25/23, prior 675k.

U.S. Real GDP QoQ for 3rd Quarter 2023, released 10/26/23, prior +2.1%

U.S. Personal Consumption Expenditure Index YoY for September 2023, released 10/27/23, prior 3.48% (Fed’s favored inflation indicator)

U.S. Index of Consumer Sentiment for October 2023, released 10/27/23, prior level of 63.

We chose the summary for the week to discuss our third word – uncertainty. We have discussed markets hating uncertainty the most out of all worrisome trends. Typically, in a market where fear and turmoil exist, investors are uncertain, and their natural reaction is a flight to quality, which means buying U.S. Treasuries. However, U.S. Treasuries continue to sell off as the Federal Reserve’s surge in debt supply and mixed signals on the rate path weaken fixed-income markets. Furthermore, our leaders in Washington continue to do nothing as they wrangle to simply fill the U.S. Speaker of the House position, notably the third position in line for succession to the U.S. President.

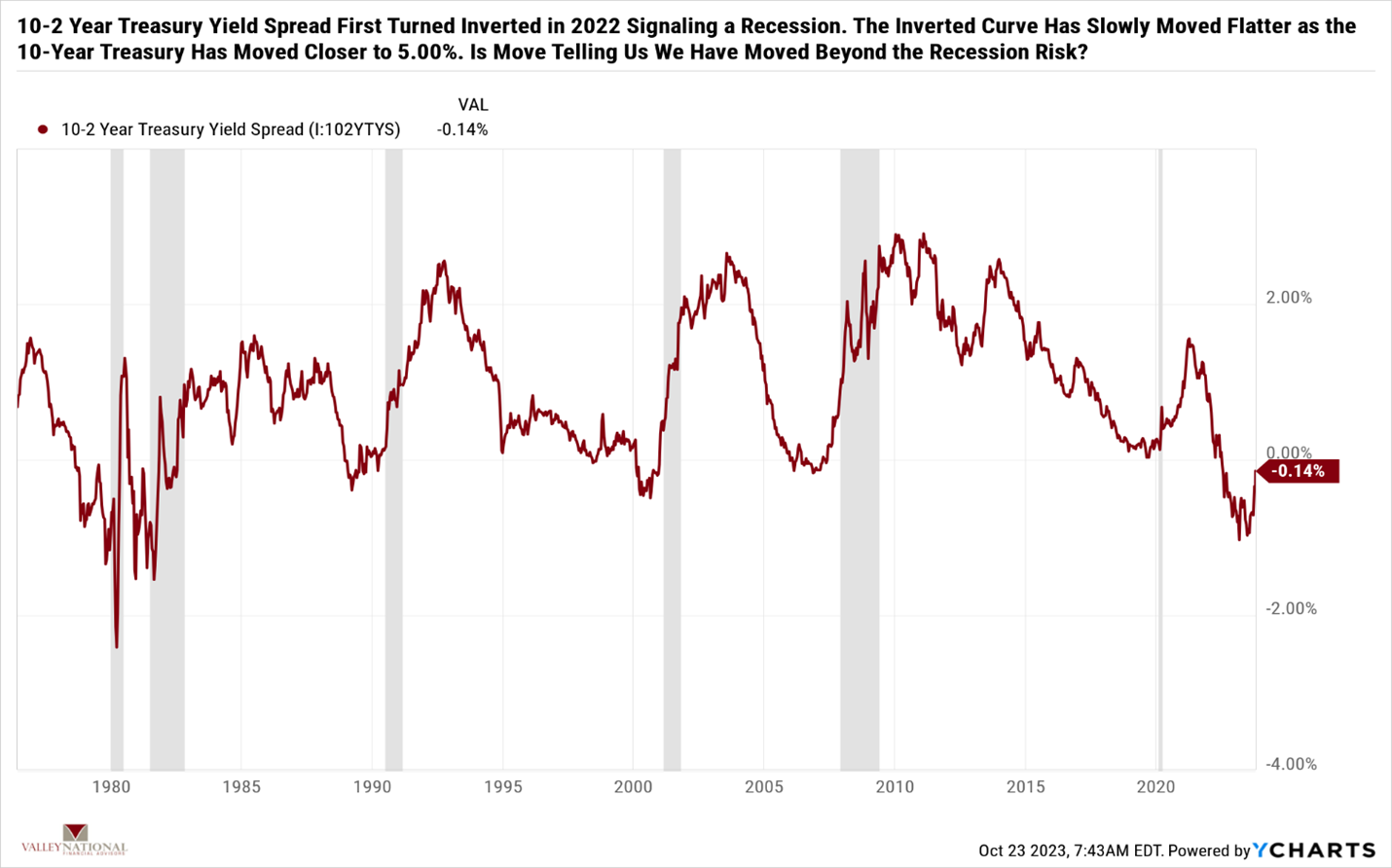

Uncertainty persists in our leaders, world politics, and the markets, so while it is not unusual for markets to sell off, it is unusual to see such a connected and broad sell-off in all markets in tandem. Treasuries at 5.00% offer investors real after inflation yields. See charts 1 & 2 above by Valley National & Y Charts showing first the U.S. Inflation rate and the 10-year U.S. Treasury yield and second the 10-2-year Treasury Yield Spread.

We expect to see turmoil, fear, and uncertainty in the market until each issue gets resolved over time, and time is always on the patient investors’ side. The patient investor can outlast uncertainty. Reach out to your advisor at Valley National Financial Advisors for advice or questions.

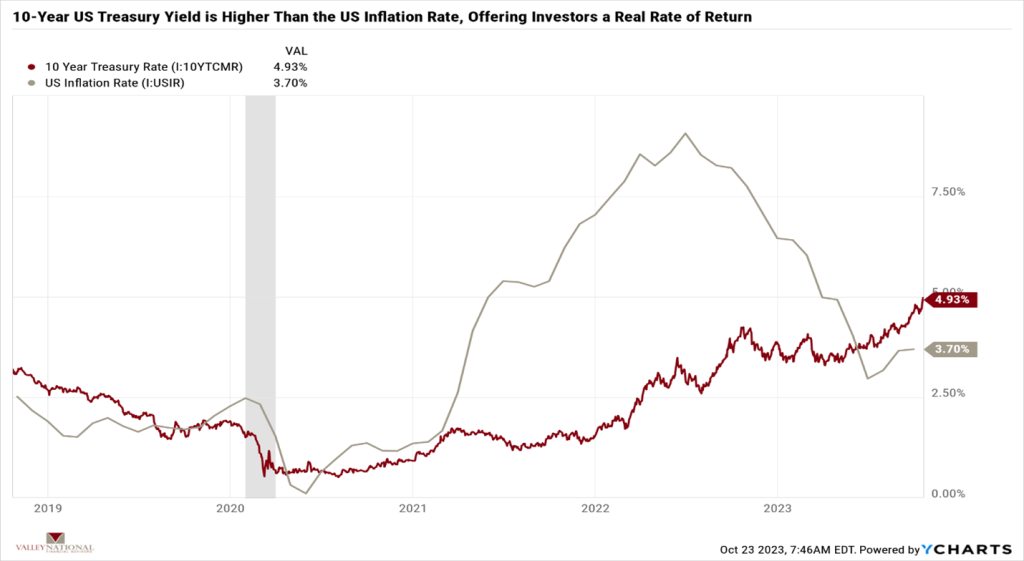

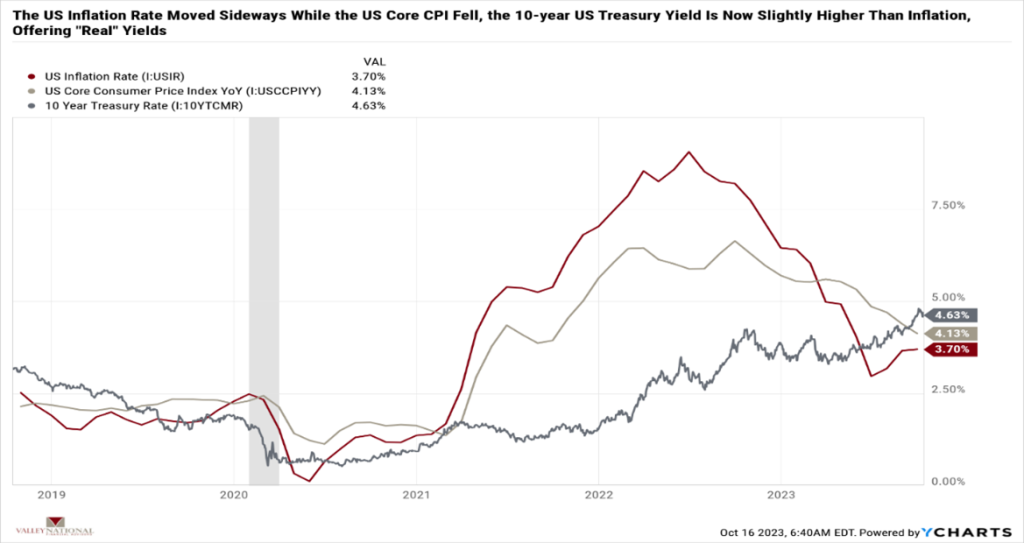

The broader markets rallied last week, seeing through the noise of continued inflation concerns, a protracted war in the Middle East, and mixed third-quarter corporate earnings releases. Last week, the Dow Jones Industrial Average and the S&P 500 Index moved +0.79% and +0.45%, respectively, while the NASDAQ moved lower by –0.18%. In a classic “Flight-to-Quality” trade, U.S. Treasury bond yields fell as investors moved to safe Treasuries during a time of global conflict. The 10-year U.S. Treasury bond fell 15 basis points, ending the week at 4.63%. Even at this lower yield, investors are finally seeing “real” yields on Treasuries as the U.S. Inflation Rate has finally fallen lower than the 10-year U.S. Treasury bond yield. See Chart 1 from Valley National Financial Advisors and Y Charts.

US Economy

As mentioned above, while stubbornly staying above the Fed’s target rate of 2%, the U.S. Inflation Rate is now 3.70% (released last week). The U.S. Core CPI (Consumer Price Index) fell to 4.13% in September 2023 from 4.39% in August 2023. Chart 1 below shows the 10-year U.S. Treasury and two inflation measures. While inflation remains higher, the yield on the 10-year Treasury is slightly higher, thereby finally offering investors real, after-inflation returns.

Higher interest rates continue to negatively impact growth stocks as those companies typically borrow money to expand operations or hire additional employees. As third-quarter earnings releases hit the tape, we will get a better picture of which firms and industries are best dealing with higher interest rates for longer. Large banks Citigroup, JP Morgan, and Wells Fargo all reported earnings better than expected as higher interest rates helped these banks as they continue to remain a bit stingy in passing on the higher rates to their depositors.

A widening or global escalation of the Israel-Palestinian conflict could impact oil prices, but thus far, world oil prices have not been materially impacted. It is important to watch this event to see how various actors on the world stage choose sides. For example, the U.S. has moved the USS Gerald Ford carrier fleet to the region to support Israel. Of course, defense stocks (ex. Northrop Grumman, General Dynamics & Lockheed Martin) have modestly rallied because of the growing conflict.

Policy and Politics

Three government forces are working in the economy right now, and all are impacting the markets, pushing uncertainty and worry into prices:

We have the Fed and its constant fight against inflation. Last week, Federal Reserve Bank Vice Chairman Philip Jefferson noted that higher long bond yields are doing a lot of the work for the Fed in slowing the economy, implying that there is no need for further rate hikes.

U.S. Secretary of State Anthony Blinken is actively involved in the Israeli-Palestinian conflict, which clearly indicates the U.S. is willing to do whatever is necessary to support our allies in the region.

We continue to see a circus in Washington, DC, as lawmakers fall over each other trying to elect a new U.S. Speaker of the House.

Taken together, these government forces are adding uncertainty and worry to the markets, which is quite the opposite of what we expect and desire from our leaders.

What to Watch

• U.S. Retail Gas Price for week of October 13, 2023, released 10/16/23, prior price $3.81/gallon. • U.S. Housing Starts for September 2023, released 10/18/23, prior 1.283 million starts. • U.S. Initial Claims for Unemployment for week of October 14, 2023, release 10/19/12, prior 209k • 30 Year Mortgage Rate as of October 19, 2023, released 10/19/23, prior 7.57% • Key Earnings releases to watch this week: Tesla, Netflix, Goldman Sachs, Lockheed Martin.

We pointed out the wall of worry above with confusion on interest rates, continuing global conflict, and a broken U.S. Congress. Meanwhile, the markets are moving slightly higher each week, and bonds finally offer “real” yields for investors. Instead of worrying about what is happening now, the markets are scaling the wall of worry and moving higher as they filter out the noise and see sectors like big tech, healthcare, and mega banks doing well, even given all the noise. It is easy to get mired down with worry and negativity – that is all we see on TV and hear from so-called experts, but the markets see the future and ignore the noise. Investors interested in creating long-term generational wealth should listen to the markets and ignore the TV. Reach out to your financial adviser at Valley National Financial Advisors for advice or questions.

The equity market ended the week mixed as a rally in tech stocks propelled the NASDAQ and S&P 500 Index higher but failed to pull along the broader Dow Jones Industrial Average. For the week, the Dow Jones ended down 0.45%, the S&P 500 up 0.82%, and the NASDAQ higher by 2.26%. The focus remained heavy on the Federal Reserve to see what monetary policy would come out of their Jackson Hole conference, and spoiler alert, Chairman Powell implied that rates would remain elevated until inflation approaches the 2% target and maintains that level. Across the pond, the Eurozone is struggling to combat inflation, which is still above 5%, suggesting the ECB may have to be more aggressive in its policymaking. Finally, the effects of China’s post-pandemic slowdown are beginning to be felt by trade partners and are causing a net detraction in global growth.

Global Economy

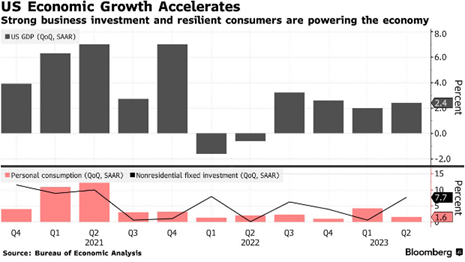

Federal Reserve policymakers met last week in Jackson Hole for their annual conference, focusing on monetary policy. Fed Chair Jerome Powell said that the central bank is ready and willing to continue raising rates if inflation does not sustainably trend down towards its 2% target. U.S. inflation printed last month at 3.18%, while it peaked last August 2022 at 9.1%. Remember that the Federal Reserve raised rates consistently in 2022 and through most of 2023—just recently pausing its tightening cycle, which greatly aided in bringing inflation down to 3.18% from 9.1% during that time period. While we have seen some commentary suggesting that the Fed will begin cutting rates by the end of the year, the news from Jackson Hole suggests that we may be in for an extended period of higher rates through at least mid-2024. Chart 1 below shows U.S. quarter-over-quarter (QoQ) GDP plotted against personal consumption QoQ.

Chart 1:

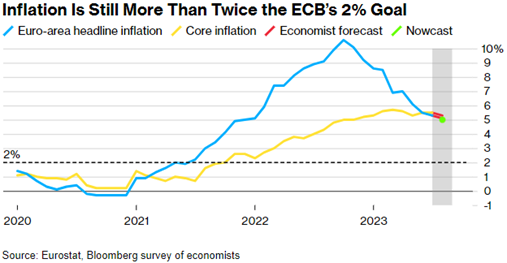

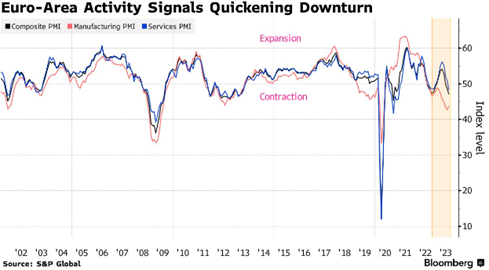

While the U.S. received somewhat clear direction from the Fed last week, Europe faces relative silence from Christine Lagarde and the European Central Bank (ECB) leading up to the bank’s Sept. 14th meeting. Inflation has continued to run rampant in the Eurozone and is the core focus of the ECB’s data-dependent policymaking. For reference, EU core inflation (ex-Energy) remains above 5% versus the central bank’s 2% target (the same as the Fed’s target). See Chart 2 showing European inflation data. However, the recent release of Europe’s Purchasing Managers’ Index (PMI) signaled the contraction of private sector activity, meaning there is now more significant downward pressure on inflation. See Chart 3 for both components and composite of PMI charted against each other from 2002 through the present.

Chart 2:

Chart 3:

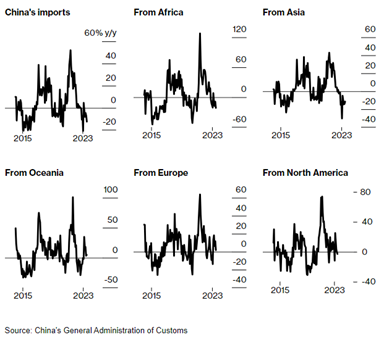

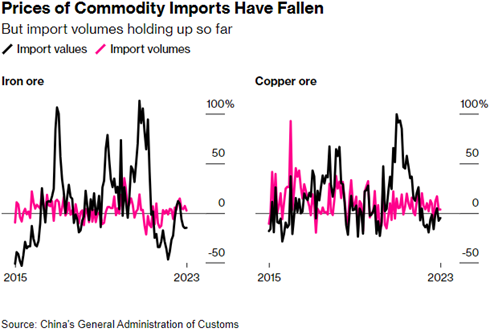

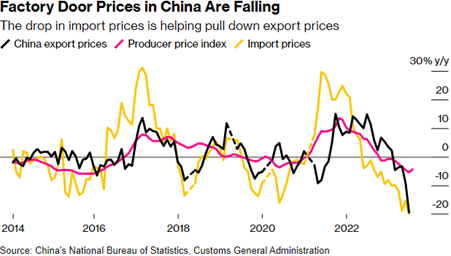

This year, China’s economy was supposed to drive 1/3rd of global economic growth. For reference, for every 1% gain in China’s growth rate, global expansion is boosted by 0.3%. Unfortunately, the country’s post-pandemic reopening has been fraught with weak data seeping into its trade partners. So far this year, more than $10B has been pulled from China’s stock markets in the longest stretch of net outflows in the country’s history. This does not mean there are no benefits from an economic slowdown in China. For example, China’s slowdown will depress oil prices and lower prices for exported goods. This is good news for other places, such as the U.S. and Eurozone, which are still battling elevated inflation and will benefit from falling Chinese demand. Chinese imports have fallen as demand dropped from pandemic-era highs. See Charts 4and 5 for Chinese import data. Chart 6 belowshows export prices falling with the Producer Price Index (PPI) and import prices.

Chart 4:

Chart 5:

Chart 6:

What to Watch

Monday, Aug. 28th

4:30PM – Retail Gas Price (Prior: $3.984/gal.)

Tuesday, Aug. 29th

9:00AM – Case-Shiller National Home Price Index (Prior: 302.38)

10:00AM – Total Nonfarm U.S. Job Openings (Prior: 9.582M)

Wednesday, Aug. 30th

8:30AM – Real GDP QoQ (Prior: 2.40%)

10:00AM – Pending Home Sales QoQ/YoY (Priors: 0.26% / -15.60%)

Thursday, August 31st

8:30AM – Personal Income/Spending MoM (Priors: 0.31% / 0.55%)

12:00PM – 30 Year Mortgage Rate (Prior: 7.23%)

Friday, Sept. 1st

8:30AM – Labor Force Participation Rate (Prior: 62.60%)

8:30AM – Nonfarm Payrolls MoM (Prior: 187.00K)

8:30AM – Unemployment Rate (Prior: 3.50%)

11:00AM – U.S. Recession Probability (Prior: 66.01%)

Federal Reserve policymakers signaled that they remain vigilant in their fight against inflation with the end goal continuing to be a 2.00% target rate. We believe Chairman Powell sees the impact of the aggressive tightening in 2022-23 and hinted that the impact of these hikes has yet to be fully felt across the economy. We think a continued pause in rate hikes at the September FOMC meeting is plausible but, of course, all actions are data dependent. U.S. economic growth remains resilient with a solid jobs market which is boosting consumer spending. The bond market continues to modestly sell off, especially in the short end of the curve, but this move is also offering investors a yield component on bonds that we have not seen in many years. Summer is nearing a close, back-to-school shopping is underway or already done and Wall Street will be getting back from the Hamptons and elsewhere. “Sell-in-May and Go-Away” means traders and portfolio managers will be hitting the floor looking to cement positive returns for year-end bonus season. Also, pay attention to the shifting climate in China as this will impact the global economy. Please reach out to your advisor at Valley National Financial Advisors with questions or concerns.

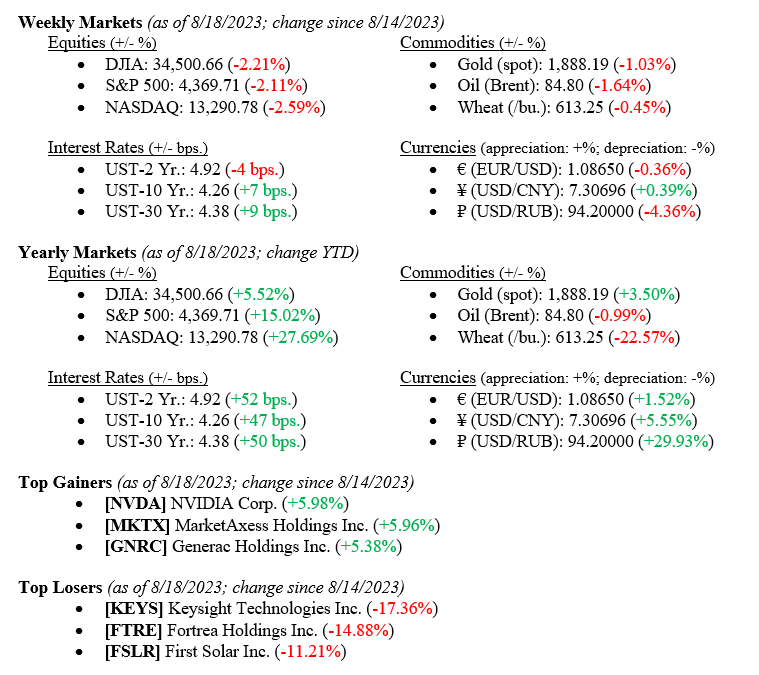

The Dow Jones Industrial Average ended the week down 2.21%, the S&P500 index lost 2.11%, and the NASDAQ fell 2.59%. Global stocks declined due to concerns about China’s economic conditions and rising global rates. Investors also continue to grapple with inflation concerns. Additionally, the CBOE Volatility Index (VIX) reached its highest level since May 2023 last week, indicating increasing market anxiety. The Federal Reserve is meeting in Jackson Hole, WY, this week—we will be watching this symposium to gauge the Fed’s policy stance going forward. We still believe that the Fed will be able to gently land the economy and avoid a recession despite being seemingly bombarded with news to the contrary.

Global Economy

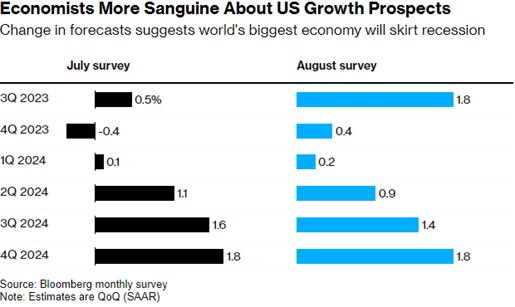

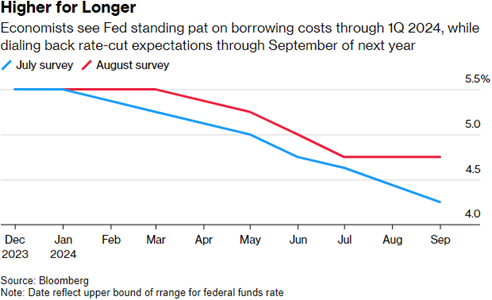

According to a recent survey, the projected 3Q GDP growth has surged to 1.8%, a notable increase from the earlier estimate of 0.5% in July, as seen in Chart 1 below. The economy’s strength is driven by resilient consumer spending, supported by recent retail sales data and a strong job market. Economists’ revised projections depict an average U.S. economic growth of 2% this year and 0.9% in 2024, exceeding previous estimates and aligning with more positive global forecasts. Despite inflation concerns, economists foresee a prolonged period of higher interest rates without any imminent rate hikes, as seen in Chart 2 below. The possibility of a rate cut has been pushed to the second quarter of the following year, reflecting their confidence in a more resilient economy.

Chart 1:

Chart 2:

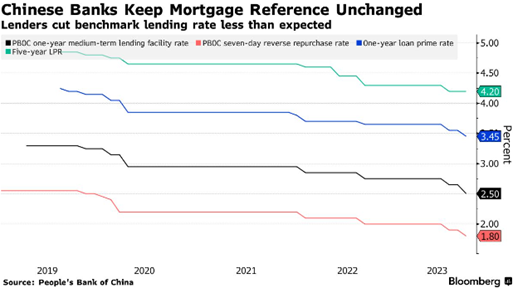

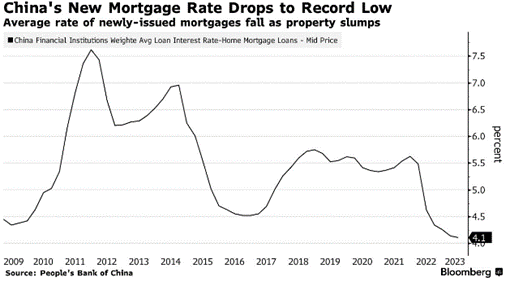

Chinese banks have maintained the key five-year loan prime rate (LPR) at 4.2%, defying predictions for a 15-basis point cut, while ten basis points reduced the one-year LPR to 3.45% (see Charts 3, 4). This unexpected move reflects China’s dilemma in balancing the need to stimulate economic growth with the imperative to ensure the banking system’s stability. The decision is seen as an effort to protect banks’ net interest margins and profitability, which are crucial for financial stability. The Chinese government is grappling with the challenge of bolstering borrowing demand amidst deflationary pressures and waning confidence, all while trying to avoid instability in the financial sector.

Chart 3:

Chart 4:

What to Watch

Monday, August 21st

Retail Gas Price at 4:30PM (Prior: $3.962/gal.)

Tuesday, August 22nd

Existing Home Sales/MoM at 11:00AM (Priors: 4.16M / -3.26%)

Thursday, August 24th

Initial Claims for Unemployment Insurance at 8:30AM (Prior: 239k)

30 Year Mortgage Rate at 12:00PM (Prior: 7.09%)

Friday, August 25th

Index of Consumer Sentiment at 10:00AM (Prior: 71.20)

While the market has had negative returns in the past few weeks, we remain cautiously optimistic about the U.S. economy and the markets for 2023. Please reach out to your contact at Valley National Financial Advisors with any questions.

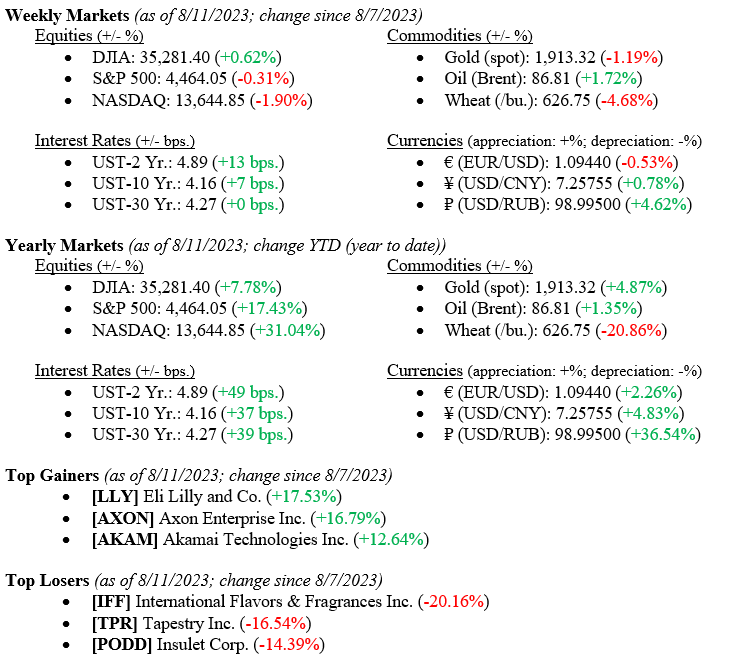

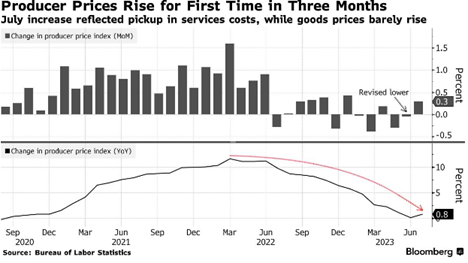

Markets ended last week mostly flat, with the Dow Jones Industrial average netting a 0.62% gain, while the S&P500 and NASDAQ lost 0.31% and 1.90%, respectively. Year-to-date returns on all three major indexes remain well in positive territory (see details below). In terms of economic data released last week, the Producer Price Index (PPI) increased month-over-month and year-over-year, which means it is still contributing to inflation despite it slowing considerably. While the Fed is waiting for solid economic data before announcing they won the inflation war, American Consumer’s inflation expectations are declining. The current inflation expectation rate is just 3.3% overall over the next year versus the 3.4% figure that was anticipated in July. Interest rates continued to increase last week, with the 10-year U.S. Treasury increasing seven basis points to end the week at 4.16%.

Global Economy

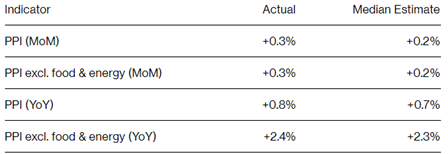

U.S. Producer Prices increased in July due to rises in service categories, underscoring the challenges in managing inflation. The Producer Price Index for final demand and the core index, excluding food and energy, rose by 0.3% in July, slightly surpassing predictions. Factors like stabilizing supply chains, limited overseas demand, and shifting consumer spending towards services have eased producer-level inflation. However, recent oil price hikes are reintroducing inflationary pressures. Inflation in healthcare services accelerated, impacting key inflation measures. Recent consumer price data indicating minimal gains might deter the Federal Reserve Bank from raising interest rates in September. The Core PPI, which excludes volatile components like food and energy, increased only 0.3% in July and 2.4% annually, which is getting close to the Fed’s target rate of 2.00%. See the detailed charts below from Bloomberg.

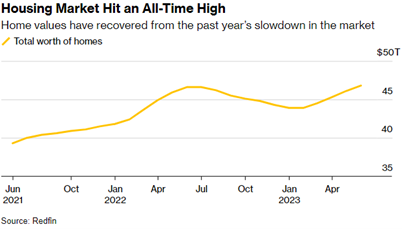

The U.S. housing market has rebounded, recovering nearly $3 trillion in lost value from the previous year’s slowdown. A continued shortage of listings has driven up prices and elevated the total worth of U.S. homes to a record $47 trillion, as reported by Redfin Corp, see Chart 2 below from Redfin. The reluctance of homeowners to relinquish their lower-rate mortgages amid rising borrowing costs has resulted in only 1% of U.S. homes changing ownership this year, the lowest figure in a decade.

Policy and Politics

During the upcoming BRICS (Brazil, Russia, India, China, & South Africa) economic summit in South Africa, discussions will revolve around increasing the utilization of local currencies for trade among member states, including establishing a common payments system and potentially forming a technical committee to explore the concept of a joint currency. The focus is not on replacing the U.S. dollar as the global currency but rather on enhancing the use of domestic currencies to foster trade and counterbalance the dominance of the U.S. This is important to us to watch as some BRICS countries are part of the major move in U.S. manufacturing around nearshoring (moving offshore manufacturing physically closer to U.S. headquarters) and friend-shoring (moving offshore manufacturing to trade partners deemed more “business friendly”) since the massive supply chain disruptions that were seen during the pandemic.

What to Watch

Monday, August 14th

U.S. Retail Gas Price at 4:30PM (Prior: $3.94/gal.)

Wednesday, August 16th

U.S. Housing Starts / MoM at 8:30AM (Priors: 1.434M / -8.02%)

U.S. Job Openings: Total Nonfarm at 10:00AM (Prior: 9.582M)

Thursday, August 17th

U.S. Initial Claims for Unemployment Insurance at 8:30AM (Prior: 248k)

30 Year Mortgage Rate at 12:00PM (Prior: 6.96%)

As is typical in August, markets reach a calm/quiet period as Washington, DC, is on vacation with much of the rest of the country and world. Federal Chairman Jay Powell has slowly crafted his economic soft landing (battling inflation with higher interest rates and not sending the economy into a recession). However, the war is ongoing as inflation is still above the 2% target (U.S. Inflation Rate for July 2023 was 3.18%). As noted above, equity markets have slowly increased year-to-date, reflecting strong economic conditions, healthy labor and housing markets, and resilient consumers. Our mantra remains that investors can be cautiously optimistic for the remaining part of 2023.

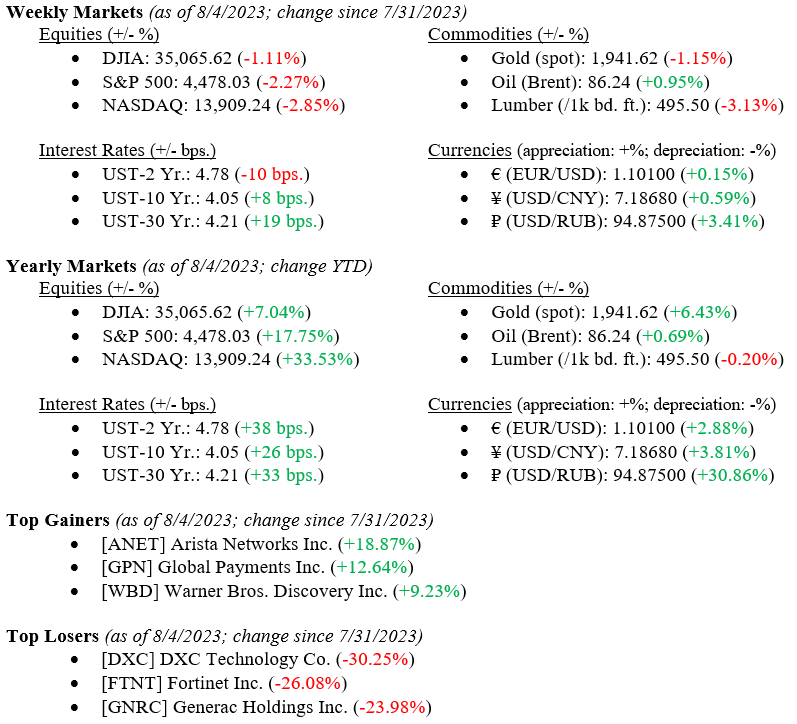

Markets ended the previous week lower overall, with the DJIA down 1.11%, the S&P down 2.27%, and the NASDAQ down 2.85%. Despite these slight moves downward, year-to-date equity indices are trying to make up for a weak 2022, with the Dow up 7.04%, S&P up 17.75%, and NASDAQ up 33.53%–they still have a way to go before breaking even. Still, at least this is a move in the right direction as the Fed continues to work towards avoiding a recession. Last week, U.S. recession probability dropped by about 2% to 66.01%, while unemployment fell to another record low of 3.50%. We are in the camp that the Fed will avoid a recession with its current path of interest rate hikes. While a recession is possible, we still believe that the Fed is well on its way to pulling off its “soft landing, Goldilocks” scenario.

Global Economy

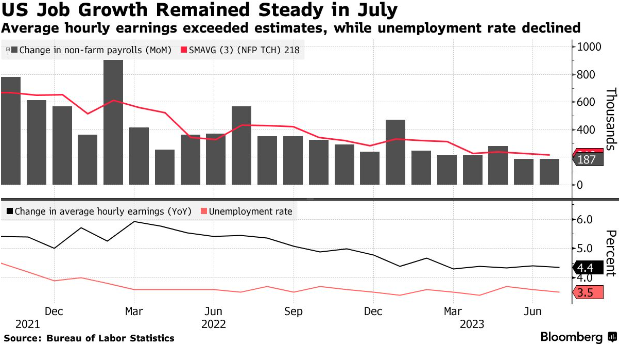

U.S. employment showed strong growth in July, accompanied by higher-than-anticipated wage increases, reflecting ongoing labor demand that is driving the economy’s renewed momentum. Nonfarm payrolls rose by 187,000, following a similar increase in June, with the unexpected decline in the unemployment rate to 3.5%, among the lowest in decades. The robust job and income gains suggest the economy can withstand rapid interest rate hikes aimed at curbing inflation, boosting consumer confidence, and potentially supporting spending and growth. Despite signs of wage growth slowing down due to labor supply and demand balancing after pandemic-related shortages, service providers, particularly in healthcare, financial activities, and construction, saw increased employment. The data, combined with relatively low inflation, suggest the Federal Reserve can manage price pressures without triggering a recession, influencing its upcoming decisions on interest rates. However, challenges remain, including potential future rate hikes and managing inflation, especially with the impending resumption of student loan payments. While President Biden’s policies have spurred growth, rising debt prompted a credit rating downgrade by Fitch Ratings.

Fitch Ratings’ downgrade of U.S. government debt from AAA to AA+ has elicited criticism from both Washington and Wall Street, despite concerns over the nation’s swelling fiscal deficits and their potential impact on markets, the economy, and the upcoming presidential election. The downgrade comes after Fitch had previously warned of such a move due to debates over raising the debt limit. The downgrade was attributed to the expectation of deteriorating finances over the next few years due to tax cuts, new spending, economic shocks, and political gridlock. Treasury Secretary Janet Yellen criticized the timing and called the downgrade “arbitrary” and “outdated,” while market reactions were mixed, with bonds staying relatively stable but risk-sensitive assets taking a hit. The downgrade underscores the worsening U.S. fiscal outlook, although investors are likely to view it as a medium-term concern. The political fallout and debates over the downgrade are expected to continue through the 2024 election. Fitch’s action increases the U.S.’s debt vulnerability and projected debt-to-GDP ratio, raising concerns about the nation’s resilience to economic shocks. Despite this, the market’s reaction remains uncertain, as the downgrade could lead to increased safe-haven buying of U.S. Treasuries and the dollar.

A surge in government bond selling intensified on Monday due to concerns about potential further interest rate hikes, leading to a rise in 30-year German bond yields to their highest level since 2014 and a six-basis point increase in similar-maturity Treasury yields. Although US equity futures saw a modest increase, investors remained wary as Federal Reserve Governor Michelle Bowman’s comments over the weekend hinted at the necessity of additional rate hikes to curb inflation. Anticipation for upcoming US inflation data added to market uncertainty, with the consumer price index reading expected to show a 0.2% rise in July, marking the smallest consecutive gains in 2.5 years. Despite this, stock trading remained relatively subdued, with European stocks retreating and German industrial output hitting a six-month low, signaling economic weakness.

What to Watch

Monday, August 7th

U.S. Retail Gas Price at 4:30PM (Prior: $3.869/gal.)

Tuesday, August 8th

U.S. Trade Balance on Goods and Services at 8:30AM (Prior: -68.98B USD)

Wednesday, August 9th

U.S. Crude Oil Stocks WoW at 10:30AM (Prior: -17.05M bbl.)

Thursday, August 10th

U.S. Consumer Price Index MoM/YoY at 8:30AM (Priors: 0.18% / 2.97%)

U.S. Inflation Rate at 8:30AM (Prior: 2.97%)

U.S. Initial Claims for Unemployment at 8:30AM (Prior: 227,000)

30 Year Mortgage Rate at 12:00PM (Prior: 6.90%)

Friday, August 11th

U.S. Producer Price Index MoM/YoY at 8:30AM (Priors: 0.14% / 0.13%)

U.S. Index of Consumer Sentiment at 10:00AM (Prior: 71.60)

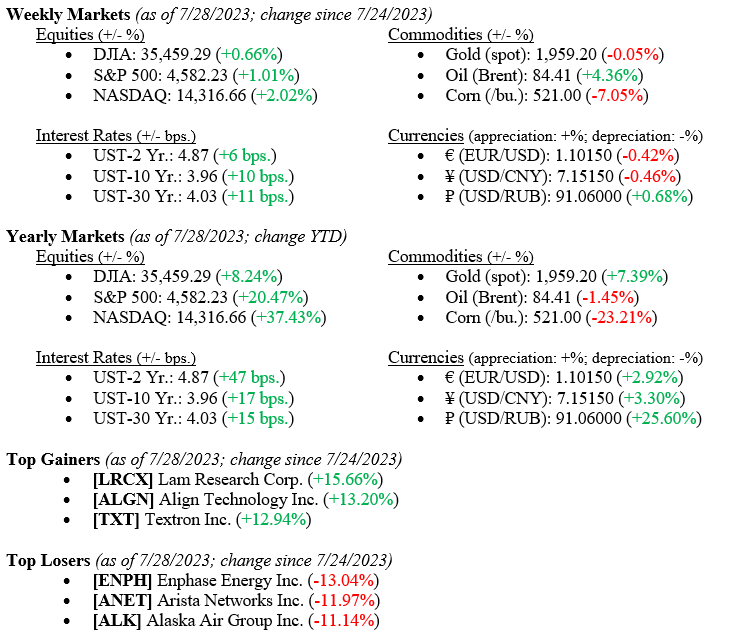

Week by week, the mythical “Goldilocks” scenario plays out, where the Fed tackles rampant inflation with higher interest rates and slows the economy as a result, but not so much so that we roll into a recession – this is also commonly called a “soft-landing,” and Fed Chairman Jay Powell, like others, is seeking this outcome. All the while, equity markets continue to quietly move higher as they did last week, with gains across all three major market indexes. For the week, the Dow Jones Industrial Average gained +0.7%, the S&P 500 Index added +1.0%, and the NASDAQ notched a gain of +2.0%. Year-to-date gains remain comfortably solid, with the Dow Jones Industrial Average at +8.2%, the S&P 500 Index at +20.5%, and the tech-heavy NASDAQ at +37.4% for the year.

US Economy

Last week we showed how inflation has moved from 9.1% in July 2022 to just under 3% a year later. This sharp drop in inflation is a direct result of the Federal Reserve raising interest rates from a range of 0.00-0.25% to 5.25%-5.50% in just under 18 months. A move this fast and this steep in interest rates, which immediately inverted the yield curve, typically slows the economy so much that a recession is the result. We at TWC have consistently stood against this typical pattern this year. Our premise was based on a solid labor market as evidenced by an unemployment rate at a paltry 3.6%, healthy consumer spending, banks continuing to lend with healthy balance sheets, corporate earnings still in the green column, and the US housing market still growing.

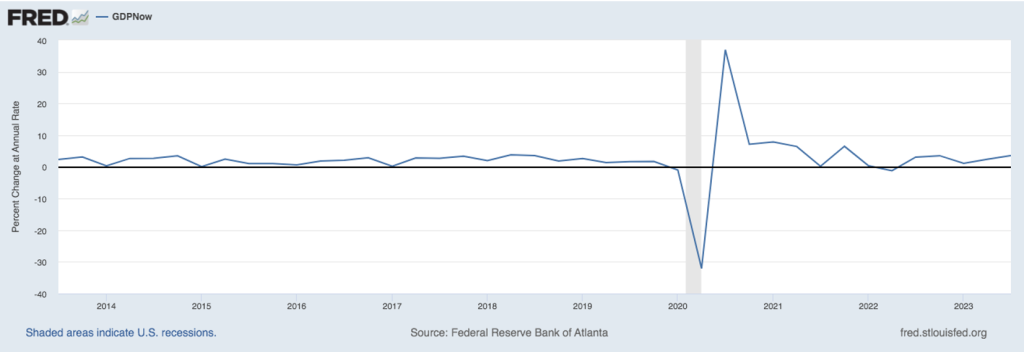

Markets continue to rally, seeing beyond the short-term concerns and instead looking ahead and understanding the fundamentals driving prices higher: we are near the end of the interest rate hikes, inflation is abating, and economic growth is accelerating rather than slowing. Last week, the Atlanta Fed raised second-quarter US GDP (Gross Domestic Product) estimates to +2.4% from +2.0%. See Chart 1 belowfromtheFederalReserveBankofSt. Louis, showingtheU.S. GDPestimate. The third quarter 2023 estimate for US GDP growth is +3.5%. Fed Chairman Jay Powell certainly seems to be getting his “Goldilocks” ending.

Policy and Politics

Washington is thankfully on vacation until after Labor Day so we can relax and not worry that new restrictive legislation will be dumped on consumers or corporations. Instead, we have a quiet period where the markets and economy will digest the news cycle this week, including earnings reports from some of the most important companies, including Apple and Amazon.com. Other important global news is coming from China, where further government stimulus was announced.

What to Watch

U.S. Job Openings Non-Farm for June 2023, released 8/1/23, prior level 9.824M job openings.

U.S. Labor Force Participation Rate for July 2023, released 8/6/23, prior rate 62.6%

U.S. Unemployment Rate for July 2023, released 8/6/23, prior rate 3.6%

The “Goldilocks” scenario certainly is plausible, and last week we saw positive GDP growth along with declining inflation. All the while, companies continue to report favorable earnings, and the buzzwords of the future remain “artificial intelligence,” or AI. AI is supposedly turning out to be the panacea of everything that is wrong with the world, from healthcare to education to global climate change. We at VNFA remain cautiously optimistic about the economy and the financial markets, basing our assumptions on the American Consumer. Volatility remains calm, and Mr. Powell may get his soft landing, but vigilance and caution should always be used. Reach out to anyone at Valley National Financial Advisors for assistance.